Igor Borisenko/iStock via Getty Images

Civitas Resources (CIVI) may be able to generate over $1 billion in positive cash flow in 2022 at current strip prices. This would allow it to nearly pay off its net debt (which increased by around $221 million with its Bison acquisition) and also pay substantial dividends. Based on its tentative dividend framework, it may be able to pay total dividends of around $6.75 per share based on 2022 free cash flow at current strip prices.

Bison Acquisition

Civitas is acquiring Bison Oil & Gas II, continuing its consolidation spree in the DJ Basin. It is paying $346 million for Bison, consisting of 2.3 million common shares, $45 million in cash and the assumption of $176 million in debt and other liabilities.

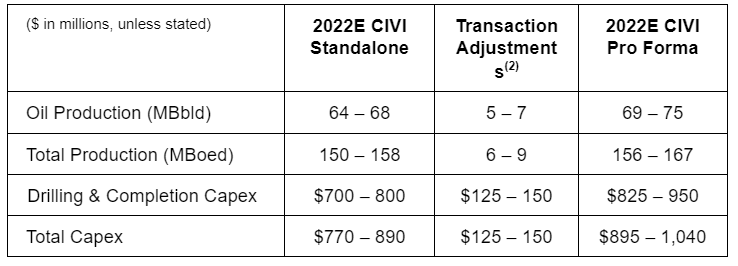

The Bison assets are expected to produce an average of around 9,000 BOEPD (75% oil and 90% liquids in 2022). This appears to be higher than current production levels, which may be around 5,000 BOEPD to 6,000 BOEPD given the large amount ($125 million to $150 million) budgeted for the Bison assets in 2022.

The Bison assets are expected to generate around $200 million EBITDA in 2022 (full year). It also comes with 102 gross locations, of which 38 are fully permitted. Many of the fully permitted locations could be drilled in 2022.

Production Levels

Civitas estimated that its Q4 2021 production would average 151,000 BOEPD (40% oil) at guidance midpoint, assuming that its business combination and Crestone Peak acquisition closed at the start of the quarter.

It projected 154,000 BOEPD (43% oil) in average production as a standalone company for 2022, with a capital expenditure budget of approximately $830 million. This would be 2% total production growth and 9% oil production growth compared to Q4 2021 levels.

Civitas: Preliminary 2022 Production Expectations (civitasresources.com)

Civitas is now expecting around 161,500 BOEPD (45% oil) production in 2022 including 10 months of production from the Bison acquisition. With a full year’s worth of production from Bison, Civitas’ 2022 production would be around 163,000 BOEPD (45% oil).

2022 Outlook

At current strip prices for 2022 (approximately $83 WTI oil and $4.80 NYMEX gas), Civitas may generate around $3.044 billion in oil and gas revenues before hedges. This assumes 163,000 BOEPD in average production. I’ve included a full year of production from the Bison acquisition since the effective date of the transaction is January 1, so the cash flow from that asset during the first couple of months of 2022 (before the deal closes) will result in a purchase price adjustment.

Civitas’ hedges have an estimated negative $356 million in value at current strip for 2022.

Civitas’ Hedges (civitasresources.com)

Thus, after hedges, Civitas is projected to generate $2.688 billion in revenues.

| Type | Units | $/Unit | $ Million |

| Oil (Barrels) | 26,645,000 | $78.00 | $2,078 |

| NGLs (Barrels) | 13,687,500 | $37.00 | $506 |

| Natural Gas [MCF] | 114,975,000 | $4.00 | $460 |

| Hedge Value | -$356 | ||

| Total Revenue | $2,688 |

Author’s Work

With a $968 million capital expenditure budget, I estimate that Civitas’ total cash expenditures will reach $1.675 billion for 2022.

| Expenses | $ Million |

| Lease Operating Expense | $202 |

| Gathering, Transportation, Processing and Midstream | $268 |

| Production Taxes | $167 |

| Cash G&A | $40 |

| Cash Interest | $30 |

| CapEx | $968 |

| Total Expenses | $1,675 |

Author’s Work

Thus, Civitas is projected to generate $1.013 billion in positive cash flow in 2022 at current strip and before any dividend payments.

Civitas’ base dividend is around $161 million per year at $1.85 per share and 86.8 million shares outstanding. It previously mentioned a proposed plan to return 50% of free cash flow (after its base dividend) to stockholders in the form of a variable cash dividend.

Half of its free cash flow (after its base dividend) for 2022 at current strip prices would be $426 million or approximately $4.90 per share. The first variable cash dividend may be based on 2021 results though.

Debt Situation and Valuation

Civitas ended 2021 with around $250 million in net debt (with $500 million in outstanding notes and $250 million in cash on hand). The Bison acquisition adds $221 million in debt and other liabilities.

Civitas’ positive cash flow after dividends would reduce its net debt to around $45 million at the end of 2022 at current strip prices.

At a 3.0x EV to unhedged EBITDAX (at $65 WTI oil and $3.25 NYMEX gas) multiple, I estimate that Civitas would be worth approximately $56 per share in one year. This is based on current strip for 2022, and then uses $65 WTI oil and $3.25 NYMEX gas after. While this is around Civitas’ current share price, this calculation assumes that Civitas will pay $6.75 per share in dividends for 2022, so the total return would be around 14% if Civitas is at $56 in one year’s time.

At long-term $70 WTI oil and $3.50 NYMEX gas, Civitas’ estimated value (in one year) increases to approximately $62.25 per share.

Conclusion

Civitas may be able to generate over $1 billion in positive cash flow in 2022 at current strip prices. This would allow it to pay off most of its net debt as well as pay dividends (fixed plus variable) that could add up to as much as $6.75 per share.

If it pays dividends of $6.75 per share over the next year, its value in a longer-term $65 WTI oil scenario is near its current share price. The returns would mostly be from the dividends in that case. At longer-term $70 WTI oil, Civitas’ estimated value for early 2023 rises to around $62.25 per share, or around $69 including dividend payments.

Be the first to comment