alphaspirit

This article was co-produced with Cappuccino Finance.

It’s hard to maintain trust and focus during times of volatility, even though this is the time that you most need the trust and focus. 2022 has certainly been a testing ground for investors.

With bad news following bad news, and underlying inflation troubling people at the grocery store and stock market alike, it has been difficult to keep faith in our investments.

Now the Fed has dashed more cold water in the face of investors with their resolve to stay aggressive on inflation. The light at the end of the tunnel seems like it just got a little dimmer.

In times like these, the following three real estate investment trusts (“REITs”) will give you some peace of mind over the holidays, knowing that your money is safe and working hard for you. The dividends will keep on flowing and allow you to steadily build your wealth.

Invitation Homes Inc. (INVH)

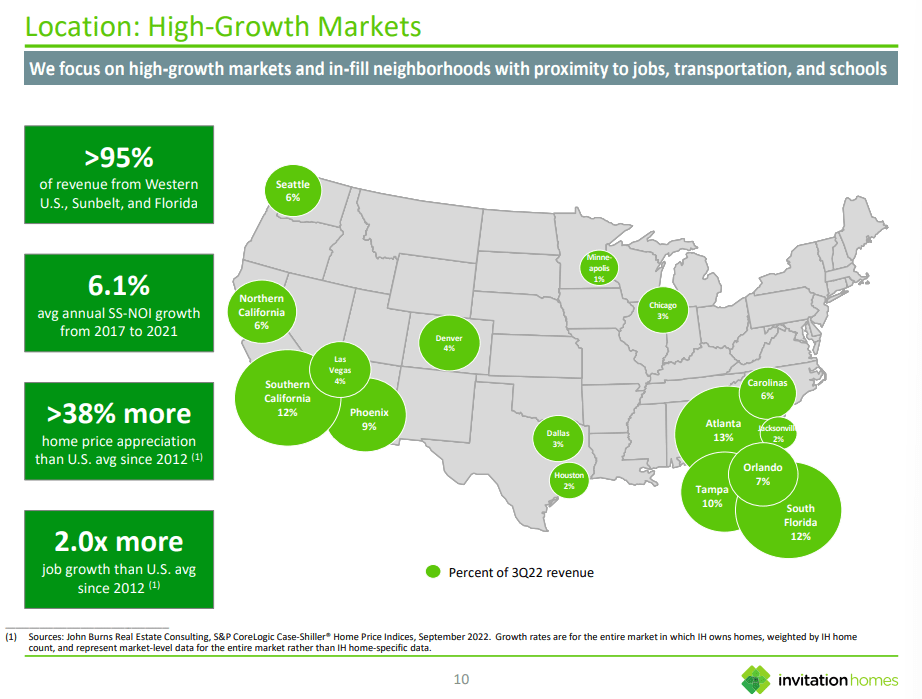

Invitation Homes is a leading owner and operator of single-family homes for lease, and they offer high-quality homes in high demand neighborhoods across America. They have over 86,000 homes in their portfolio, and their properties are in high demand.

The average resident satisfaction score for their houses was 4.3/5, and the same resident average occupancy rate was 97.5%.

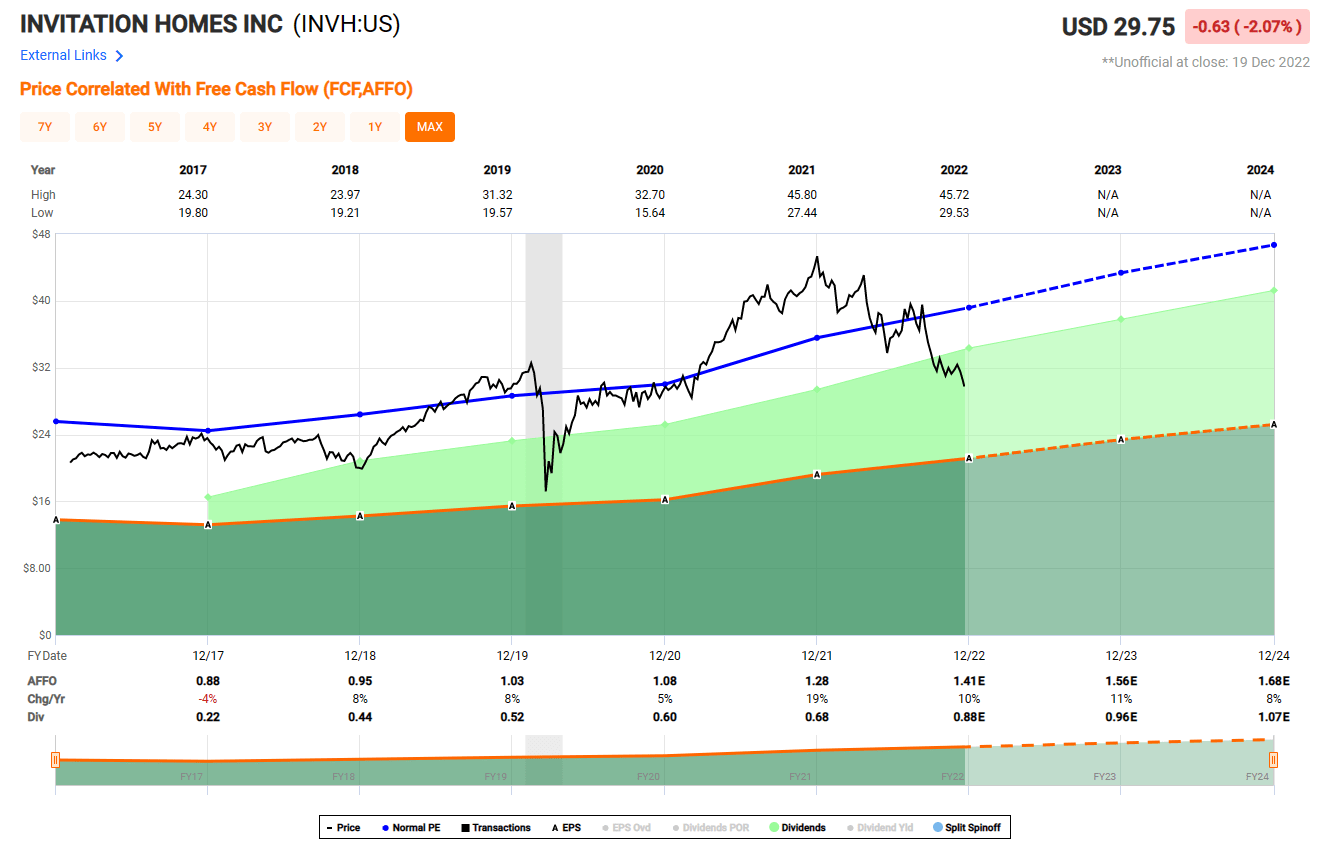

Invitation Homes portfolio and revenue has been growing substantially in the past several years. Their revenue growth in the past 5 years has been 17.75% CAGR, and the adjusted funds from operations (“AFFO”) growth rate has been 13.86% CAGR in the same time span. Given that their markets lie in high growth areas of population, I expect the trend to continue well into the future.

Investor Relations

The dividend of Invitation Homes is safe at this point. The cash dividend payout ratio is at 49.17%, and FFO payout ratio is at 53.99%. There is a substantial cushion between the cash flow and their dividend payout.

Their valuation is favorable as well. The current P/AFFO of 24.3x and P/FFO of 16.78x are about 25% below their 5-year average.

The negative sentiment towards the real estate market caused by high mortgage rates had led to this favorable valuation. Investors can grab some share at a discount.

FAST Graphs

VICI Properties (VICI)

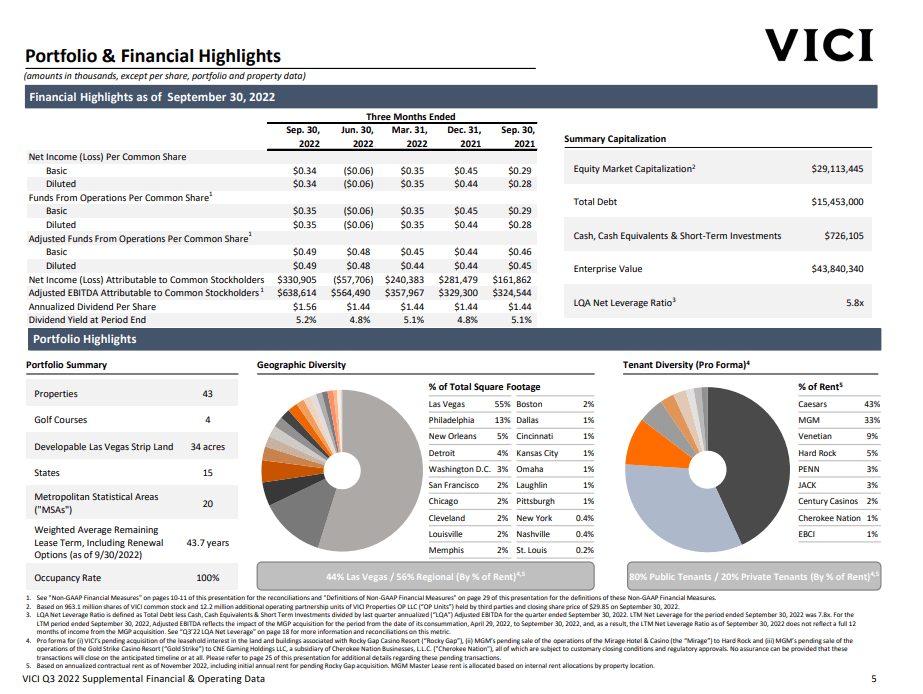

VICI Properties Inc. is a REIT that primarily engages in the business of owning, acquiring, and managing gaming, hospitality, and entertainment destinations. Their portfolio includes impressive names like Caesar Palace Las Vegas, Harrah’s Las Vegas, and Venetian Resort.

The weighted average remaining lease term is a whopping 43.7 years.

Not only that, but VICI owns about 34 acres of undeveloped or underdeveloped land near the Las Vegas Strip, which can be monetized when the time is appropriate.

Investor Relations

VICI has a strong capital structure and ample liquidity to further improve their already impressive portfolio. Their LQA net leverage ratio is 5.8x. They have revolving credit facility capacity of $2.5 B, and delayed draw term loan capacity of $1.0 B. Their total liquidity capacity is an impressive $4.7 B.

With this strong capital structure and great liquidity, they won’t have any trouble supporting their acquisition and development plans in the future. I expect them to maintain their leadership position in the gaming and hospitality industry.

Management described the 3Q 2022 results as demonstrating “realization and continuing activation.” By realization, they mean growth since 2021, and by activation, they mean continuing investment in the non-gaming segment.

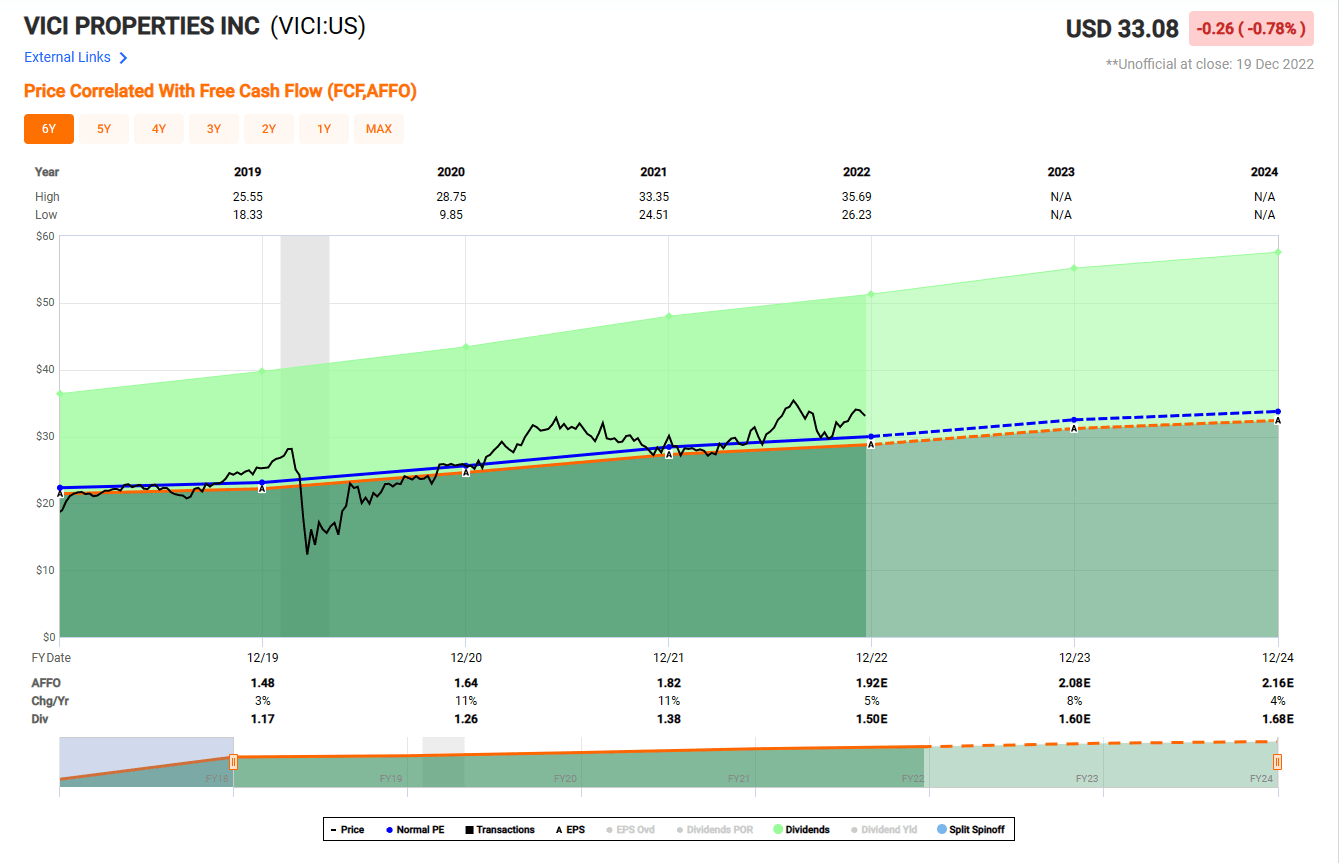

Revenue grew by 100% compared to the same quarter in 2021, and the impact from the acquisition of the Venetian and MGP was a large part of the growth. AFFO grew by 83% YoY, and AFFO per share grew by 8.5% YoY.

The growth in AFFO was followed by a dividend increase of 8.3%, which has resulted in a dividend growth rate of 8.2% CAGR since 2017 for VICI.

Also, VICI’s 4.7% dividend yield is safe at this point, shown by cash dividend payout ratio of 61.47% and AFFO payout ratio of 79.46%.

VICI is currently undervalued. P/AFFO of 18.02x and P/FFO of 15.73x is about 10% lower than their historical average. The iREIT ratings tracker shows that the margin of safety for VICI is at 7%.

The market wide volatility and fears of recession have created a great opportunity here for investors.

FAST Graphs

Equity Residential (EQR)

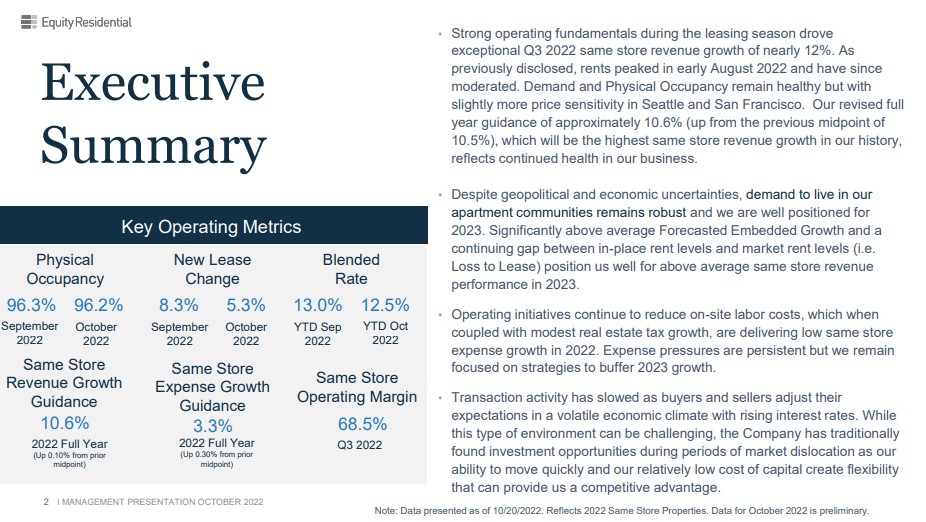

Equity Residential is a REIT that owns and operates high-quality rental apartment properties. Their main markets include Boston, New York, Washington D.C., Southern California, and Seattle.

Their properties are well managed and in high demand, shown by an exceptional occupancy rate of 96.3%, and the quality of the portfolio has improved over the course of the year (same unit revenue growth of 10.6% for 2022).

Investor Relations

Equity Residential’s management expects the strong growth to carry into 2023. As in-place leases expire and are renewed at the prevailing market prices, the revenue is expected to grow.

Currently, Equity Residential’s Loss to Lease (in-place lease price compared to the current rate) is about 5.1%. Essentially, this means that the portfolio of current leases is about 5.1% below the current prevailing lease rate. Therefore, over the course of 2023, Equity Residential’s revenue will grow.

Equity Residential’s dividend is safe at this point, as demonstrated by a cash dividend payout ratio of 66% and FFO payout ratio of 72.87%.

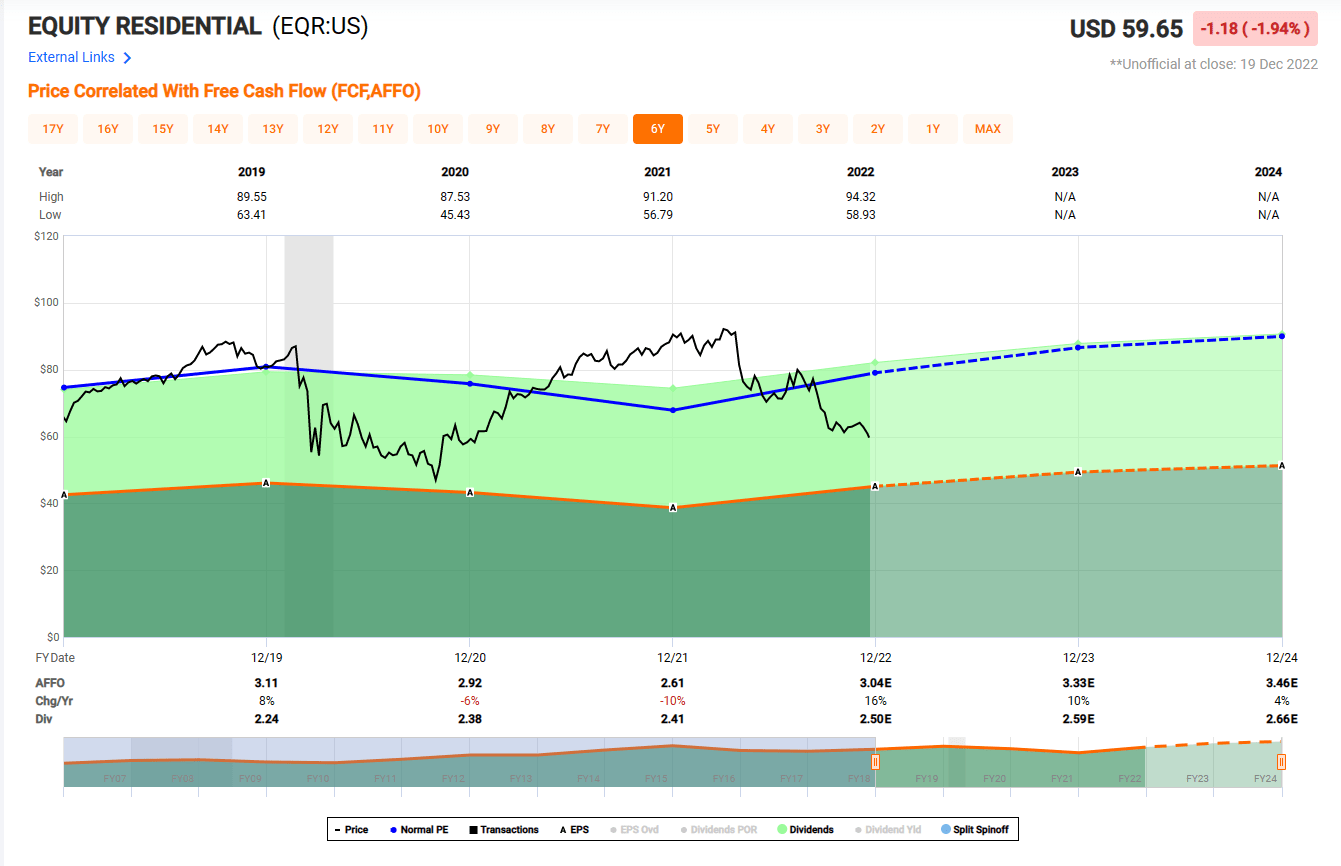

Also, Equity Residential is undervalued at this point. Their current P/AFFO of 23.67x and P/FFO of 16.05x are about 23% below their 5-year average. The iREIT equity rating tracker shows that Equity Residential’s margin of safety is at 17%.

The recent slump of the real estate market and sour consumer sentiment over the high interest and mortgage rates have created another great opportunity for investors.

FAST Graphs

Risks

As many of us expected, the Federal Reserve came out and raised the interest rate by 50 basis points. That was welcome news and experts expected the market to gain some momentum.

However, Jerome Powell’s comments remained rather hawkish, indicating that the Federal Reserve is still not happy with the inflation rate. The Federal Reserve will maintain a high interest rate until their job is “done.”

This hawkish tone poured cold water onto the market yet again, and the bear sentiment returned in full force. It will be hard for the stock market to gain momentum in this environment, and these three REITs are going to struggle right along with the market.

As recessionary pressure mounts, capital availability will be reduced in the short term. Less capital equals fewer real estate transactions. A slow transaction rate and less capital availability may negatively impact the REITs’ growth plan.

Fewer properties available on the market will slow down the acquisition activities, and the spread between the buyer and the seller may increase.

Conclusion

Christmas is almost here.

It’s typically a very happy time for everyone.

However, fears of recession and high inflation are bringing some gloomy sentiment to the market.

But it’s not all bad news, though. Unemployment has stayed at a historically low level, and hospitality, leisure, and restaurant industries roared back this year. These trends should help the three REITs mentioned here.

It’s hard to keep trust in a volatile market and stick to your long-term goals. However, slow and steady wins the race. Keeping a long-term perspective and investing money in these three solid REITs has been a winning formula for many years.

I believe the formula holds true at the end of 2022 and beyond for sure.

Be the first to comment