Dzmitry Dzemidovich

AGNC Investment Corp. (NASDAQ:AGNC), a mortgage REIT (real estate investment trust), has been the subject of great debate in recent months. On the one hand, the company’s 13.5% annual yield, with monthly dividend payments, is extremely attractive for most types of investors to have in their portfolio. On the other hand, the fact that interest rates are heading higher and are likely to remain high-ish for the coming few years is likely to continue and hurt the company’s book value and their ability to maintain that dividend payout.

The company has successfully employed hedges against these interest rate rises, which resulted in a strong performance in the most recent quarter, which showed a dividend payout ratio of just 46%. But it does indeed mask the issue of their dividend sustainability.

So the question in my mind, as an AGNC holder, is whether the company can continue to use the short term hedges and other cash to maintain their relatively high dividend payouts until the U.S. federal reserve begins lowering interest rates and the NAV of the mortgage REIT begins to increase.

Some Of The Best Payouts

AGNC Investment has one of the best payout structures in the stock market today. While I’ve had AGNC Investment for several years now, I really began amassing a larger position over the past year or so when their share price cratered during and after the COVID-19 pandemic, which boosted their annual dividend yield to around 15%.

The cherry on the cake is that the company pays out this dividend payment on a monthly basis. This increases both short and long term incentives of holding a stock position.

In the short run, the monthly payouts allow short term folks to get paid around 1% a month on whatever cash they have invested. While this is not a long-term strategy given the relative volatility in their dividend rates, it’s an excellent short-term strategy if you’re able to nag the company’s share when they yield over 13.3% or so where you’d earn 1% monthly after dividend tax.

In the long run, it increases the overall return a bit. Again, this is before the discussion about dividend sustainability, but if we assume it will remain within a certain range, it provides for better returns than a quarterly or annual yield. Given the classic investment scenario I like to use – if you invest $100 and then subsequently invest $50 a month in AGNC over the course of a 25 year investment plan, you’d make about $4,000 more at the end of that period.

Given these two factors, the company has been perceived as a very attractive investment over the past 2 years or so, even if the underlying fundamentals have been a bit sketchy.

Headline Fundamentals Mask Headwinds

While folks were piling into AGNC Investment over the past few quarters and year, the company reported extremely high and relatively unsustainable payout ratios. This means that they were paying out more in dividend on their shares than they were bringing in through interest fees on their mortgage securities.

But then came the most recent quarter when their hedges kicked in and they reported a large bump in earnings, resulting in a roughly 46% payout ratio. While that has happened, and most dividend ratings now state a “46% payout ratio,” the company is projected to lose even more book value and earnings.

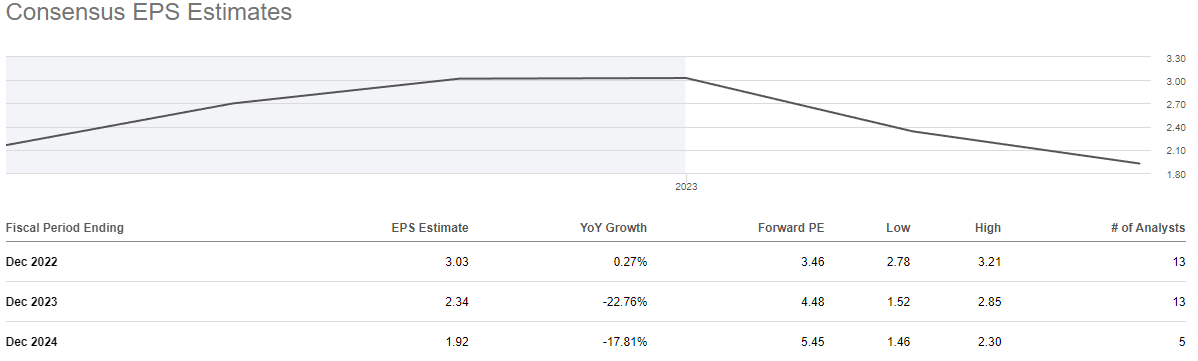

After reporting an adjusted EPS of $3.03 for the year, the company is projected to report low double digit declines over the next 2 years before an expected rebound, which mostly coincides with the expected decline in the federal funds rate, which I’ll discuss in the next section of the article.

AGNC EPS Projections (Seeking Alpha Aggregator)

The question remains whether AGNC Investment will be able to maintain their dividend payouts as higher interest rates hurt both the NAV of mortgage REITs and their ability to generate enough interest income to pay this dividend.

Risk Reward Profile Is A Lucrative 50-50

The prospects of the company maintaining a dividend high enough to remain attractive to both existing investors and potential new ones is more or less a coin toss.

The pessimistic view is that there is a historical precedent for them cutting the cash amount of dividends as NAV of mREITs decline and their interest income earnings struggle. This means that if they report a 25% decline in earnings over the next 2 years, they’d report a 25% cut in dividends to make sure they remain ok for the longer run.

This will result in a dividend yield under 10%, which, while it being a high yield relative to the broader market, can make the risk-reward unappealing to those who don’t have a high degree of confidence in the housing and mortgage markets, which get hurt in recessions and housing market corrections.

The optimistic view says that the company can and should lower their dividend in order to maintain a healthier balance sheet and value but can manage to do so without creating pain for existing or new investors. They have the ability to continue and use the hedges to generate meaningful negative interest expense, which will boost their earnings and use their cash on hand to sustain their dividends until earnings and value picks back up.

Let’s Focus On The Positive

While the negative elements of the this thesis are serious, I won’t bore you with them since they’ve been covered extensively by other Seeking Alpha contributors over the past few months. My favorite and most recent article is by Johnathan Weber, titled AGNC Investment: Be Fearful When Others Are Greedy. I believe it perfectly and most accurately encapsulates the risks and negative sentiment surrounding the sustainability of AGNC’s dividend.

On the positive side of things, however, there are 2 main factors I’m considering while positioning my investment for the next year or 25:

Fed Dot Plot Is Favorable-Ish

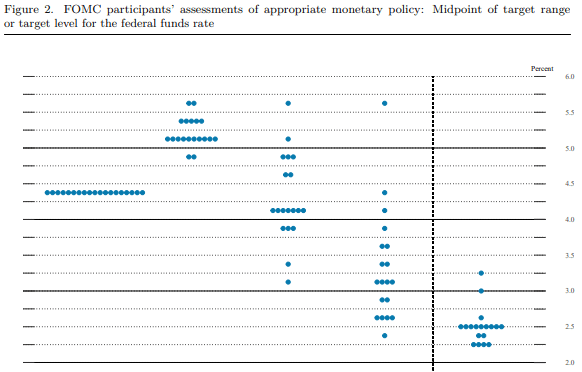

While high interest rate hurt the NAV of a mortgage REIT, the relatively sky high interest rate environment we’re in right now is not projected to persist for all that long. In the federal reserve’s latest meeting on December 14th, 2022, they released their most updated dot plot, which lays out where they expect interest rates to be over the next 3-4 years.

Through 2025, they project the average interest rate to go down to about half where it is today, which should be favorable for mortgage REITs.

Fed Dot Plot (Summary of Economic Projections)

After the average interest rate is expected to stay around the 5% to 5.5% mark for a bit, it’s projected to be lowered to prevent overheating and given the fact that inflation isn’t projected to persist as long. This means that the company should, key word should, see higher value and interest earnings heading into 2025.

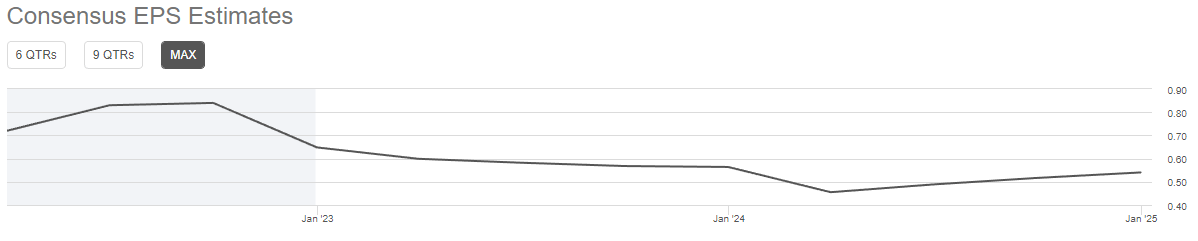

That’s what analysts project as well. After reporting declines in quarterly earnings per share (adjusted), they’re projecting a return to growth in the quarters in 2025:

AGNC EPS Projections (Seeking Alpha Aggregator )

This brings me to point number 2.

They Can Sustain Payments… Ish

The company pays out $1.44 in dividends per year, or around $850 million. While that figure may be steep given the losses they report on a GAAP basis, they can certainly sustain that over the next 2 to 3 years until they return to growth with lower interest rates. They still have hundreds of millions of dollars in trading asset securities as hedges against interest rate rises and have almost $1 billion in cash and equivalents, which can help sustain their payouts.

This means that they company will only have to go into the red for a year or so of dividend payments, and that’s without any decline in dividend amounts, which they have done in the past.

I do believe that the company can cut their dividend amount by 10% or so and it will help them maintain their business as interest rates begin to decline in the coming year or so. That will, I believe, allow investors to maintain their positions without readjusting too much with the lower yield.

Investment Conclusion: 50-50 Risk Reward

A new investment in AGNC Investment Corp. right now may tilt a little riskier, while an existing investment at a lower price point may be a good and sustainable one.

I believe that while the company is likely to see a continued decline in the value of their assets, and while I hope they cut their dividend payouts by 10% or so to make sure they can sustain the rest of it until income and value grows again in early 2025, AGNC Investment still presents one of the best dividend plays for 2023 and beyond.

We’re likely to see some form of continued share price pressure over the coming months for AGNC Investment Corp., and likely more so IF they do indeed make a cut to their payouts. That, I believe, will be a good opportunity to add some to a position in order to take better advantage of later years once it’s all priced in.

I am slightly bullish on AGNC Investment Corp. heading into 2023 and I will be looking for dips in the company’s share price below $9.00 to $9.50 per share to buy more shares and hold for the 25 year period my retirement account is geared to.

Be the first to comment