Alan_Lagadu

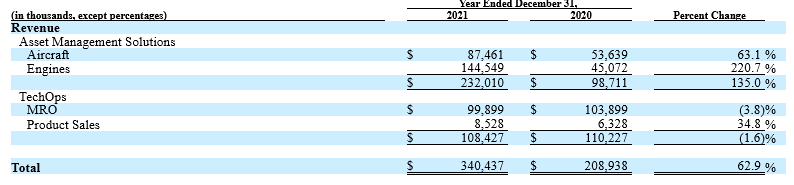

AerSale Corporation (NASDAQ:ASLE) supplies the aviation industry in two segments, leasing of engines and aircraft, and a service side. It is a founder-led company with around 22% insider ownership. Will industry turnaround be the tide that lifts this boat? Below is a breakdown of revenue by segment.

ASLE 10-K

The company was founded in 2008 and went public in 2019, not a great year to IPO considering how badly the airline industry was hurt.

dividendchannel

The entire industry has yet to recover from Covid-19, yet ASLE remained profitable throughout. They did receive assistance from the government during the crisis, and as a condition of the financial aid, they have been prohibited from paying dividends or repurchasing shares until September of this year. Revenue has basically been flat over the past four years, but obviously the pandemic affected this, so it’s hard to determine exactly where sales would be in a scenario without Covid-19.

Below are tables comparing margins and return metrics with peers:

|

Company |

10-Year Median ROE |

10-Year Median ROIC |

10-Year EPS CAGR |

10-Year FCF CAGR |

|

ASLE |

8.9%* |

7.7%* |

n/a |

13%* |

|

9.2% |

2.6% |

19.7% |

n/a |

|

|

10% |

3.7% |

22.9% |

n/a |

|

|

9.2% |

4.6% |

16.1% |

n/a |

*4-year

|

Company |

Gross Margin |

Operating Margin |

Net Margin |

|

ASLE |

35% |

16.6% |

10.6% |

|

AL |

35.6% |

15.8% |

-6.9% |

|

ATSG |

55% |

17.8% |

13% |

|

AAWW |

58% |

17.2% |

11.5% |

ASLE has yet to establish a long track record of returns on capital, but there could be a potential trend upwards if the 2021 numbers are any indication. I don’t think this is likely due to the uncertainty of the airline industry overall. Operating margins impressively tripled from 2020 levels, but this won’t likely be continuing.

|

Year |

2018 |

2019 |

2020 |

2021 |

|

Gross Margin |

24.8% |

27.9% |

25.2% |

35% |

|

Operating Margin |

8.7% |

7.2% |

5.4% |

15.6% |

|

Net Margin |

3% |

5% |

4% |

10.6% |

|

ROE |

n/a |

5.3% |

2.4% |

8.8% |

|

ROIC |

n/a |

5.9% |

2.8% |

18.4% |

Capital Allocation

As mentioned, dividends and buybacks have been prohibited as a condition of taking financial assistance from the government. Even if there had been no pandemic, though, ASLE is not at the stage where it needs to return capital to shareholders. They are better served by acquiring more assets or related businesses. There is essentially no debt on the balance sheet, so the use of some to obtain assets that add to cash flow wouldn’t be irresponsible at this point.

Valuation

Below is a table showing relative pricing on a multiples basis:

|

Company |

EV/Sales |

EV/EBITDA |

EV/FCF |

P/B |

|

ASLE |

1.6 |

8.3 |

5 |

1.9 |

|

AL |

9.1 |

12.6 |

-10.5 |

0.6 |

|

ATSG |

1.8 |

4.9 |

28.6 |

1.6 |

|

AAWW |

0.6 |

2.4 |

4.2 |

0.6 |

Forecasting future cash flows for ASLE is difficult mostly due to the unpredictability of air travel. The biggest risk lies in the industry, not with any particular weakness the company has. The multiples aren’t low enough to make this a screaming bargain at all. Should the business recover along with the industry, this could be a decent starting point as shares are close to fairly priced. I’ll wait to see how the industry recovers and how ASLE executes in the meantime. I really like the fact that the company is still founder led, and they still have significant insider ownership.

Conclusion

ASLE serves an important function that most airlines don’t want to deal with. They’ve been able to survive through the pandemic, in part through government assistance, but their future success depends largely on the performance of the airline industry as a whole. Capital allocation isn’t vital at this point as they need to grow their cash flows much more before returning anything to shareholders. There was a huge margin expansion from 2020 to 2021, but being able to sustain those numbers isn’t likely.

There is no huge discount to be found as far as pricing, and future uncertainty of the industry makes forecasting quite difficult. Being founder led with a high rate of insider ownership is a great attribute, but that fact isn’t enough to discount fairly priced shares and risk associated with the still-recovering industry.

Be the first to comment