SvetaZi/iStock via Getty Images

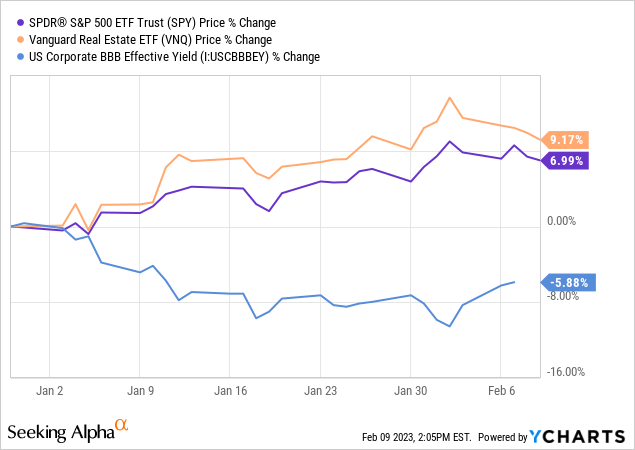

So far this year, the S&P 500 (SPY) and Vanguard Real Estate Index (VNQ) have rallied as long-term interest rates begin to price in an eventually lower Federal Funds rate later this year or next year.

Whether this newfound optimism turns into a new bull market or fizzles out and transitions into the next leg down in the bear market, it seems like a good idea to remain defensive in the stocks one chooses to buy, especially for dividend-oriented investors who wish to protect their dividend income.

After all, even if the Fed does cut interest rates later this year, it will likely be due to a recession. Caution seems appropriate.

As for this dividend growth investor, I recently initiated new positions in three dividend stocks that I believe to be defensive and recession-resistant. I also think they offer strong long-term growth prospects.

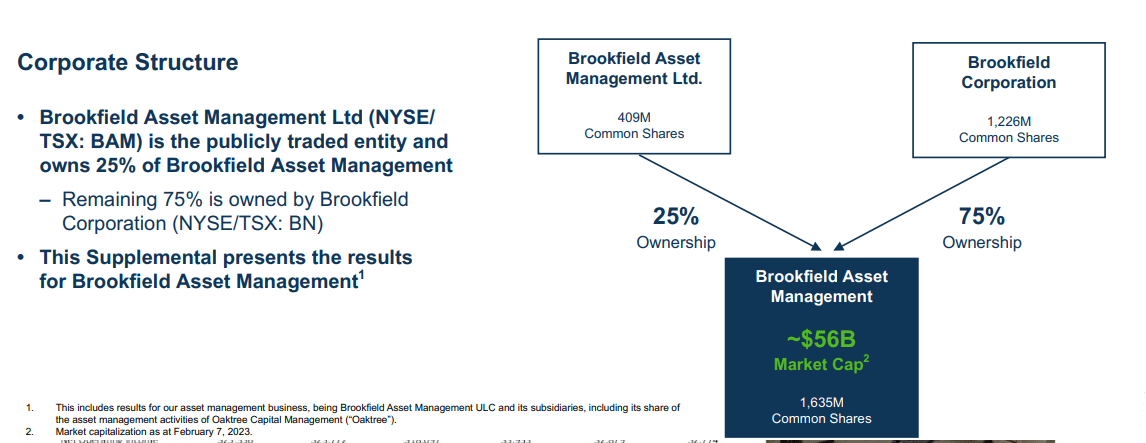

Brookfield Asset Management (BAM)

Since the split between BAM and Brookfield Corporation (BN) in December, there have been some fantastic analyses proffered here on Seeking Alpha, including from Samuel Smith at High Yield Investor.

BAM Q4 2022 Presentation

BAM is one of the biggest (~$800 billion in assets under management) and best asset managers in the world, led by the steady hand of long-time CEO Bruce Flatt. The company boasts a commanding market position in infrastructure, real estate, and renewable energy assets (the “backbone of the global economy”), both of which are expected to provide massive investment opportunities in the decade ahead.

Moreover, by nature of the asset management business, BAM does not need to raise much debt or equity capital, because it mostly uses third-party funds for investment purposes and fee generation. As such, BAM is a very capital-light business with zero debt and $3.2 billion in cash and financial assets ready to support growth.

What’s more, with 83% of fee-bearing capital long-term or perpetual in nature (thanks in part to its publicly traded investment vehicles), BAM is unlikely to suffer similar problems as Blackstone (BX) has had with investor withdrawals from its flagship real estate fund.

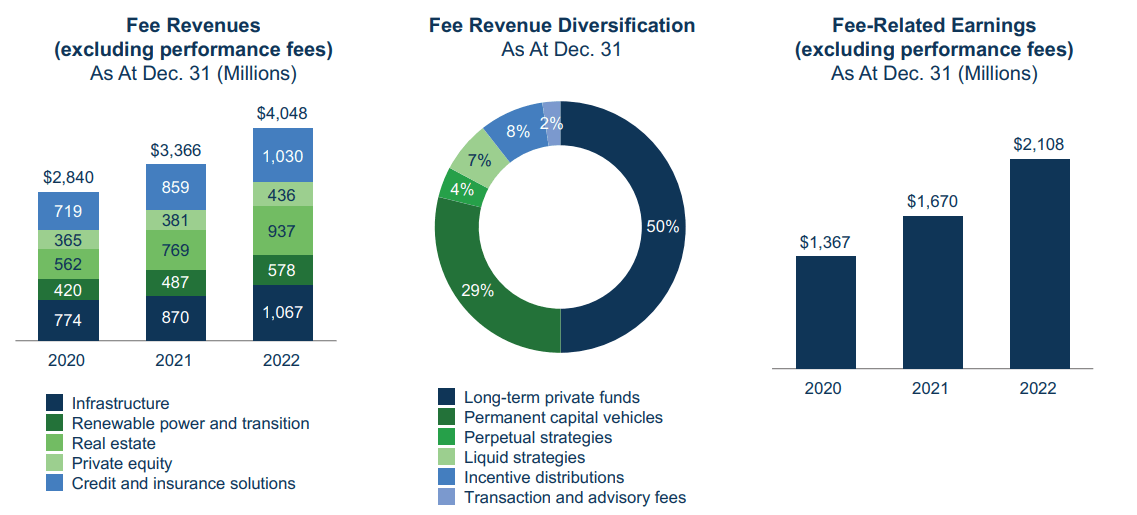

BAM aims to grow fee-related earnings (“FRE”) by 15-20% per year over the next several years, which should in turn facilitate a similar rate of dividend growth. In 2022, FRE surged by 26% to $2.1 billion, or $1.29 per share.

BAM Q4 2022 Presentation

In Q4 2022, BAM generated $0.35 in distributable EPS, covering the $0.32 quarterly dividend at a payout ratio of 91%. Given BAM’s capital-light model, stable fee generation from long-term private funds, and ample fundraising ability, the company does not need to retain much cash, hence the 90%+ payout ratio.

BAM is currently valued at a price to distributable earnings of 27.6x, which sounds high only if you ignore the fact that BAM is likely to turn in a 15-20% annual growth rate.

The dividend yield of 3.6% drops to around 3.1% after tax withholding for American investors, but a 15%+ dividend growth rate on top of that is extraordinary.

First Interstate BancSystem (FIBK)

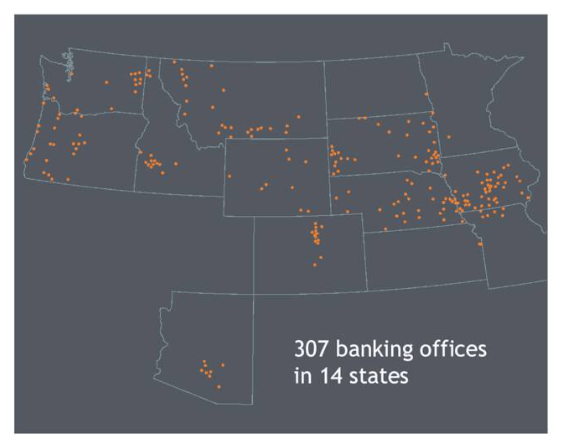

FIBK is a Montana-based regional bank that sold off hard recently after poor Q4 2022 earnings. After last year’s mega-acquisition of Great Western Bancorp (GWB), FIBK’s operational territory extends as far West as Oregon and Washington and as far East as Iowa.

FIBK Q4 2022 Presentation

There were credit issues to work through with the GWB acquisition, and there remain a lot of moving parts to FIBK that complicate and muddy the outlook. Clearly, with EPS declining from $0.83 in Q4 2021 to $0.82 in Q4 2022, the GWB acquisition has not been as accretive as management would’ve liked so far.

But I do think the long-term outlook for FIBK remains strong, with a loan portfolio split roughly 60% fixed rate and 40% floating rate. More Fed rate hikes will be beneficial for the bank, but if (and when?) rate cuts eventually come, FIBK will be better prepared than more asset sensitive banks with higher floating rate exposure in their loan books.

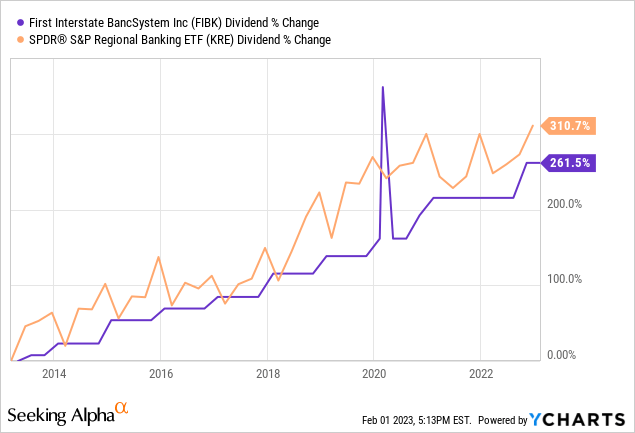

What’s more, FIBK has quite a respectable dividend growth record over the last decade, though not as strong as the S&P Regional Banking ETF (KRE):

But compared to KRE’s dividend yield of about 2.3%, FIBK currently offers a dividend yield of about 5.2% (as of this writing). Moreover, with a payout ratio slightly under 60%, FIBK’s dividend appears to be safe.

I think management should be able to fix the issues and revive growth once GWB is fully absorbed.

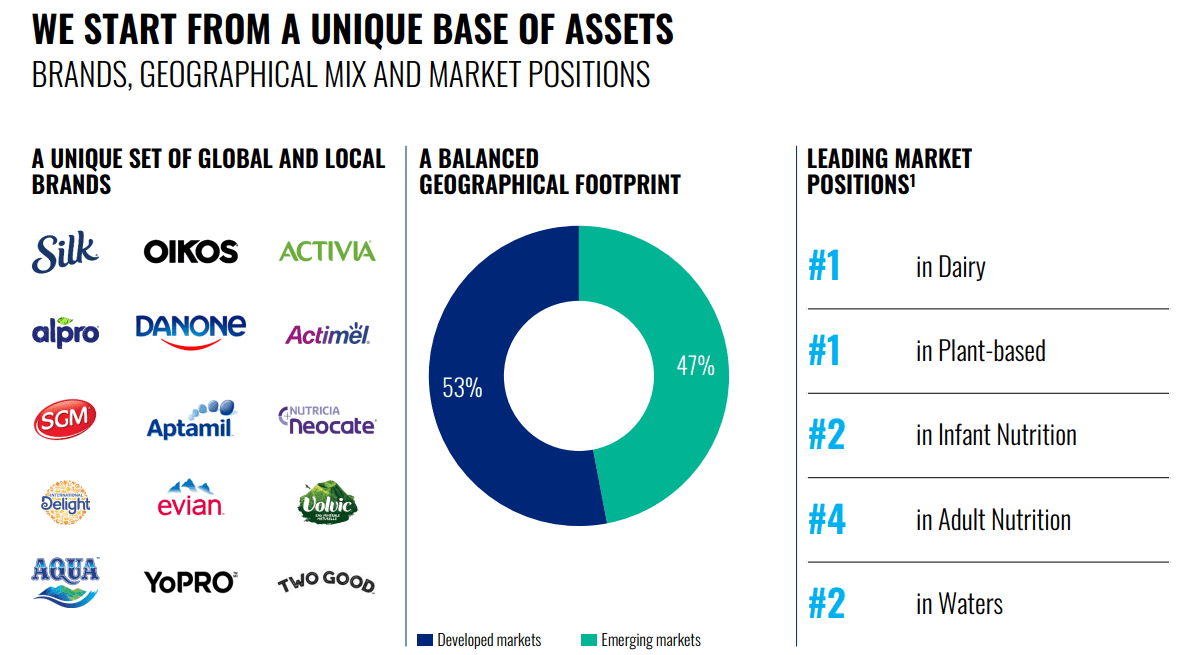

I recently wrote an introductory article about French consumer staples company Danone, explaining why I like it and bought a small starter position in it.

The company’s brands enjoy strong market leadership in their respective categories, but they haven’t been managed for optimal growth. The relatively new CEO (installed September 2021), Antoine de Saint-Affrique, appears to be doing a good job of reviving growth and innovating to remain competitive.

DANOY March 2022 Presentation

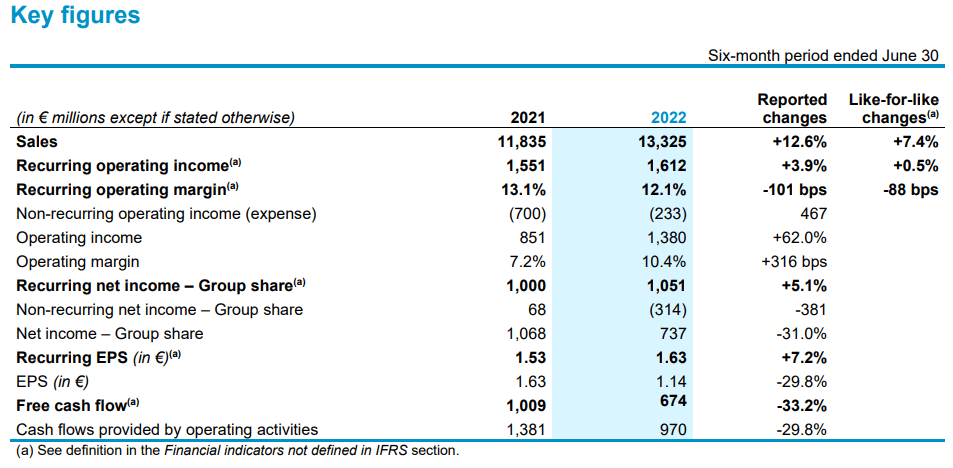

In the first half of 2022, despite 12.6% sales growth YoY, net income grew only 5.1% while recurring EPS rose 7.2%. Operating cash flow, however, declined by around 30%, and free cash flow plunged 33%.

Danone 1H 2022 Report

Input cost pressures have been an anchor on Danone’s profitability and cash flow, and rising interest costs haven’t helped.

But, fortunately, in Q3’s earnings report, the situation appears to have improved for the consumer staples company. Like-for-like sales rose 9.5% (compared to 7.4% in the first half of 2022), spurring management to raise LFL sales guidance for the second time last year. Meanwhile, the recurring operating margin held steady at a little above 12% as inflationary pressures had only just begun to ease during the quarter.

While inflationary pressures will likely continue to keep margins low in the first half of this year, I would expect to see the operating margin expand in the second half of the year as input costs settle and Danone’s price hikes take effect.

With a dividend yield around 4% and a P/E ratio of 15.5x, Danone is way cheaper than most of its consumer staples peers and strikes me as a defensive holding to own going into a recession.

Bottom Line

While it is a bit disconcerting that a 2023 recession has become the consensus view (and the consensus is often wrong), the data still appears to point decisively toward that scenario.

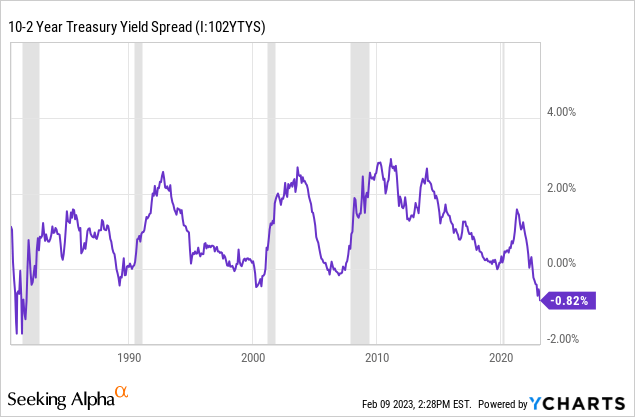

For example, the 10-year / 2-year Treasury yield spread, which has reliably predicted every recession upon sustained inversions, is now more inverted than at any point since the early 1980s.

The inverted yield curve is flashing a red “Recession Incoming!” sign, and investors ignore it at their peril.

I would argue that BAM, FIBK, and DANOY are each defensive and recession-resistant in their own respective ways. Their dividends, with yields ranging from 3.6% to 5.2%, are unlikely to be cut. In fact, I believe them likely to keep growing at steady pace going forward.

That makes these three dividend stocks worthy of consideration during these uncertain times.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment