Charday Penn

Investment Thesis

Altair Engineering, Inc. (NASDAQ:ALTR) operates in the fast-growing simulation and analysis (S&A) software market that has been delivering a ~10% CAGR in recent years. As S&A software TAM is indexed to R&D spending, I believe ALTR’s core S&A business will be resilient should a global recession arise in 2023. Despite the resilience of the company’s core business, I expect some weakness in ALTR’s automotive vertical and a related deceleration of the segment’s growth. Meanwhile, I expect ALTR’s HPC and data analytics businesses to lift the total revenue growth for the company into the low-teens range. I am optimistic about the potential for adjusted EBITDA margin expansion to 20%+ in the midterm and to 30%+ over the long term.

Altair enjoys optionality from the still-nascent growth vectors of Data Analytics and HPC

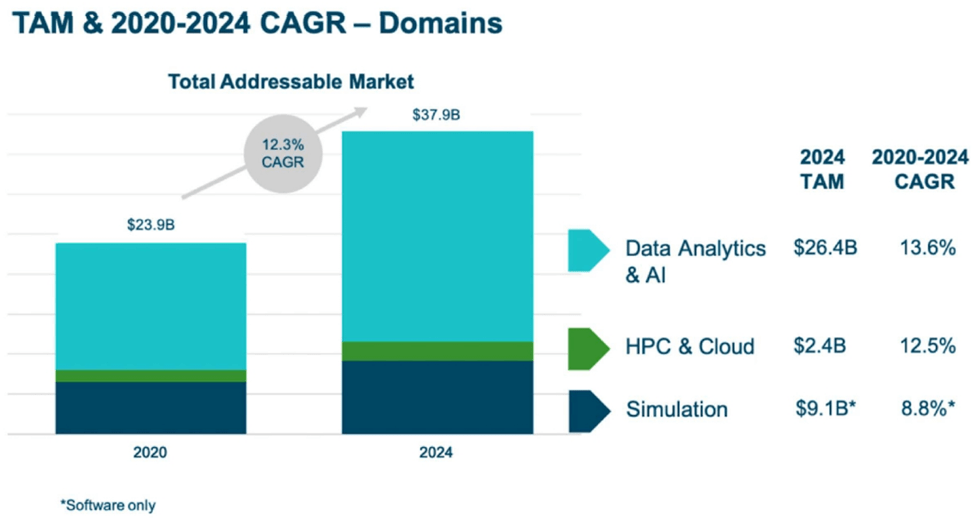

While Simulation and Analysis (S&A) account for ~70% of ALTR’s software revenue, HPC and Data Analytics’ shares of ALTR’s revenue mix are expanding due to faster market growth and market share gains. Specifically, ALTR forecasts a low-teens CAGR for the HPC and Data Analytics markets, and for this, to lift ALTR’s overall TAM CAGR to ~12%. As such, despite S&A being a 10% growth market, I look for ALTR to maintain a slightly faster long-term CAGR. While part of the HPC and Data Analytics growth will come from the banking, insurance, and financial services (BIFS) sector, ALTR is bullish on the growth of HPC and Data Analytics in its traditional automotive vertical as well as the semiconductor vertical due to cross-selling opportunities.

Altair TAM Growth Forecast (Company Presentation)

R&D intensity increasing in Altair’s core automotive market, look for the trend to be sustained

Automotive is ALTR’s largest end market, contributing 30-40% of ALTR’s total revenue over the past few years. Despite automotive being a slow-growth, cyclical industry, R&D as a percentage of auto OEM revenue has been rising in recent years. While some of the R&D intensity growth is coming from electric vehicle makers, many of which are pre-revenue, traditional auto OEMs appear to be raising their R&D intensity as well. ALTR is also investing in the electronics space, such as PCB design and analysis – e.g., via the acquisition of Polliwog, and multiphysics platforms, which are seen as the next growth vectors. While there is currently a debate on the direction of the automotive industry going into 2023, I believe automotive is still a strong market for the long term, and ALTR should be able to expand its margin in the automotive market in the long term.

Altair to maintain a 10%+ revenue CAGR, along with a pathway to expand its EBITDA margin to 30%+

ALTR has healthy business fundamentals that I believe are not fully reflected in the company’s stock price. This year, as the U.S. Federal Reserve tightens financial conditions, investors are increasingly focusing on cash flow generation and profitability as valuation tools rather than top-line growth, as we saw during the prolonged low-interest environment that just came to an end. In the past, ALTR’s relatively slow top-line growth was seen as a disadvantage. I think investors will flip their approach to valuation and that the company’s profitability and margin expansion will become upside drivers for the stock.

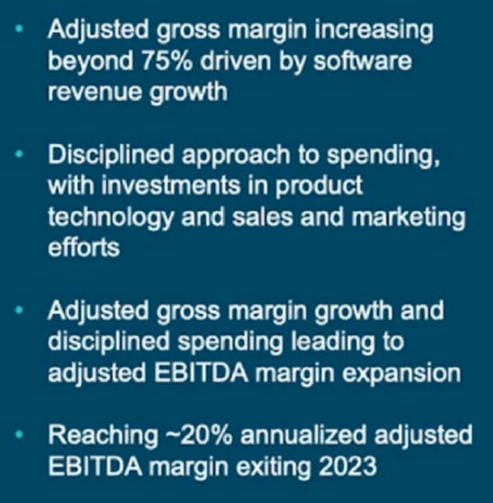

Based on a 10% revenue CAGR, ALTR is targeting a ~20% adjusted EBITDA margin exiting 2023. With the 2022 EBITDA margin to be ∼17%, I believe 20% will be a milestone, and the company will target expanding margins to 30% next. Given ALTR’s design and engineering software peers are already generating ~30% operating margins, I believe ALTR can also target and achieve a 30%+ EBITDA margin.

Altair Mid-Term Outlook on Bottom Line Growth (Company Presentation)

Valuation

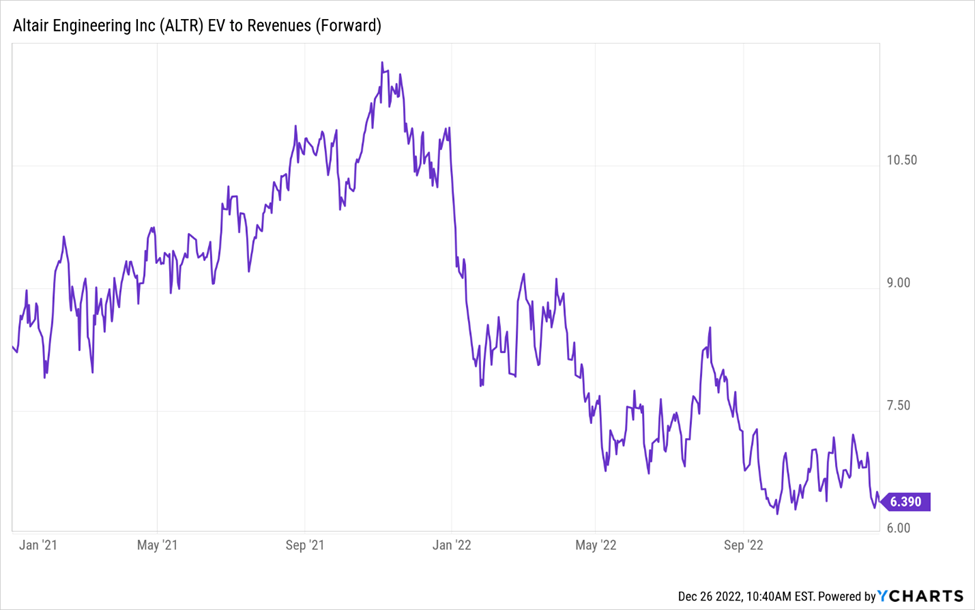

My valuation is based on an EV/sales multiple. The company’s valuation multiple has been quite volatile since COVID-19 first impacted the market in March 2020. While I think ALTR’s peak multiple of 11x forward sales, reached in November 2021, might be a thing of the past, the stock is almost back to the pre-COVID valuation level, a level that I believe is largely derisked.

ALTR is already profitable, generating positive free cash flow, and has the potential to expand its EBITDA margin to 20%+ by 2024 and to 30%+ over the next five years. As such, I value the shares at an EV/sales multiple of 8x my 2024 estimate, a premium to today’s valuation multiple of 6.4x. As a recession looms and a potential Fed pivot is on the horizon, I believe ALTR’s peers will rerate higher over the next 12 months. As such, I look for ALTR’s stock to trade up to an ~8x multiple over the coming 12 months. My December 2023 target price on the stock stands at $60 and is based on an EV/sales multiple of 8x my 2024 EBITDA estimate.

Altair EV/sales (Ycharts)

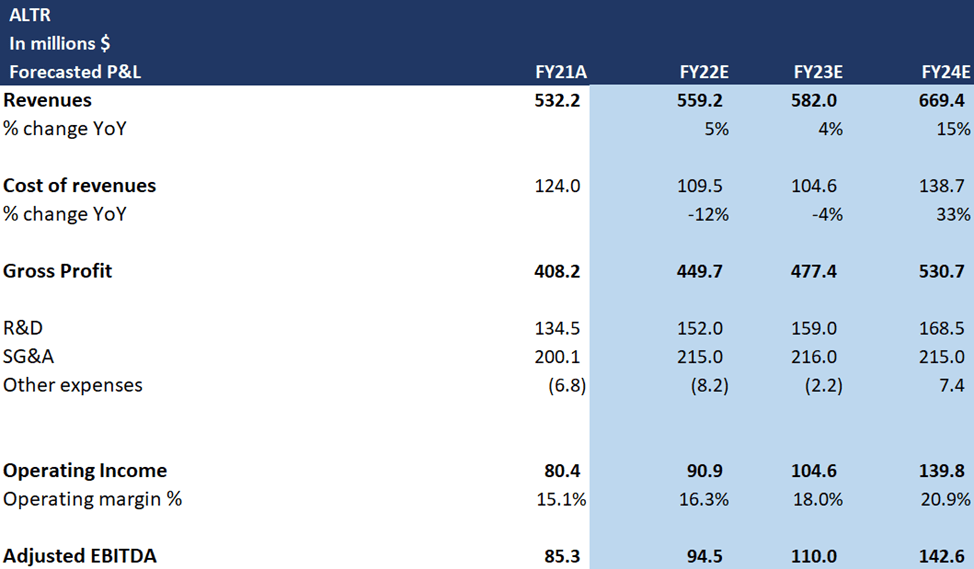

Altair forecasted P&L (my estimates)

Risks

Altair’s relatively low margin means its valuation might be more subject to changes in interest rates than peers

Software stocks were hit harder through this year’s Fed tightening cycle and are generally more exposed to interest rate risk than stocks in other industries. I expect higher-margin software names to see better valuation support than lower-margin names. While this might be a risk for ALTR today, it could become a major upward driver for the stock as the company marches ahead to its 20% EBITDA margin goal and a potential long-term margin of 30%.

Foreign exchange appears to have a more meaningful impact on Altair

ALTR bills customers primarily in local currencies. With half of the total revenue coming from EMEA and APAC, ALTR’s revenue growth, denominated by the USD, took a hit this year. Should the USD remain strong, ALTR’s foreign exchange headwind might not be over. However, I think the rapid appreciation of the USD might be slowing and that the FX headwind will ease.

Final Thoughts

ALTR’s core simulation business is indexed to R&D spending across automotive, aerospace, financial services, and others, which will help Altair prove resilient in a recessionary macroeconomic environment. And that is the fundamental reason why I believe 2023 will be a growth year for ALTR. I have estimated a 10% CAGR for the company’s revenue and look for its EBITDA margin to expand to 20%+ by 2024. I keep a price target of $60 on the stock with EV/sales multiple of 8x the 2024 EBITDA estimate.

Be the first to comment