sefa ozel/iStock via Getty Images

Energy Transfer (NYSE:ET) has generated very impressive total returns year-to-date for unit holders, especially when compared with the broader market (SPY):

Despite this run-up in its unit price, it still sports a clearly discounted valuation according to several metrics:

| MLP | P/DCF 23E | EV/EBITDA | EV/EBITDA (10-Year Average) |

| ET | 4.49x | 7.78x | 11.29x |

| EPD | 7.12x | 9.11x | 12.82x |

| PAA | 4.54x | 8.91x | 10.78x |

| MPLX | 6.56x | 9.17x | 12.36x |

| MMP | 8.33x | 10.36x | 11.06x |

On top of that, ET also has significant distribution growth potential in the near future. As per management’s ongoing narrative thus far in 2022, one of ET’s top priorities is restoring the quarterly distribution to the $0.305 level where it was prior to the COVID-19 crash cut of 2020. Given that ET is already generating more than enough cash flow to pay out such a distribution, it seems like they should be able to restore it to that point sooner rather than later. As a result, further outperformance for ET common units seems likely.

While the valuation and total return proposition certainly looks enticing, ET’s credit rating is weaker than some of its more expensive peers. AT a BBB- credit rating from S&P, ET trails EPD’s and MMP’s BBB+ credit ratings and MPLX’s BBB credit rating. With a meaningful recession increasingly likely in the coming months, ESG sentiments increasingly pressuring energy companies’ access to capital, and interest rates soaring higher, assessing ET’s balance sheet strength is a critical part of the investment thesis. In this article we do a deep dive into its upcoming debt maturities to get a better sense of how well positioned it is for this increasingly challenging environment.

A Look At ET’s Upcoming Debt Maturities

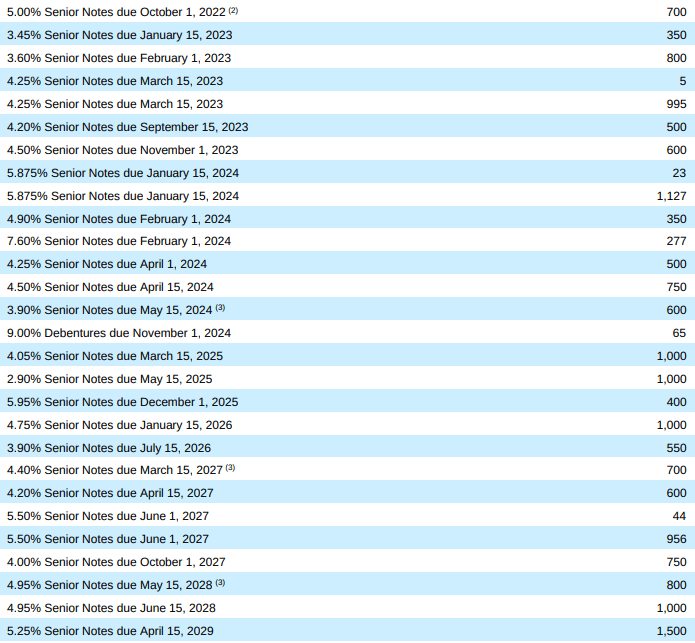

Based on ET’s 2021 10-K and assuming they continued their year-to-date practice (on the Q2 earnings call management said: “we expect to continue to pay down debt throughout this year and beyond with excess cash flow from operations“) of redeeming debt as it matures (i.e., paying off the October 1, 2022 5% senior notes as they came due), they have $14.642 billion in maturing debt over the next five years:

Upcoming Debt Maturities (ET 2021 10-K)

Fortunately, it is well-laddered over that time frame, with no more maturities in 2022, $3.25 billion maturing in 2023, ~$3.7 billion maturing in 2024, $2.4 billion maturing in 2025, $1.55 billion maturing in 2026, and $3.05 billion maturing in 2027. ET’s weighted average interest rate is low enough that it is unlikely to generate any interest rate savings if it had to refinance its debt given that its 2030 maturing bonds are currently trading at an over 5% yield to maturity. However, it is also unlikely to lose much with higher interest rates on most of its maturing debt.

Using expected annual capital expenditures of between $2.5 billion and $3 billion, ET is expected to generate about $6.5 billion in free cash flow per year moving forward based on analyst projections through 2026. That translates to roughly $1.80 per unit in free cash flow. Given that analysts are currently projecting that ET restores its distribution to its pre-cut level of $1.22 per year in 2023, that leaves just under one-third of ET’s free cash flow net of distributions for debt reduction. This amounts to about $2 billion per year in free cash flow net of distributions.

On top of that, management stated on its Q2 earnings call that it had significant liquidity through its revolving credit facility:

As of June 30, 2022, total available liquidity under our revolving credit facility was approximately $2.44 billion.

When combined with the well over $1 billion in excess free cash flow that ET should be generating net of distributions in the second half of 2022, ET is expected to be capable of bringing to bear over $7.5 billion in total liquidity through 2024 without having to cut CapEx and paying out a full $1.22 per unit distribution in both 2023 and 2024.

That exceeds their total debt maturities during that period by over $0.5 billion (in fact, it could be closer to $1.5 billion depending on how much free cash flow ET generates in the second half of 2022), giving the company some wiggle room in the event that commodity prices and/or other industry factors underperform current consensus estimates. Note that ET can also cut and/or delay some of its CapEx if it needs to in order to pay down debt as it matures.

However, several of ET’s 2024 maturities have quite high interest rates assigned to them, so those should be pretty easy for ET to refinance at comparable or even better interest rates, barring a significant further spike in interest rates, so that could likely further increase their capital flexibility over the next several years.

Looking out into its 2025 and 2026 debt maturities, ET should be able to generate sufficient free cash flow in those years as well to fully redeem those debts as they mature if it so wishes. However, there is plenty of time between now and then for ET to take advantage of any decline in interest rates to refinance that debt as well if it wants to.

Investor Takeaway

Based on our analysis in this article, ET’s expected free cash flow generation over the next half decade should be sufficient to fully redeem upcoming maturities while still providing sufficient cash flow to fund the fairly substantial capital expenditures budget and fully funding the restored distribution level.

This puts ET in remarkably strong financial condition as it means that ET has little to no dependency on the capital markets as we enter a period of increasingly challenging capital market conditions for midstream businesses. ET should be able to fully meet all of its debt and equity obligations for the foreseeable future without having to depend on the interest of bond or equity investors. As a result, it enjoys a fairly low-risk financial profile, provided of course, that its business continues to generate fairly stable cash flow.

It is also worth noting that management expects to achieve its leverage ratio target by the end of 2022, stating on the Q2 earnings call:

We also expect to reach our leverage target range by the end of this year

This means that the leverage ratio is close to hitting – or possibly already at – its 4.5x target level, which further adds weight to the argument that ET’s balance sheet is in solid shape to weather any long-term challenges.

We are reiterating our Strong Buy rating on ET as we view it as offering a highly compelling risk-reward proposition to investors.

Be the first to comment