Jason Tang/iStock via Getty Images

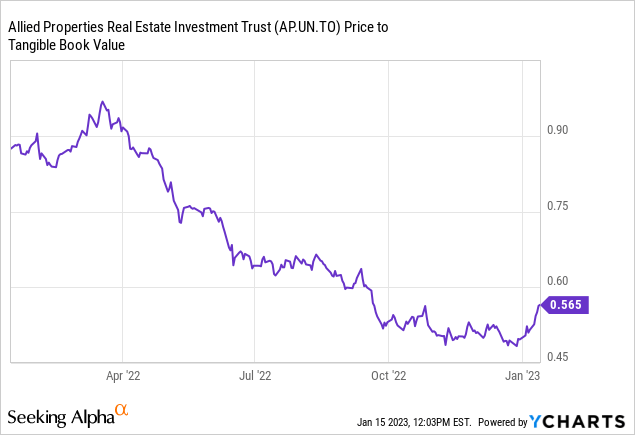

Valuation was baiting investors the last time we wrote about Allied Properties Real Estate Investment Trust (APYRF) (TSX:AP.UN:CA). This office (primarily) and retail REIT was still bearing the brunt of the market ire towards its kind. The Q3 results showed stable occupancy levels and slightly higher rents per square foot compared to the prior quarter, but the stock was still trading lower than its long-term lows. Allied specializes in Class I properties, which in the REIT own words:

…typically features high ceilings, abundant natural light, exposed structural frames, interior brick and hardwood floors. When restored and retrofitted to high standards, Class I workspace can satisfy the needs of the most demanding office and retail users.

Source: Q3-2022 Financial Report

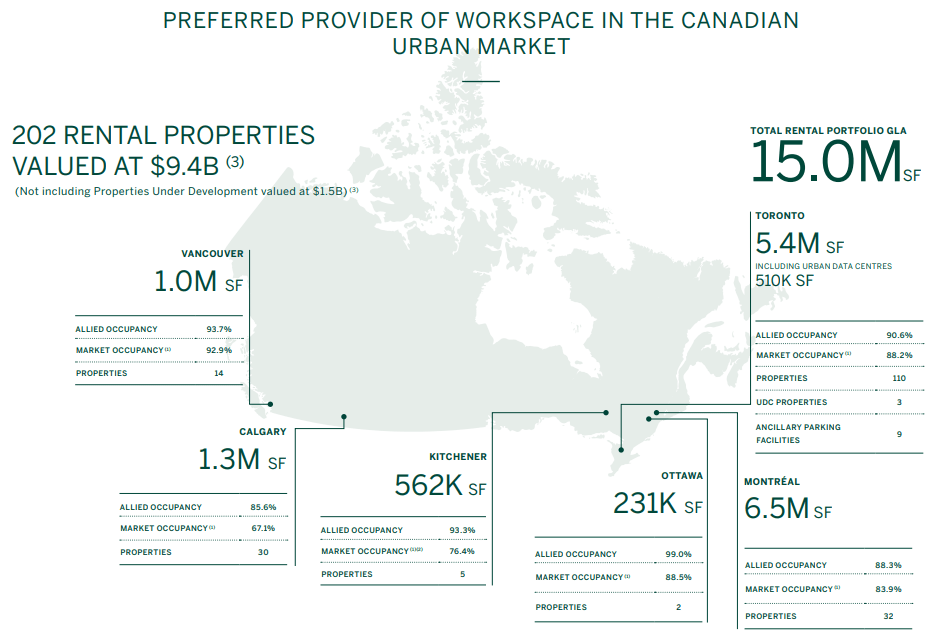

Before office properties replaced the word anathema in the dictionary, investors happily paid a 10%-20% premium for this specialized REIT. The premium was paid in part also because majority of its properties were in Toronto and Montreal, markets which bought on a duchenne smile on collective faces.

Q3-2022 Financial Report

We still passed on it because there were others in the office space we liked better, and we felt interest rate and lease rollover challenges would still persist. We also said,

While Calgary and Edmonton exposure is modest, it will still pressure rents going forward. Allied’s equity cost has vaulted higher and at this point issuing equity so far below NAV is really not feasible. What it needs to demonstrate here is perhaps the underlying value is sound and sell assets at or above book value. This would help it complete its internal development projects without increasing debt or diluting equity. It will also help investors become more comfortable with the valuation metrics being presented for NAV.

Source: Allied Properties: 50% NAV Discount, But Is It Enough

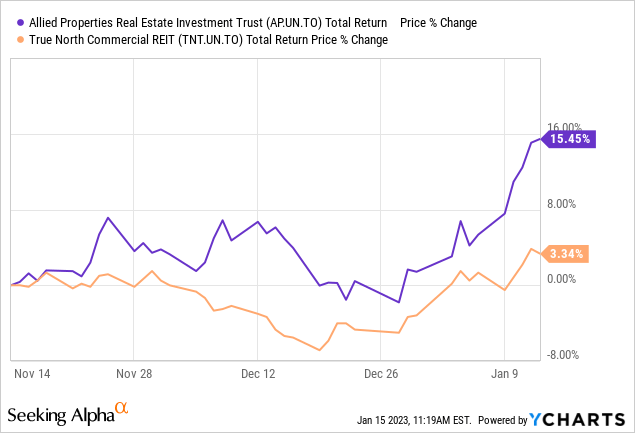

In the same piece we had noted our preference for Allied versus its brethren True North Commercial REIT (TNT.UN:CA) which was being chased by income investors. Allied has done very well comparatively since then.

Although True North still trades at a premium versus the discount that continues to plague allied. The Q4 results are due at the beginning of the next month and we have already discussed the Q3 results in the prior piece. Today, we talk about what we think the investors should expect from the upcoming results and what will set the tone for 2023.

Leasing Activity

Coming into Q4-2022, management had noted the slowdown in leasing activity. This is atypical late in Q3-2022 where touring is strong. Q4-2022 will be the key decider of this and it will either cement of alleviate bull concerns. Management is saying the exact same thing.

So I think the right thing for us to do is to experience Q4. One thing to remember, leasing isn’t that cyclical. It tends to slow down a little in August because everybody’s working from home, so to speak, or working from their cottage or just at the cottage, but it picks up very rapidly in September. And the one thing we know from long experience is December 31 is a massive deadline for leasing. We were actually finalizing deals on December 31, 2021.

I remember. I wasn’t here, but a big part of the team was, and they were literally signing deals that date. So it’s a big, big deadline in the leasing cycle that we have experienced over a very long period of time now. And frankly, before I make any bold pronouncements, I really want to see how the fourth quarter plays out.

Source: Allied Q3-2022 Conference Call Transcript

Low leasing activity will panic the bull case, even though Allied has only 11% of its portfolio leases expiring in 2023.

Development Timeline

One thing that has handicapped Allied responsiveness to the malaise in office space has been its huge development pipeline. Granted that it did not help matters for itself by actually acquiring more properties during this challenging time period. But the development pipeline is crucial as its represents cash that is not earning any money. Allied has close to $1.5 billion of properties in development and has an estimated $300 million more to spend on them. Q3-2022 brought out delays and cost escalations on 4 different properties. The street will be watching closely for updates here.

Refinancing and Deleveraging

Allied management noted that they were not in any hurry to access the capital markets at the moment.

We’re pleased with our financial position. We allocated $108 million of capital in the quarter to revenue enhancing and development activity, which is what we’ll continue focusing on for the foreseeable future. With over 91% of our debt now on a fixed rate basis, our exposure to rising interest rates is mitigated. Also, our liquidity position is strong, allowing us to meet our commitment into 2024 without having to access either the public capital market.

Source: Allied Q3-2022 Conference Call Transcript

While this fits well with the current debt maturity profile, we believe Allied would likely need to start improving its debt metrics way before 2025.

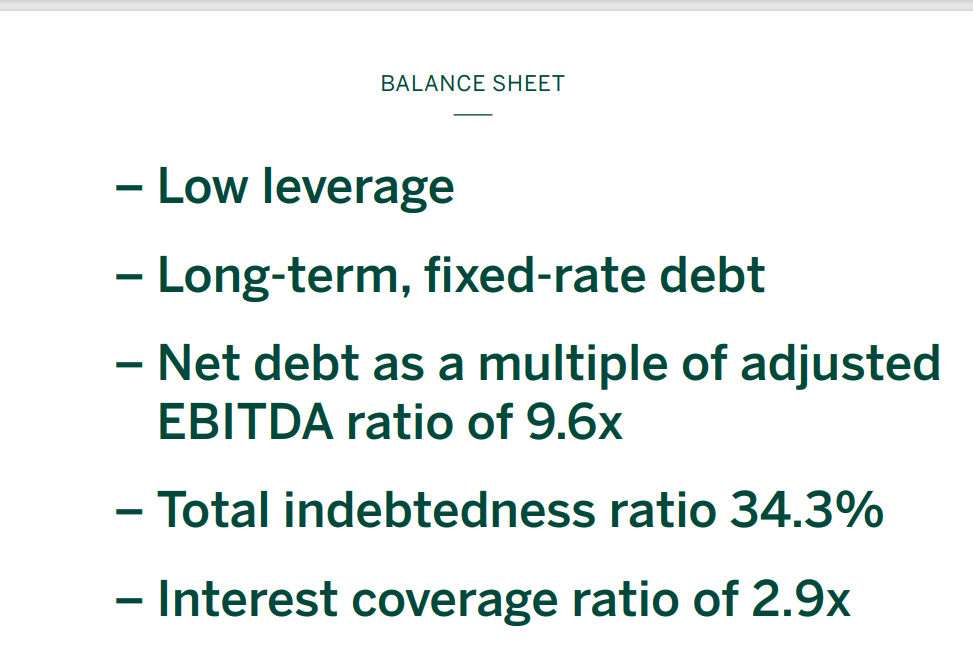

Allied November Presentation

While the company has spoken of its investment grade balance sheet, large unencumbered pool of properties and “low leverage”, we think that 9.6X number (seriously are we calling that low?) needs to move to under 8.0X in under 2 years.

Allied November Presentation

That low total indebtedness ratio of 34.3% may seem at odds with the 9.6X debt to EBITDA. That is what happens when properties have such high value/costs and such low cap rates. It takes a lot of turns of EBITDA to generate incremental funds flow. We saw the same with Brookfield Property Partners before it was taken private. But in a high interest rate environment, Allied should make that work in the reverse. Unloading properties won’t hurt funds from operations (FFO) too much.

Take Home Message

Office has its believers and we doubt the asset class is going away. Allied has some of the best office properties we have seen, by far, and if quality is your thing, this is the REIT for it.

Allied Presentation

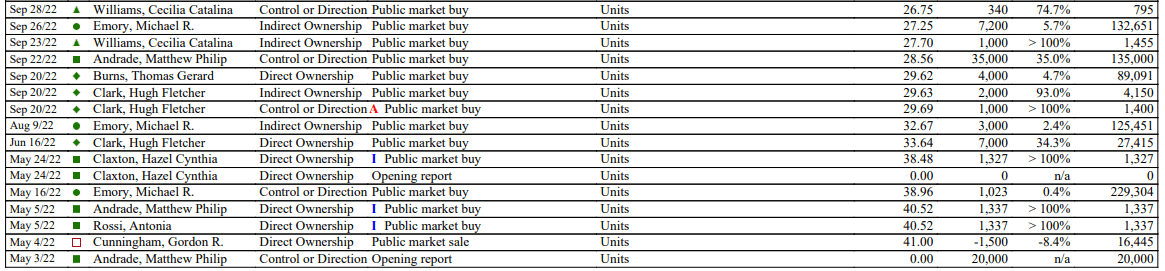

Insiders also believe in the cause and certainly stepped up to the plate in the middle of 2022 with the CEO and CFO buying shares.

Ink report

All that said, Allied cannot afford going into 2024 with debt to EBITDA approaching 10X. A recession will likely create serious stresses on the extended balance sheet. Time to deleverage is now and that same process can demonstrate to the markets the validity of its NAV. The market clearly has doubts.

The current implied cap rate is closer to 7% vs the 5% that Allied uses in its NAV calculation. A few dispositions can help set the record straight and allow for some more breathing room in the next 2 years. The company is making a general effort in this area, though we think it needs to have more urgency.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment