Sundry Photography

Zscaler (NASDAQ:ZS) is well positioned in cloud security, providing multiple services for users, workloads, cloud as well as IoT/OT. Its Zero Trust platform has the potential to disrupt the traditional legacy firewall+VPN structure. I believe Zscaler can sustain 30%+ revenue growth in the near future. I initiate with a ‘Buy’ rating with a one-year price target of $230 per share.

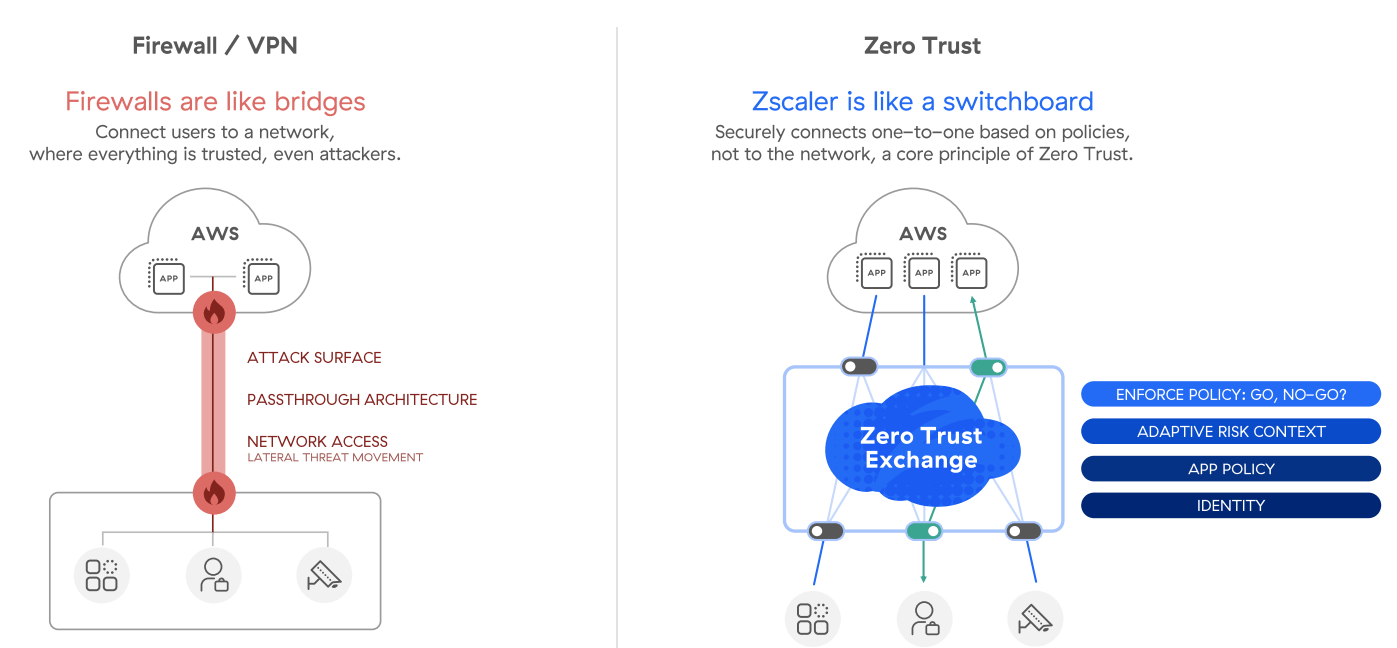

Zero Trust Platform Wining the Cybersecurity Market

Zero Trust includes several core products including Zscaler for Users, Zscaler for Workloads and Zscaler for IoT/OT, powering enterprise customers in their cloud migration and digitalization efforts. As of Q3 FY24, Zscaler’s Zero Trust platform has already processed over 400 billion transactions. As depicted in the chart below, Zero Trust Exchange provides enforce policies, manages risk, provides application policies and identity controls, disrupting the traditional Firewall/VPN cybersecurity structure.

Zscaler Investor Presentation

Zscaler’s Zero Trust platform has the following advantages:

- It provides one integrated platform to secure all the network and cloud traffic. It makes earlier for enterprises to management its network and cloud security via Zscaler’s unified platform. Dealing with less vendors, enterprise security operations can save tremendous time and costs in handling cyber breaches and monitoring.

- The platform enables enterprise customers to manage their users, devices and applications from any locations. In the current IT environment, enterprise customers face the challenge of dealing with multi-clouds, multi-users, and complex network access environments. Zscaler’s Zero Trust platform is an ideal solution for managing these complex access activities.

- The centralized trust exchange makes it possible for enterprise customers to leverage cybersecurity data for AI machine learnings. Zscaler’s platform can provide valuable insights from all major devices and network access, and the data can be used for enterprise’s AI training and inference workloads.

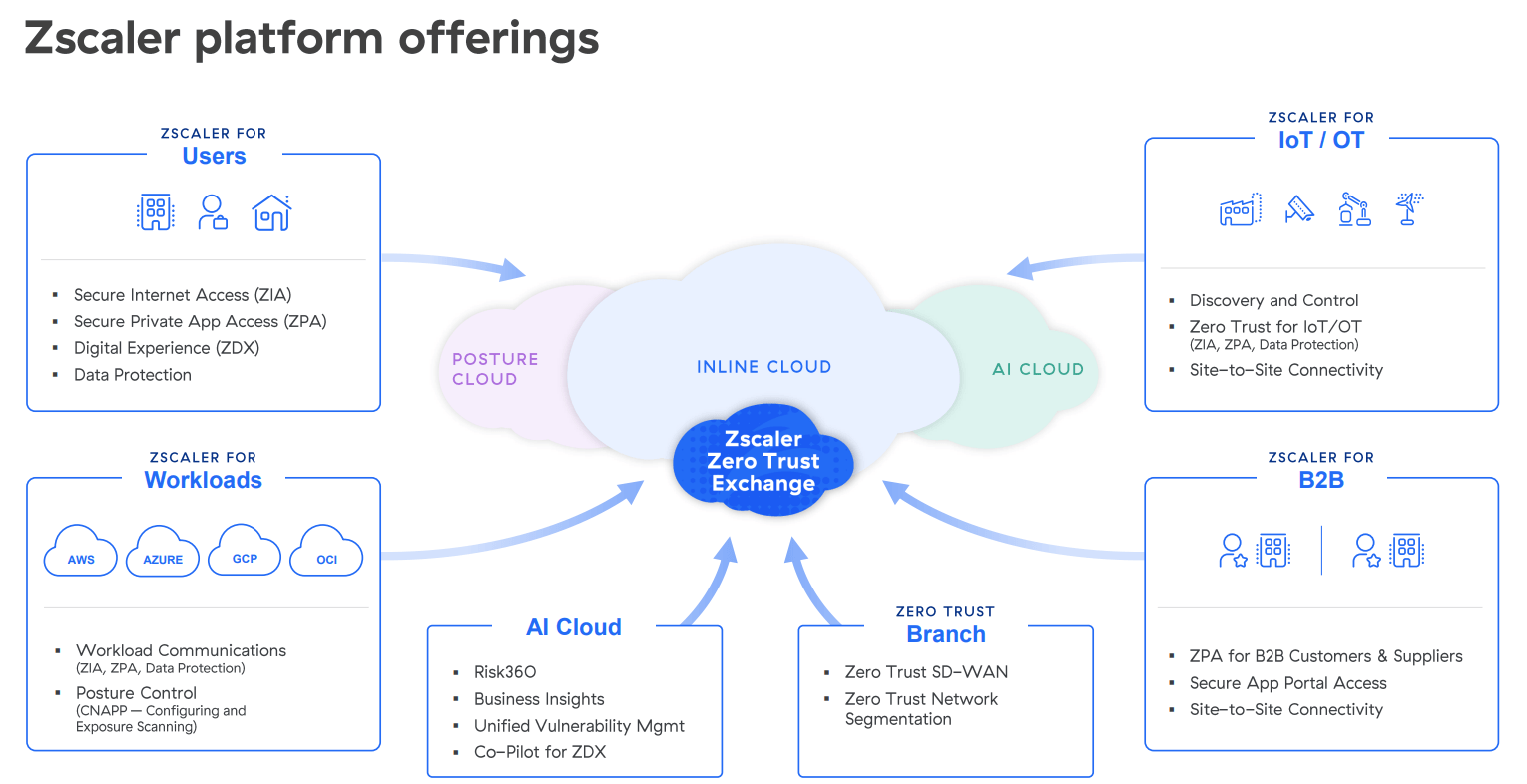

Large Deals and Bundles Accelerate Margin and Billings

As shown in the chart below, Zscaler has been expanding its product offerings across users, IoT, cloud, AI and workloads. These emerging technologies, along with its core Trust Exchange, enable Zscaler’s sales team to secure larger deals with more product bundles.

Zscaler Investor Presentation

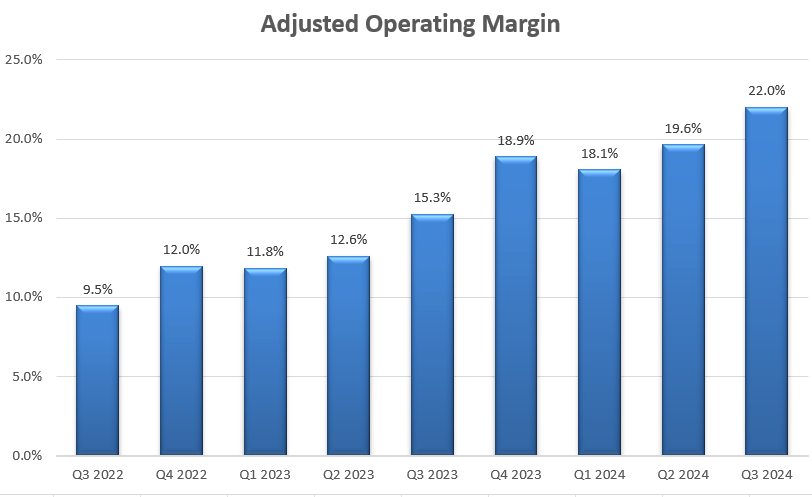

Partially because of these large deals and bundles, Zscaler has expanded its operating margin from 9.5% in Q3 FY22 to 22% in Q3 FY24. Over the latest earnings call, their management indicated that the company has experienced increased success with larger bundles and selling multiple pillars.

Zscaler Quarterly Results

I anticipate its large deals and bigger bundles will continue in the near future for the following reasons:

- Zscaler provides a variety of packages for users, internet access, and private access networks. For instance, Zscaler for Users bundles combine Zscaler Internet Access, Zscaler Private Access, and Zscaler Digital Experience. With these bundles, enterprise customers can leverage the full benefits of Zscaler Zero Trust Exchange. From the customers’ perspective, these bundles can save on subscription costs.

- In FY23, channel partners accounted for almost 92% of total Zscaler’s total revenue. Zscaler has started to expand its direct-to-consumer channel in recent years. With a growing direct sales team, Zscaler can potentially penetrate high-end customers, with more complicated workloads and cybersecurity needs. During Q3 FY24 earnings call, the management expressed that the company would continue hiring for sales team, aiming to capture more large deals.

Latest Result and FY25 Outlook

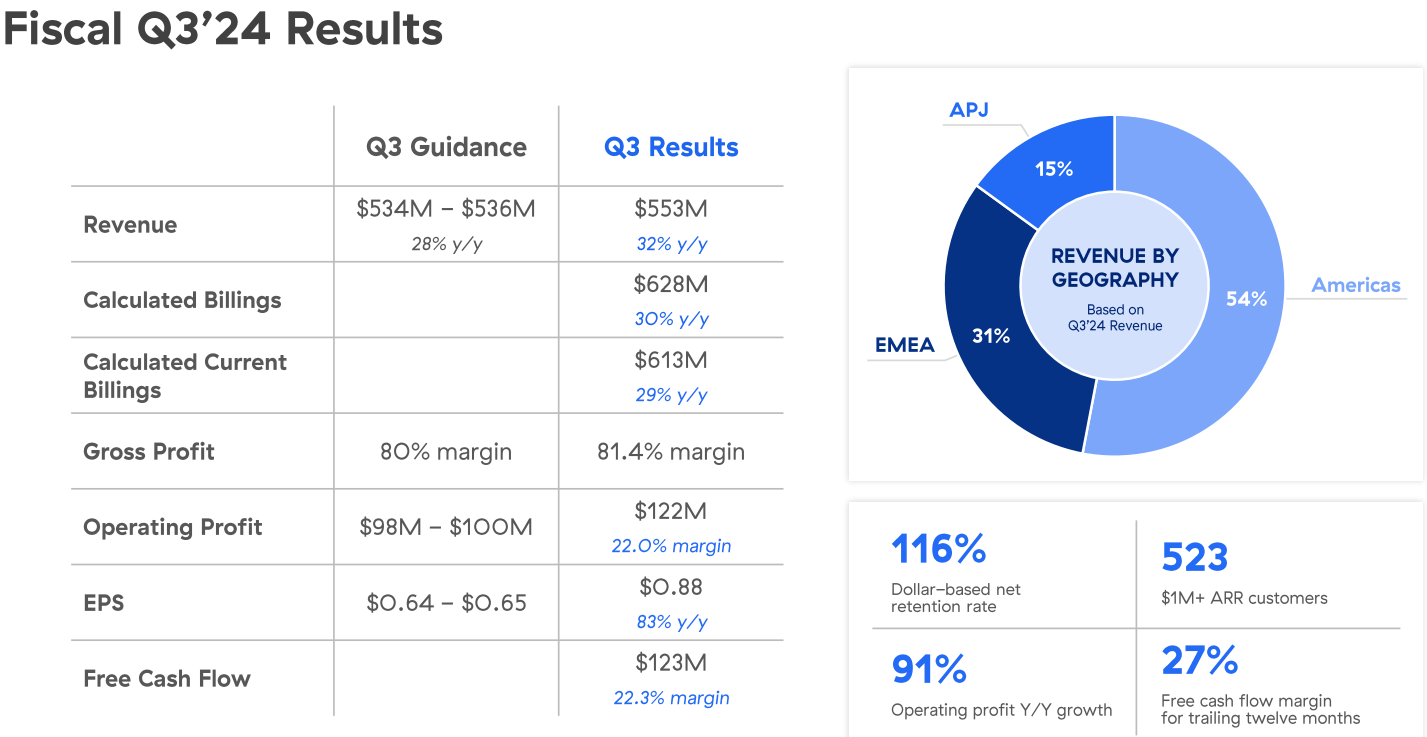

In Q3 FY24, Zscaler delivered 32% revenue growth and 30% billings growth year-over-year, as detailed in the summary below. It is a quite strong financial results considering that most enterprise customers are rationing their IT budgets and allocating less to software spending and more to AI-related platforms, as evidenced by the latest results from Salesforce (CRM), ServiceNow (NOW) and Workday (WDAY).

Zscaler Q3 FY24 Result

I anticipate Zscaler will continue to deliver 30%+ growth in FY25 for the following reasons:

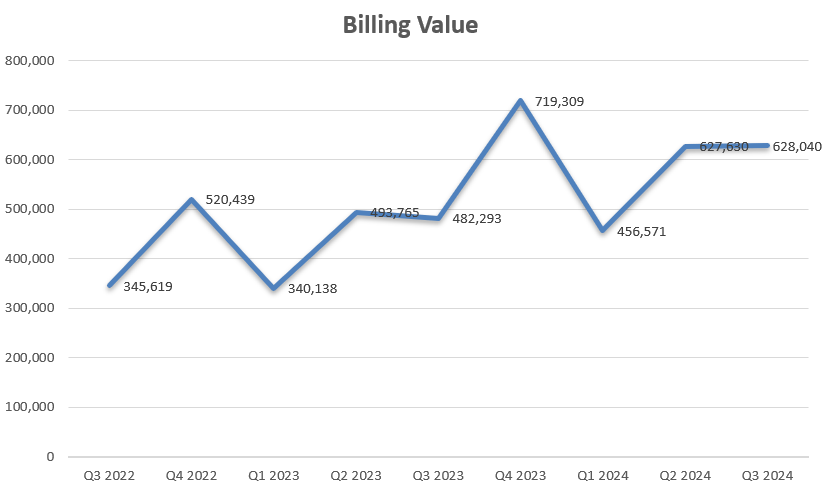

- In Q3 FY24, Zscaler delivered 30.2% growth in calculated billings, as shown in the chart below. The billing growth is a leading indicator of Zscaler’s growth in the upcoming quarters. As discussed previously, the strong billing growth is driven by winning large deals and increased bundle sales.

Zscaler Quarterly Results

- Although fast-growing, Zscaler is a relatively small company, expecting only $2 billion+ in revenue in FY24. The company operates in a vast cybersecurity market, where it remains a smaller player. This smaller base allows Zscaler to maintain its rapid growth pace.

- Lastly, Zscaler has expanded its product offerings in recent years, thereby increasing its total addressable market. They have successfully introduced services such as workflow automation, Risk360, Branch connector, and identity security. I believe the company will continue its R&D path to introduce more emerging products offerings in the near future, better leveraging its existing customers, and expanding new clients.

Valuation

As discussed, I anticipate Zscaler will grow its revenue by 30% in FY25, driven by its strong billings growth and emerging product offerings. Fortune Business Insights forecasts that the cloud security market will grow at a CAGR of 17.3% from 2024 to 2032, driven by identity security, data loss prevention and event management etc. Zscaler is well positioned in these platforms, and I expect its Zero Trust platform to gradually disrupt the traditional Firewall/VPN infrastructure. As such, I foresee Zscaler outpacing the overall market growth.

Considering its scaling trajectory, I forecast that Zscaler will achieve revenue growth of 25% in FY28, followed by 20% in FY30, and eventually stabilize at 15% from FY32 onward, aligning with the typical growth trajectory of high-growth software companies.

On the margin side, Zscaler has effectively managed its operating expenses, by reducing its sales & marketing expenses and optimizing its R&D resources. Its reported operating margin has been improved from -30.9% in FY21 to -14.5% in FY23. I forecast the company can achieve 400bps operating leverage from sales/marketing expenses, as more sales shift towards the direct channel with better margins. Additionally, I calculate 20bps of operating leverage from both R&D and G&A expenses. In total, I expect the company to deliver 420bps of annual margin expansion.

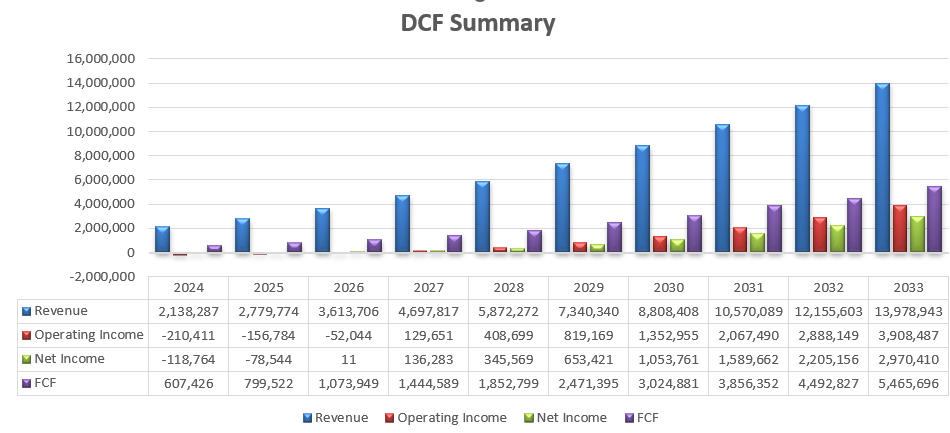

The DCF summary can be found below:

Zscaler DCF Summary – Author’s Calculations

I calculate the free cash flow from equity by adjusting the net income with depreciation/amortization, net change in working capital, and net borrowings:

Zscaler DCF Summary – Author’s Calculations

The cost of equity is estimated to be 19% assuming: risk-free rate 4.2% ((US 10Y Treasury Yield)); beta 2.14 ((Seeking Alpha) and equity market premium 7%.

Discounting all the future FCFE, the one-year price target is calculated to be $230 per share.

Key Risks

- High Stock Options: Zscaler allocated more than 27% of revenues to stock-based compensations (SBC) in FY23. While this is common in high-growth software companies, reducing SBC as a percentage of total revenue is crucial for margin expansion in the future.

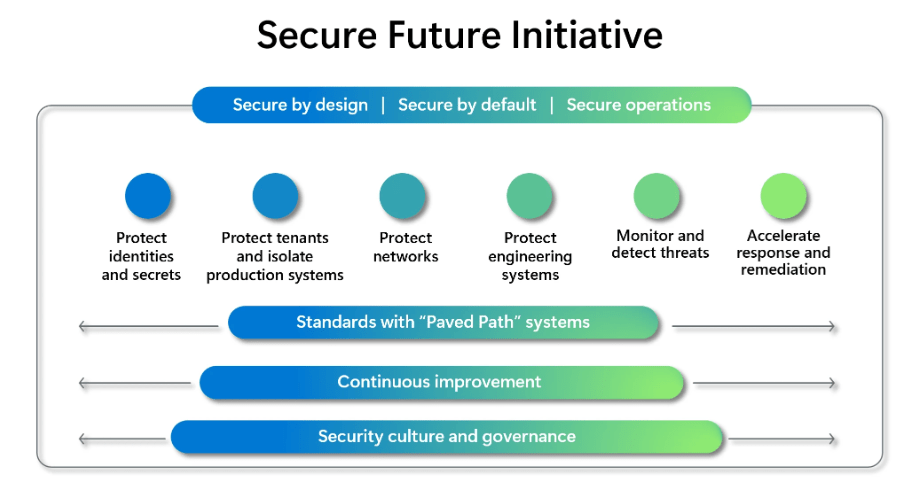

- Competition from Microsoft (MSFT): Microsoft has been expanding its cybersecurity offerings in recent years. In May 2024, Microsoft announced its Secure Future Initiative, expanding its services across identities, threat prevention, monitoring and remediation. Microsoft possesses significant advantages such as ample capital funding, a large customer base, as well as strong R&D capabilities. Zscaler’s shareholders need to monitor Microsoft’s progress closely in the future.

Microsoft Website

- Lastly, Zscaler is a high-beta stock, and its stock price is very volatile, especially during earning seasons. The company does not distribute any dividends or buy back shares. It is not suitable for value investors.

End Notes

Overall, Zscaler is well positioned in the cloud security market with its unified Zero Trust Platform, poised to disrupt the traditional firewall/VPN infrastructure. I anticipate the company will sustain 30%+ revenue growth in the near future. I initiate coverage with a ‘Buy’ rating and set a one-year price target of $230 per share.

Be the first to comment