maybefalse/iStock Unreleased via Getty Images

Shares of Alibaba (NYSE:BABA) surged last week on reports that Chinese regulators could allow the U.S. Public Company Accounting Oversight Board to inspect audit reports from Chinese companies with overseas stock listings. The news is a big deal for companies like Alibaba which have been subjected to growing concerns over a securities delisting in FY 2021 and FY 2022. With delisting concerns out of the way, investors could start to focus again entirely on Alibaba’s actual e-Commerce performance and considerable free cash flow!

This might be just the regulatory game-changer the market has been waiting for

According to a recent Bloomberg news report, the China Securities Regulatory Commission is said to work on a framework that would allow U.S. regulators to inspect the books of more than 200 Chinese companies with ADR listings in the U.S. Granting the U.S. Public Company Accounting Oversight Board full access to audit reports of Chinese companies could put to bed a contentious issue that has plagued Chinese companies with ADR listings in the United States, like Alibaba, for more than a year. Chinese companies only present unaudited financial statements to foreign shareholders, opening them up to criticism about a lack of transparency. Investors buying U.S.-listed ADRs have no assurances that the financials Chinese companies submit can be relied upon.

For more than a year, many investors have been fearful to touch Alibaba’s ADRs, in part because Beijing was cracking down on Chinese companies with overseas securities listings. While I considered Alibaba’s ADR delisting risk to be minuscule all along — largely because it is not in Beijing’s interest to cut off its own companies from the ability to raise foreign investor capital — investors can now feel reassured that the U.S. and China are moving towards an amicable solution regarding audit inspections.

The news is a big deal for Alibaba and other Chinese companies with ADRs trading on U.S. stock exchanges. This is because the Securities and Exchange Commission listed five Chinese companies — including Yum China, BeiGene, Zai Lab, ACM Research and HUTCHMED — as possible delisting candidates a short while ago which sparked another sell-off in Alibaba’s ADRs.

Beijing’s concessions to the U.S. are a positive step in the right direction and a mutually-agreed on framework for audit inspections clears the way for growing investor interest in Alibaba’s e-Commerce empire and significant free cash flow value.

Growing e-Commerce empire and free cash flow

The biggest reason to buy Alibaba relates to its incredible free cash flow value and the most recently announced $25B share buyback. Alibaba’s free cash flow remains largely ignored and I believe it has a lot to do with delisting fears that have weighed on Alibaba’s ADRs.

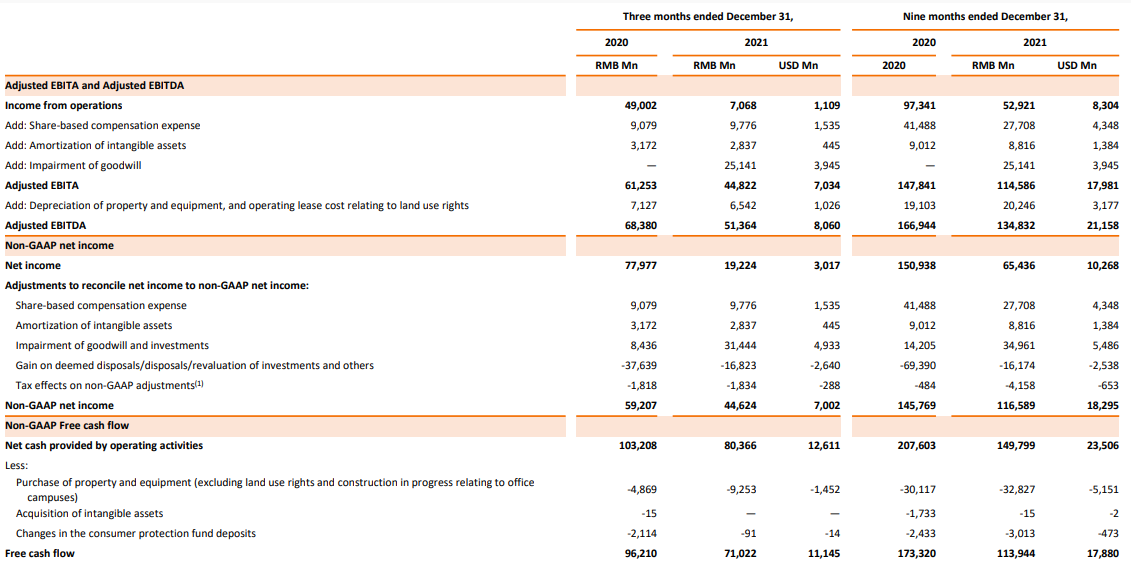

In the first nine months of FY 2022, Alibaba generated 113.94B Chinese Yuan in free cash flow which calculates to $17.9B. Alibaba could generate up to $28.0B in free cash flow next year and achieve free cash flow margins close to 20%.

Alibaba

Alibaba recently upsized its share buyback from $15B to $25B which is a considerable amount of cash that will be returned to shareholders in the next two years. The firm’s top line is also expected to keep growing, although at a smaller rate than in the past. We are likely going to see around 20% top line growth for Alibaba annually in the foreseeable future.

With margins of around 20%, regarding free cash flow, shares of Alibaba still remain fundamentally undervalued… and the collaboration regarding audit inspections could clear the way for a higher valuation of Alibaba’s shares going forward.

Alibaba’s current market price implies a free cash flow valuation factor of just 8.6 X. The P-FCF ratio has been calculated by adjusting Alibaba’s market cap of $300B for its considerable net cash position of $59B and dividing it by my free cash flow prediction of $28B for FY 2023.

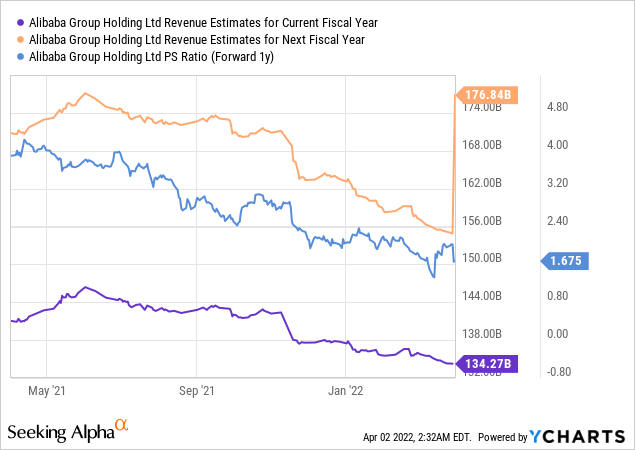

Based off of just sales expectations, shares of Alibaba have a market-cap-to-revenues ratio of 1.7 X, which is significantly below the sales multiplier factors achieved a year ago.

Risks with Alibaba

As I have said along, the ADR delisting risk has been widely blown out of proportion and Alibaba and other large Chinese companies with ADR delistings in the U.S. are unlikely to see their shares getting delisted. The most recent developments are highly encouraging. However, this is not to say that Alibaba doesn’t have any risks. The biggest risk for Alibaba remains a slowdown in top line growth longer term, especially in its e-Commerce business which is still responsible for 70% of the firm’s revenues. Lower free cash flows and declining free cash flow margins also represent risks for Alibaba and the stock going forward.

Final thoughts

I suspected that the U.S. and China would reach an agreement on audit checks. The most recent report from Bloomberg suggests that U.S. and Chinese regulators work on a mutually beneficial solution to keep ADRs of Chinese companies tradable in the U.S. Beijing is making big concessions here and I believe it will ultimately benefit Alibaba as well as other Chinese Big Tech companies. With ADR delisting concerns out of the way, investors can now try to focus on Alibaba’s actual commercial performance and free cash flow again.

Be the first to comment