vzphotos

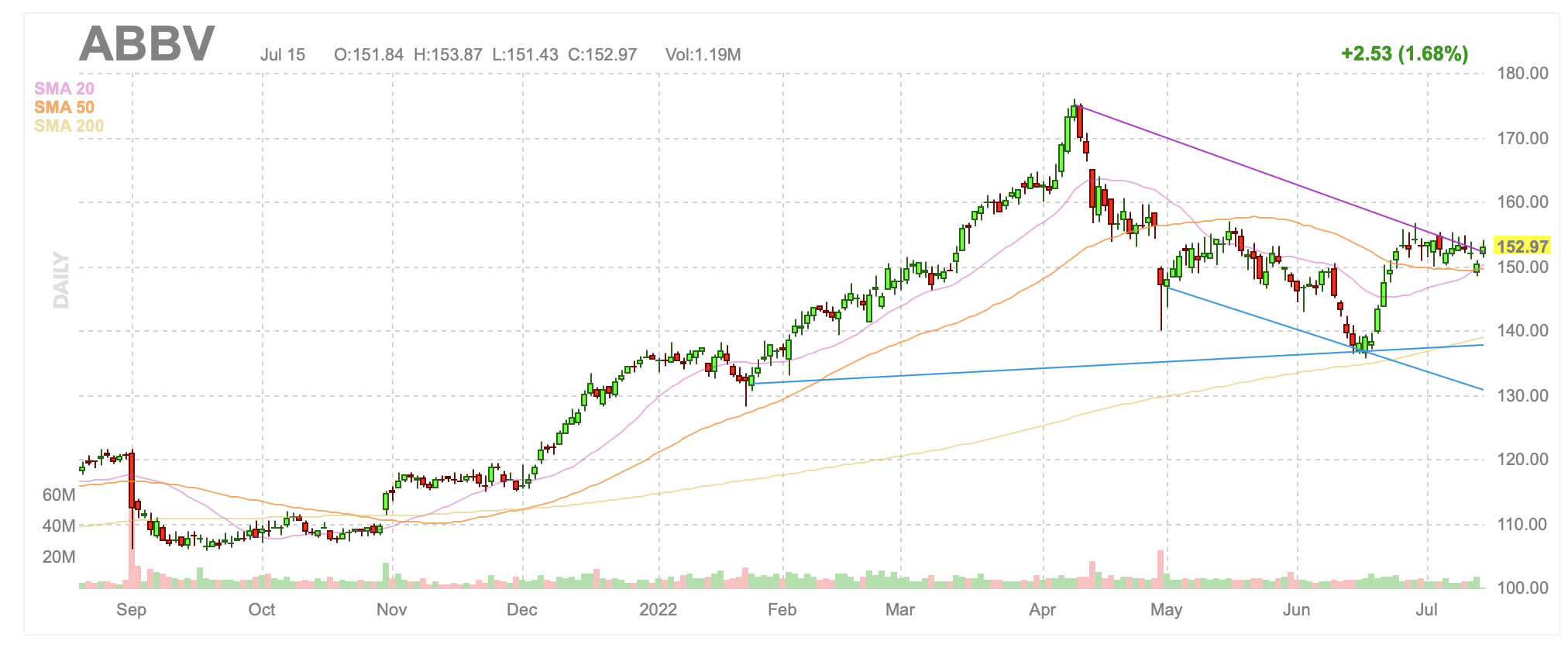

AbbVie (NYSE:ABBV) may be breaking out again. The company was considerably undervalued for several years, but broke out last year and through the first quarter of 2022. Since peaking in early April, the company has been in a sustained downtrend that was exacerbated by both Q1 earnings and broader market weakness. I believe that AbbVie just broke out of that downtrend, and that its multiple expansion phase is ready to resume.

AbbVie daily candlestick chart (Finviz)

I believe that this down period since that early April peak will end up looking like a bull flag. I think it clearly overshot itself in April, but then similarly overshot to the downside in mid-June, where it seemed to touch longer term support, only to bounce hard and fast from around $140 to around $150. It has remained in a tightly wound range over the last few weeks, but recent strength seems to be taking it out of that range, as well as out of that downturn altogether.

AbbVie is a Dividend Aristocrat that is likely to increase its quarterly payout every year, and generally in the fall. AbbVie is also a regular repurchaser of shares. Further, AbbVie’s fairly consistent domestic cash flow should be desirable in this strong dollar environment. Those flows and that dividend should support share prices going forward.

In early July, AbbVie noted that its Q2 and fiscal year 2022 results shall be negatively impacted by in-process research and development (IPR&D) costs due to acquired assets and milestone expenses that would be around $269 million on a pre-tax basis in Q2. AbbVie’s filing also updated guidance for Q2 EPS of $3.24-3.28, down from $3.38-$3.42. Similarly, full year 2022 EPS guidance was lowered from a range of $13.92-$14.12 to a reduced range of $13.78-13.98, excluding non-recurring items.

This was the second time AbbVie lowered guidance this year, where it also did so in April when it provided Q1 earnings. At that time, AbbVie was hammered for it, but this more recent update hardly affected the stock price. Further, the stock has performed well since then, indicating the market is reasonably comfortable with the valuation and probable details to be provided when AbbVie reports earnings on July 29, before the market opens.

AbbVie’s continued dependence upon Humira remains its most frequently discussed risk. In Q1, AbbVie entered into an agreement with Alvotech Holdings (ALVO) to settle a patent and trade secret dispute related to Humira. According to the disclosed terms, Alvotech obtained the non-exclusive right to market its high-concentration biosimilar candidate for Humira, AVT02, in the United States, with a license entry date of July 01, 2023.

This biosimilar competition has been seen as an inevitability for quite a while, but AbbVie has been quite capable of extending the drug’s market and revenue strength. Humira’s market share and revenue will inevitably weaken, but it remains a powerhouse drug that is still projected to have billions in revenue per quarter for the next couple of years.

AbbVie’s ability to extend the longevity of Humira has been consistently underestimated, which is part of why the company has remained undervalued compared to actual performance. Humira brought in about $20.7 billion worth of sales in 2021, which was roughly 37% of AbbVie’s total annual net revenue last year.

AbbVie also continues to benefit from its 2019 acquisition of Allergan, which was under-appreciated by the market. Allergan gave AbbVie some much needed diversification. Prior to the acquisition, AbbVie was primarily dependent upon Humira, but Allergan also brought multiple new profitable drugs into the portfolio.

Allergan was probably best-known for its aesthetic and/or cosmetic treatments, including Botox, Juvederm, and CoolSculpting, all of which continue to perform well. Allergan also had a neuroscience division that included Vraylar, which is the fastest-growing domestic atypical antipsychotic, and is likely to become a blockbuster in the near term. Allergan also brought with it over $2 billion in eye care related revenue, and almost $2 billion in gastrointestinal revenue. Allergan also included a women’s health division that was differentiated from AbbVie’s existing portfolio.

Of course, the fact that AbbVie brings in so much revenue within the United States often makes it a target for political scrutiny. For example, in 2021, the House Oversight Committee scrutinized the company’s use of patents in order to extend Humira’s protection from competition. Similarly, last year, the Senate Finance Committee demanded information on AbbVie’s use of international corporate domiciles and tax law. The same thing happened again recently.

Earlier this month, Senate Finance Committee Chair Ron Wyden issued an interim report on tax practices that focused on AbbVie. The document argues that AbbVie uses tax havens to minimize its U.S. tax obligation. Wyden asserts that even though over 75% of the company’s annual 2020 sales were domestic, only 1% of AbbVie’s income was reported as domestic for tax purposes.

The report also notes that AbbVie benefitted from the tax law signed by former President Trump in December of 2017, where its effective tax rate dropped from around 22% between 2015 and 2017, AbbVie paid a 22% effective tax rate that dropped to 8.7% in 2018, 11.2% in 2020, and 12.5% in 2021. This report is more of a political campaign argument than an indictment of AbbVie, which it appears is merely an effective user of tax laws as they were written.

It is often the case that large pharmaceutical companies underperform in the weeks and months in advance of a domestic election. This is generally because of the risk that a change in control might make drugs a greater target, but mostly because such claims are often used as campaign promises. Any such weakness is usually a buying opportunity.

Conclusion

ABBV provides a well-covered dividend that is likely to be increased in the fall. AbbVie substantially outperformed the market in early 2021, but it fed out of favor in Q2. Since then, shares bounced off of strong support at around $140 per share, and have since hovered around $150. AbbVie now appears to be breaking out of its recent tight trading range, which should subsequently act as a new level of support.

Be the first to comment