Natali_Mis

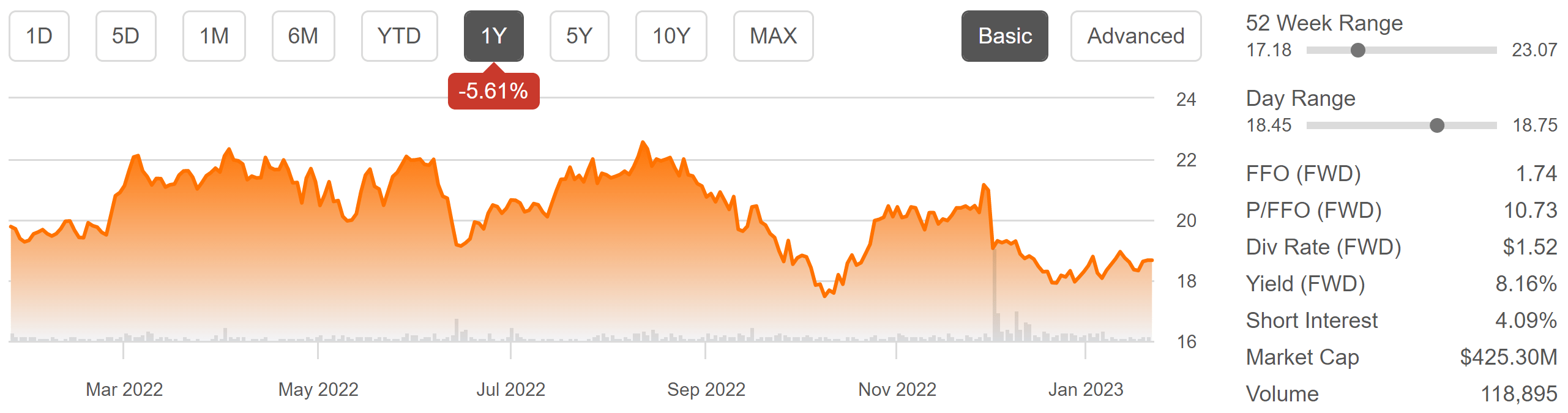

There remains plenty of high yielding bargains despite the recent market rally, which has mostly affected tech stocks. One such high yielder is CTO Realty Growth (NYSE:CTO), which as shown below, remains well below its 52-week high of $23 and hasn’t really budged in price since the start of the year. In this article, I highlight why CTO is a growth name that’s worth looking into at current levels, so let’s get started.

CTO Stock (Seeking Alpha)

Why CTO?

CTO Realty Growth is a REIT that owns and operates single and multi-tenant retail and office properties with strong fundamentals. Notably, it also acts as the external manager for the net lease REIT, Alpine Income Property Trust (PINE), in which it has a 16% equity ownership stake. This arrangement results in a stable stream of management fee income for CTO.

CTO is focused on acquiring properties that are selling for below market rates, then leasing up the properties through various ways to unlock value. This is exemplified by CTO’s Ashford Lane investment that’s 78% occupied and more than 85% leased, with more than a dozen new tenants that have opened or will open in the coming months. This strategy continues to work well for CTO, as saw robust 12% YoY same property NOI growth during the third quarter. Moreover, CTO has added grocery-anchored properties and is recycling capital through accretive dispositions of lower yielding and non-core properties.

This includes the recent acquisition in October of West Broad Village, a mixed-use and grocery-anchored lifestyle property in Richmond, Virginia with a going-in cap rate above CTO’s prior guidance for initial cash yields, and the disposition of two non-core multi-tenant office and retail properties for a weighted average exit cap rate of 6.3%.

This strategic positioning contributed to the doubling of CTO’s grocery-anchored asset exposure to nearly 30% of the portfolio and increased its overall retail and mixed-use portfolio to nearly 90%. This also leaves CTO with just one remaining office property in Jacksonville, Florida. Importantly, CTO’s new investments are anchored by high quality tenants such as Whole Foods (AMZN), HomeGoods (TJX), Publix, REI, Ross Stores (ROST), and Best Buy (BBY).

Looking forward, CTO should continue to benefit from strong tenant demand, as it recently saw 8% lease spreads and meaningful demand for its high-quality locations. Having said that, CTO is also not without potential headwinds, with some tenants that generate headline risk, which management noted during the last conference call:

All of our successes are not without some challenges. We’ve been notified that the WeWork location at our Shops at legacy property in Plano, Texas will be going dark before the end of the year. We have a corporate guarantee in place that should make the anticipated client needed to find a replacement tenant. It will take some time and effort to find the right tenant, we believe we can find a productive backfill that will benefit the property given the strength of the market.

Additionally, we do have on Regal theater in the portfolio at our Beaver Creek Crossing property outside of Raleigh, North Carolina. We’ve been in dialogue with their representatives and they are currently no indications that our lease will be rejected in bankruptcy. However, given that the box is separately parceled in the Raleigh market is one of the fastest-growing most in-demand markets in the country. We believe we have an attractive set of alternatives available to us, should they decide to vacate the space.

Nonetheless, CTO has plenty of liquidity at $200 million to work through potential challenges, and it also maintains a reasonable amount of leverage for its growth nature, with a net debt to EBITDA ratio of 6.4x and healthy fixed charge coverage ratio of 3.4x.

Importantly, CTO is rewarding shareholders, with its last paid quarterly dividend of $0.38 being 13% higher than it was in the prior year period. The dividend is also well-covered by a 78% AFFO payout ratio.

Lastly, I see value in CTO at the current price of $18.66 with a forward P/FFO of just 10.7, resulting in an attractive 8.2% dividend yield. I find the current valuation to be too low considering CTO’s portfolio transformation and its strong growth profile. Analysts also have a consensus Strong Buy with an average price target of $22.50, implying a potential one-year 29% total return including dividends.

Investor Takeaway

CTO Realty Growth is transitioning its portfolio to focus more on grocery-anchored and mixed-use properties. This transition has enabled CTO to increase the quality of its asset base and capitalize on stronger tenant demand for these types of properties.

Furthermore, investors are being rewarded with an 8.2% dividend yield that’s well-covered by AFFO. Admittedly, CTO is not a premium quality REIT like Realty Income (O) or W. P. Carey (WPC), but it could be a good high income pick for risk tolerant investors in a well-diversified portfolio.

Be the first to comment