Cineberg

Dear readers/followers,

It’s time for an update on Allianz (OTCPK:ALIZF), the largest insurance company on earth. I’m very long at around 4.8% of my portfolio, and I have been since the company traded on the cheap. The company is also one of the largest and most attractive asset managers on the planet.

In this article, I’ll take you through my current and updated thesis for Allianz for 2023.

Allianz – Updating on the Company

Allianz has annual revenues of over €140B, from which it earns over €10B worth of operating income, while handling around €2T worth of assets under management for their customers. It has offices, coverage and operations in every single continent.

Over 150,000 people work for Allianz, and the company provides in the fields of P&C, Life/Health, and Asset management. To describe the company on a granular level can’t be done in 100 pages, let alone 10 – so a high-level overview is all we have time for.

The simple business idea of Allianz is securing people’s future, through insurance and quality asset management. They do this by being the number #1 insurance brand, and having 126M customers in more than 70 nations.

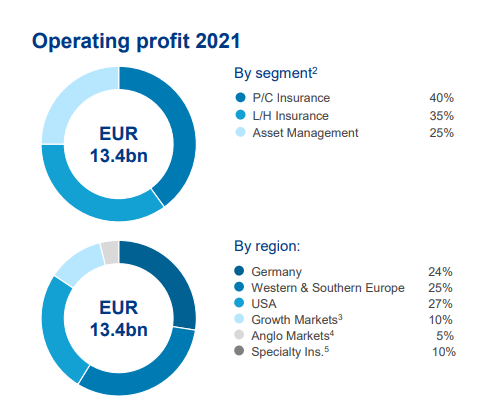

For 2021, the company generated nearly €150B of revenues, and managed to grow its operating profit by 25%. That profit came from the following business areas with the following geographical split.

Allianz IR (Allianz IR)

The company’s outlook for 2022 calls for managing a similar level of operating profit to 2021, with around €13.4B forecast. The company has a mid-term forecast of 5-7% EPS growth and an RoE level of 13%.

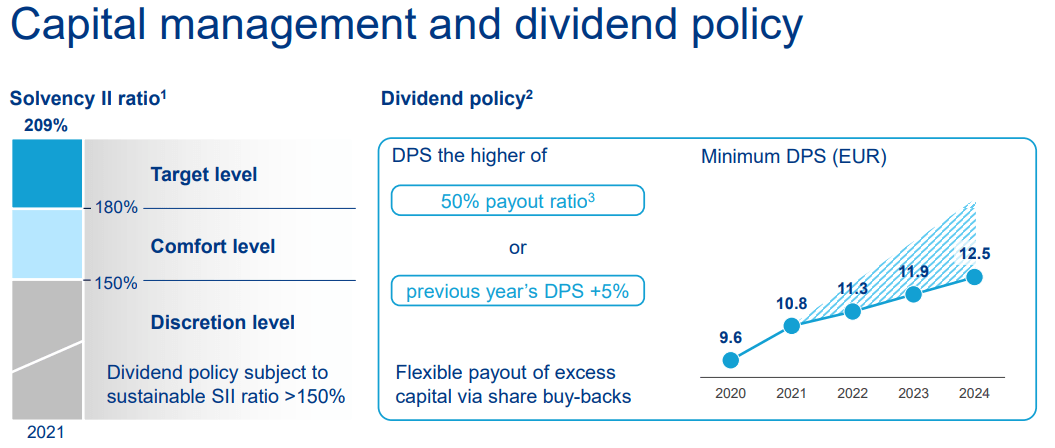

The company’s industry ratings are superb, and the company has a very attractive dividend policy, as well as payouts, including a very high solvency ratio. It is nowhere close to its comfort or discretion levels.

Allianz IR (Allianz IR)

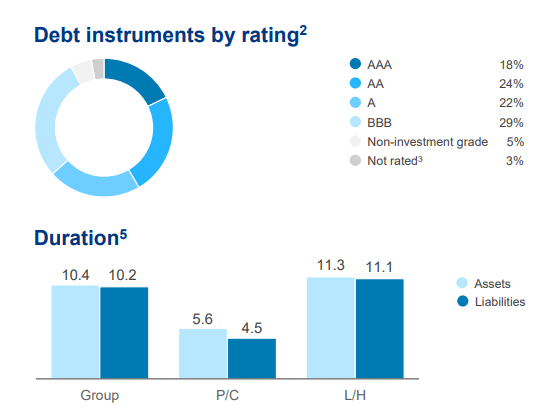

Its investment portfolio is mostly exposed to debt instruments (83%), usually bonds, and 12% equities as well as small real estate and cash positions. Those debt instruments, because it is 83% debt, have the following split. You’ll see why there is little worry here.

Allianz IR (Allianz IR)

The company’s various segments are solid.

One of the initial fears when looking at an insurance business is its reliance on insurance premiums as income when considering the volatility of the industry, especially in light of COVID-19.

Allianz has different dynamics than some of its insurance public comps, which rely on premiums while having a small wealth management arm. Allianz instead earns most of its income from asset management, with only 30% of annual operating income coming from premiums.

Allianz is, in fact, one of the biggest asset managers in the world, which gives it a different risk as well as an earnings profile. It’s similar to Principal Financial (PFG) but better/Bigger.

Allianz is the major shareholder of Pacific Investment Management Company, LLC, or PIMCO, which many of you may know. PIMCO operates as a subsidiary of Allianz following a 2000 takeover. Combining PIMCO operations and AGI operations makes Allianz one of the biggest in all of space, with representation in most nations on earth.

The company did also not cut the dividend during COVID-19, another testament to its resilience not only to the market but to political pressure as well, as the pressure at the time was significant.

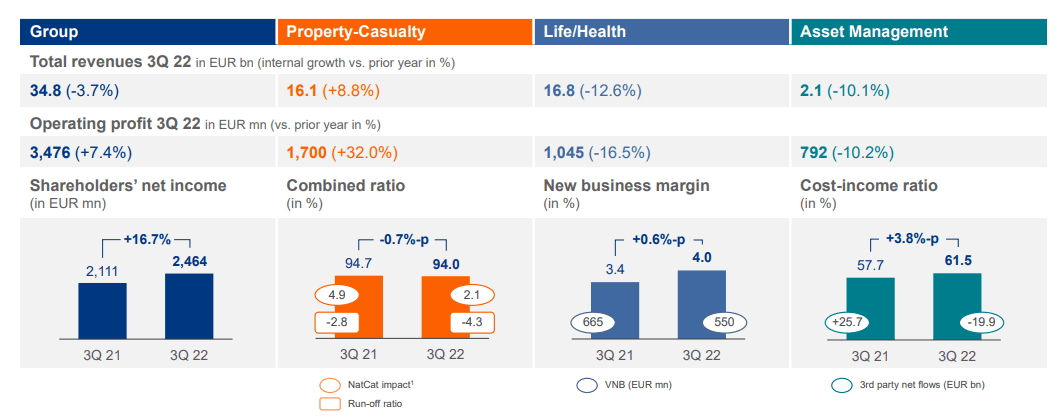

The 9M22 period is the latest results that we have, and they were mostly solid, but with continued impact in life/health and expected trends from the overall broader market, in the state it currently is.

Allianz IR (Allianz IR)

A 9M group operating profit of over €10B means that the company is ending the year well above that mark, the upper half of its target range. There was strong revenue growth at 5%, and a finalization of €1B worth of buybacks in July, at great prices.

P&C was the outperformer, with a 14% improvement in operating profit due to underwriting prudence and investment results, with superb top-line growth. L/H was, as mentioned, trickier, but managed to generate solid investment results under a very challenging environment.

3Q22 YoY was even better.

Allianz IR (Allianz IR)

Fundamentals remain solid. Solvency is very high, and SII capitalization is at or around 200%. The company’s major operational sensitivities are to the equity markets and the overall interest rates – less so to government bonds and non-government bonds.

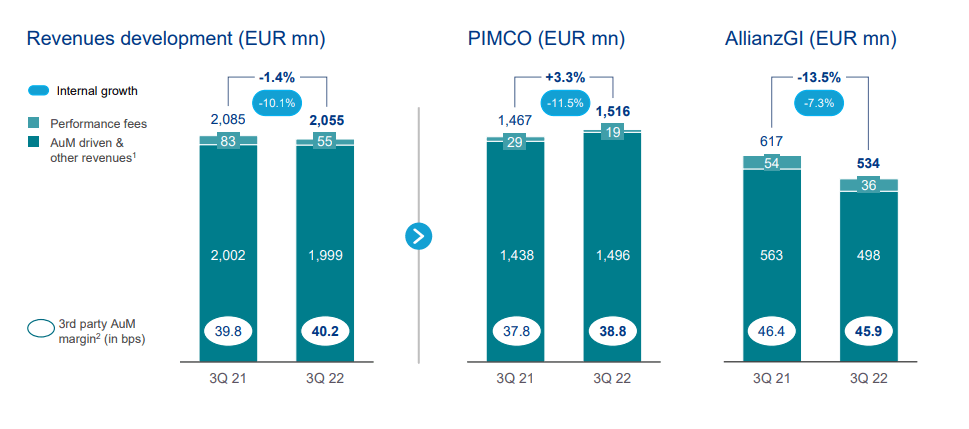

Asset management results are down slightly – but this is to be expected due to the market’s overall volatility. The revenues here are more resilient than the market results would suggest, due to the fee-based structure of the segment, only down in AllianzGI – not in PIMCO.

Allianz IR (Allianz IR)

Here’s the thing about Allianz. The future will not allow for average executions to be sustainable. You’re either an industry winner, or you’re bound for lower growth, overcapacity, inflation losses, digital disruptions, high cost of equity and debt, and increased risks – which will eventually turn to underperformance and defeat.

Allianz is not one of those latter companies – it’s one of the former.

Allianz guides to a forward journey of slight growth, a 5-7% CAGR EPS growth until 2025, and a 1-2% margin expansion based on capturing efficiencies, expanding leadership, and doing some transformative work in some of its franchises.

With an already-market-leading German position at half of the market average costs due to its scale advantages, Allianz has no issues leveraging this to get better returns. Over 10% of the German population are Allianz customers.

The recent quarterly results only confirm how “good” the company is here. You could write books about each of the company’s individual segments, but for now, I will simply state that there are no real fundamental challenges or risks to the company that I personally see. I have always viewed, and continue to view Allianz as one of the absolutely safest plays on the entire planet.

The company is one of the extremely few global businesses that warrant a stable AA credit rating. They maintained this during COVID-19.

However, we’re left with a quandary at this time. What I’m talking about is the company’s valuation.

Allianz Valuation

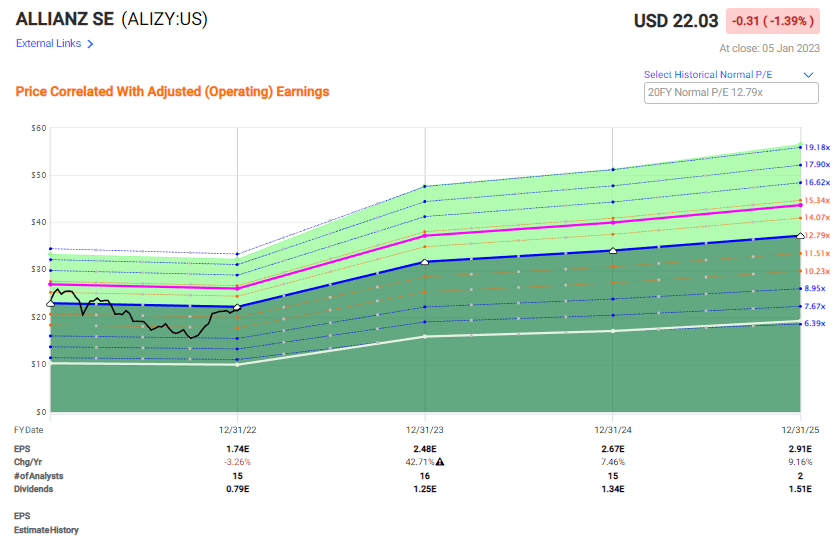

I established my position in Allianz at undervaluation – well below the current 12.6x that we’re almost trading at now. What’s more, 12-13x P/E is the range for the ADR ALIZY, which is the one I typically follow, and the current price is very close to the average share price for the native as well.

I believe Bristol Myers Squibb (BMY) is a very good example of this. Just because valuation dictates that a company should move up, it may take time for it to do so, if it ever does.

Allianz has never traded far above €220/share for the native – not for the past 10+ years at least. But current estimates call for 2023 to be a gangbuster year, which should see the company’s relative valuation of 12.5x rise to almost €300/share or above.

Allianz Valuation (F.A.S.T graphs)

Is the company safe?

Yes, it is.

Should the company rise in tandem with its valuation as results improve?

Yes, it should.

Will it?

That’s another question entirely. Going by actual established earnings for the past number of years, BMY should have normalized to far higher multiples than we’re currently seeing. However, the market takes a much slower pace than we might like – with plenty of dips on the way. That’s why I rotated part of my BMY position the last time it touched above $80/share. There is a historical logic to how high the market at any given time may see a stock rise, and it seems to be correlated to how high it has been before.

Now, if you’re a long-term value investor, you don’t need to care as much as that. However, I mingle what I like to call “active management” in my approach these days. And parts of my Allianz position have delivered close to 40% returns already, or over 200%+ if we annualized it out from when I bought it.

What if I was to rotate that profit and put it towards some attractively-priced cash-secured Puts? What if I reinvested in something cheaper? Because let’s be clear, as much as I love Allianz, it’s not cheap based on current 2022E P/E multiples – only to forward ones.

These are the questions I ask myself when looking at my position. Once, I was a B&H-forever investor. That is something I no longer am. I can still operate within the mindset, and I respect those that do it, but I have evolved – and my approach has evolved with it.

So, you may keep Allianz – and it’s a great choice to do so. There’s upside to the stock. Double digits, but it’s based on forward P/E multiples and EPS growth, not normalization.

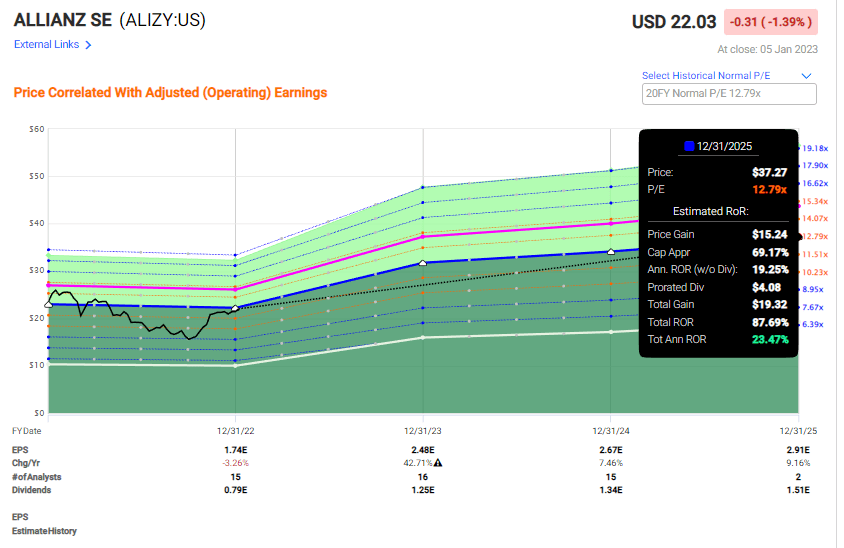

Allianz Upside (F.A.S.T graphs)

S&P Global gives Allianz the following target, with a lower-end range of €200 and a higher of €271, averaging at €235, meaning an upside of about 12.3%, again based mostly on growth forecasts as opposed to normalization. Out of 18 analysts, 11 are at a “BUY” or Outperform rating.

I agree that the company is a “BUY” here – but I don’t agree on the target. I wouldn’t “BUY” this business above €230 at most – there are too much of those future results baked into that. At over €230, there are better and cheaper options in the space while we wait for the valuation of Allianz to normalize.

Based on the company coming out of pandemic trends in good shape, a conservative valuation calls for an embedded value (Embedded value is used outside of NA contexts for valuing insurance businesses, combining the sum of NAV and a discounted PV of future profits) of around €210-€230/share, depending on the exact variables or rates used.

At a 5% Allianz yield, you’re outpacing most of the inflation, and with capital appreciation, you’re usually beating most average markets. You’re doing so at AA credit and with less than a 0.7X 5-year monthly average Beta. Allianz, despite no longer yielding the record 6-7% I bought at, still does that, and because of this, I view it as a continued attractive investment.

However, I also want to call your attention to the fact that I am less exuberant than other analysts, and less so than some of my respected colleagues here – because I see a historical previous “cap” on the share price. Combining that with a triple-digit annualized outperformance for my position, I’m “shopping around”, so to speak.

Questions?

Let me know – otherwise, here’s the thesis!

Thesis

- Allianz is the largest and safest insurance shop on earth – that’s my simple view on the matter. At the right valuation, this one becomes a “must-buy” to me, and I’ve been loading up on Allianz cheaply, to close to 5% of my overall conservative portfolio.

- At this particular time, Allianz is up more than 30% for me, and it’s touching over €210 for the native. I’m still at a “BUY”, but at today’s price, I’m growing more conservative with those targets.

- My PT for Allianz is €230/share – no more than that.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I no longer call Allianz “Cheap”, but it has an upside here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment