Sezeryadigar/iStock via Getty Images

Introduction

Despite being a long-term supporter of Altria (NYSE:MO) and their dividends, it was not a smooth ride with continuous disappointments and frankly speaking, their lackluster share price performance hindering the appeal of their dividends. Following further setbacks relating to their largely failed JUUL investment near the middle of 2022, my previous article discussed how it was time to start thinking about the end of their dividends. Fast-forward to the present day and after digging further into their numbers and viewing the situation from a different angle, it sadly appears the old model is breaking that supported their financial performance and thus as a result, it risks a dividend cut one day in the future.

The Old Model

Similar to any investment, there are always many moving parts to consider and whilst their dividends are obviously grabbing the majority of the attention, which is fair but alas, it is arguably somewhat short-sighted. They obviously require earnings and more importantly, free cash flow and whilst this aspect also receives attention, I nevertheless feel the core driving force is often neglected, most likely because it has consistently been unproblematic for decades.

After largely failing to diversify into JUUL, IQOS and so forth during the past few years, as documented and discussed elsewhere on this platform, their present and future is still heavily dependent upon tobacco and mostly, cigarettes. To this point, during the first nine months of 2022 their smokeable products business segment reported operating income of $8.112b, thereby forming a staggering circa 89% of their total result of $9.101b. It is commonly known by investors that smoking rates have been decreasing for decades but due to the elasticity of tobacco demand, tobacco companies have been capable of not only supporting their earnings but actually driving them higher across the years. Hence why their recent operating income was modestly above its previous result of $7.901b during the first nine months of 2021.

Due to their financial performance seemingly defying gravity during the last few decades, I feel the trajectory of their cigarette volumes is often overlooked, which is not surprising given their otherwise solid financial performance. In my eyes, this is a risky assumption in this fast-evolving world, not just economically but more so, politically and socially and thus it raises the question of whether their cigarette volumes are seeing a smooth diminishing decline or a linear decline.

Author

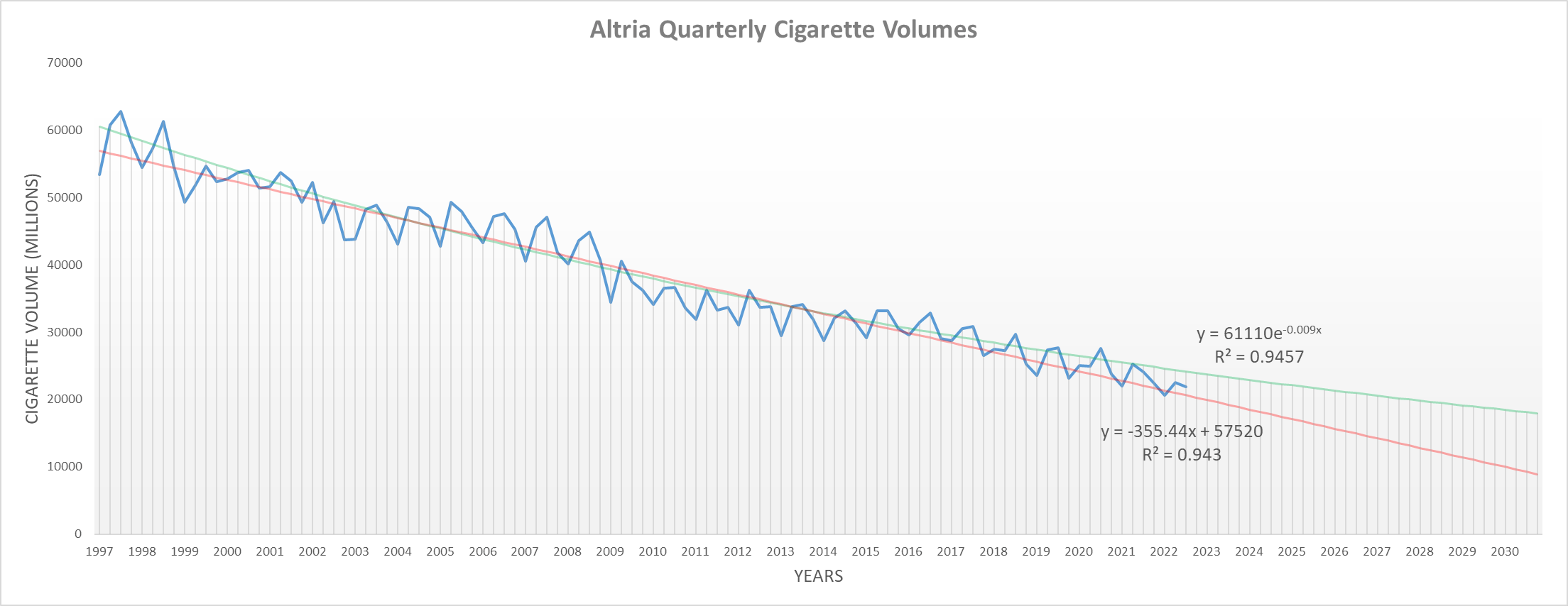

Whilst it was not a quick task, collecting and graphing their cigarette volumes from their SEC Filings dating back to the beginning of 1997 provides useful context and insights, which was selected as it represents the peak from the available data. As a side note for anyone wondering, this data excludes international cigarette volumes from the past before their spin-off of Philip Morris (PM), thereby ensuring it is not skewed.

Unsurprisingly, their cigarette volumes in recent years are well beneath their previous levels in past decades with a clear and strong downward trend. More worryingly, when overlaying exponential and linear and trend lines, they both fit the data set equally as well with almost identical R-Squared values of 0.9457 and 0.943, respectively.

On the surface, this may initially sound like nothing more than boring mathematics but actually, it carries significant ramifications for their financial performance and thus as a result, their dividends. If circling back to the above graph, it shows a stark difference between the exponential and linear trends emerging as 2030 approaches. In fact, if their cigarette volumes take the latter path, they would only be roughly half that of the former, which is alarming and thus calls into question whether they can maintain their earnings via hiking cigarette prices.

Author

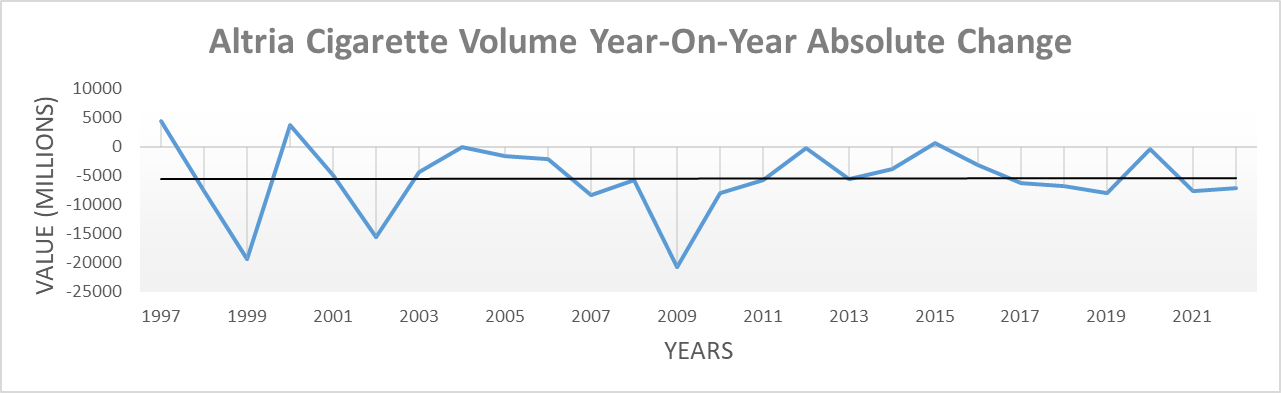

If looking at this same period of time but instead, graphing the year-on-year absolute changes of their cigarette volumes, it sees a broadly flat trend. Despite not getting any worse, this is actually not what investors should want to see because the same decline in absolute terms grows relatively larger as the years pass, thereby indicating their trend line is more likely linear, rather than exponential and thus, I fear the old model is breaking.

Author

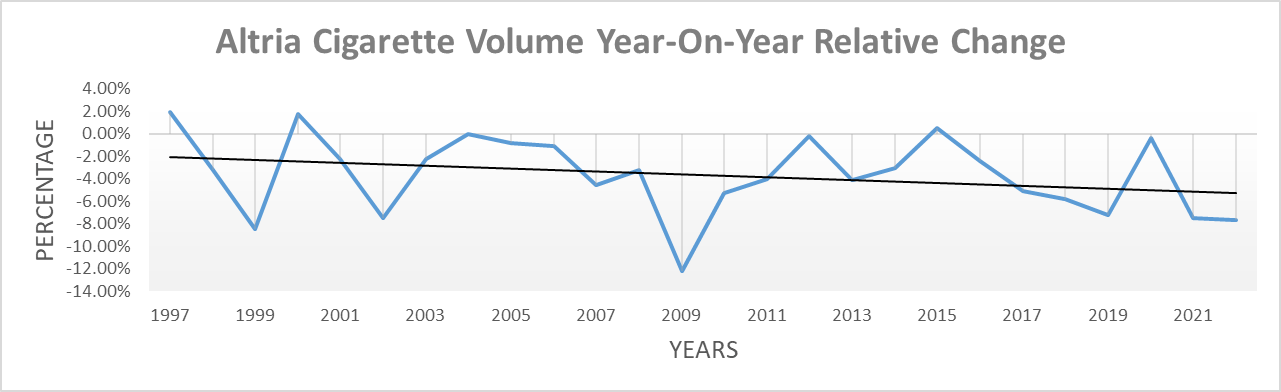

These fears are confirmed when graphing the year-on-year relative changes of their cigarette volumes during this same period of time, as the trend line is obviously pointing downwards with ever-increasing declines occurring as the years pass. Back in the late 1990s, the trend line saw a circa 2% year-on-year decline, whereas now, it is closer to 6% and thus around three times worse. As a result, it appears their volume decline is taking more of a linear decline, rather than a smooth diminishing decline, as would have been otherwise represented by the exponential trend line.

Why This Matters

Sadly, this situation is not what investors want to see because as each year passes, on average they require ever larger price hikes to offset the lost cigarette volumes, in percentage terms. Thus far, their consumers have been fairly unaffected by price hikes given the addictive nature of tobacco but nevertheless, this still has limits and thus, it cannot continue at increasingly higher rates. One day every smoker has a breaking point whereby they either quit outright, scale back dramatically or switch to a cheaper brand and with each passing year, they are pushing each of their consumers closer to this point at accelerating rates. That is unless they do not keep hiking prices in line with their ever-increasing volume declines, although this would obviously also hurt their financial performance and regardless, there is no victory.

Due to this situation, it leaves concerns surrounding when their elastic demand is finally pushed past its limit and their earnings flat line and subsequently, decline. Alas, no one can necessarily say when this day will arrive but the evidence offered by these trends is clear, the day is approaching.

To further amplify these risks, their dividend payments already consume the vast majority of their operating cash flow, such as during the first nine months of 2022 that saw the former at $4.908b against the latter of $5.637b. Once their financial performance begins to falter, it will place a dividend cut on the cards as their margin of safety is minimal, regardless of their minimal capital expenditure requirements. Not to mention, if they decide to try their hands again at diversifying away from tobacco, it will require very sizeable investments that themselves will impose a hefty cost upon their balance sheet and cash inflows and thus, it also raises the risks of a dividend cut.

It should also be considered their flagship brand, Marlboro is losing market share in recent years, such as during the first nine months of 2022 that saw a result of 42.60%, thereby down year-on-year versus their previous result of 43.00% during the first nine months of 2021. Admittedly this is only a very small change but it still indicates they do not have massive untapped potential for price hikes without suffering increasingly painful volume declines. Furthermore, as a final point to consider, it will only make this situation even grimmer if the FDA ever proceeds with regulating nicotine levels down to non-addictive levels, which has been lingering as a risk for years and discussed within my previously linked article.

Conclusion

Following the billions of dollars they have wasted on largely failed ventures, their dividends are now becoming increasingly risky as the years pass. Sadly, the evidence of their cigarette volume trend points to a linear decline, not a smooth diminishing decline and thus, I fear the old model of price hikes to offset volume declines is breaking. Since this places their dividends at risk of a cut in future years and in my eyes is more likely a case of when and not if, I now believe that a sell rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Altria’s SEC filings, all calculated figures were performed by the author.

Be the first to comment