zimmytws

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on November 26th, 2022.

VanEck CEF Muni Income ETF (BATS:XMPT) is invested in closed-end funds with municipal exposure. This year, munis – like most things – have been hit hard and are becoming attractive. They are becoming more attractive because as the share price slips, the yield goes higher. This is all being pressured by higher interest rates and the fact that municipal bonds are very interest-rate sensitive.

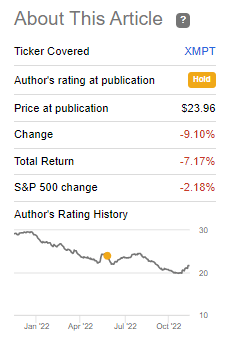

Since our previous update, the fund has declined by over 9%. On a total return basis, it has been a bit more muted of a decline as it factors in the dividends paid.

XMPT Performance Since Previous Update (Seeking Alpha)

Now that we are in a period where the Fed is starting to hint at a reduced pace of interest rate increases, munis can be a consideration for investors. It doesn’t mean that there isn’t potential for more downside going forward. However, the natural progression would be a reduction in the pace of increases and then an eventual pause in the increases altogether.

Throw in a recession, and we could see interest rates cut even. I think it’s probably far too early to look for cuts, but seeing a pause isn’t out of the question. If there is at least a pause, the downside from here should be minimal, and the fund should begin to make actual positive returns again.

The Basics

- Dividend Frequency: Monthly

- Dividend Yield: 4.51% (SEC yield 5.31%)

- Expense Ratio: 1.81% (including acquired fund fees and expenses)

- Leverage: N/A

- Managed Assets: $143.2 million

- Structure: Passive ETF

XMPT seeks “to replicate as closely as possible, before fees and expenses, the price and yield performance of S-Network Municipal Bond Closed-End Fund Index (CEFMXTR), which is intended to track the overall performance of the U.S.-listed closed-end funds that invest in U.S. dollar-denominated tax-exempt market.”

This is a rules-based index with several eligibility criteria that I’ll try to summarize with the main points:

- The CEF must be in one of the four categories: leveraged municipal fixed-income, leveraged municipal high-yield fixed-income, unleveraged municipal fixed-income or unleveraged municipal high-yield fixed-income.

- Must trade on a recognized North American stock exchange

- Minimum market cap has to be over $100 million

- Any CEF trading over an average premium of 20% for 10 days prior to the second Friday of the reconstitution will be excluded

- A non-constituent must maintain a management fee below 1.25%, while a current constituent must maintain a management fee below 1.5%

- A target-date fund must have a termination date of three or more years to be eligible

There are many more rules, but these are the main and most relevant ones. They then take these eligibility criteria and screen them for weightings to be included in the index. This process is done by the adjusted net assets of the CEF. Here is how they are adjusted.

- Net assets are multiplied by a factor of 1.3 for CEFs trading at a discount greater than 6%

- Net assets are multiplied by a factor of 1.2 for CEFs with a discount greater than 3% but less than 6%

- Net assets are multiplied by a factor of 1.1 for CEFs trading at a discount of 0% but less than 3%

- They are then multiplied by a factor of 0.7 for funds trading at over a 6% premium

- The factor is 0.8 for CEFs with a premium between 3% and 6%

- Then finally, the multiple factor is 0.9 for funds at a premium of 0 to 3%

Essentially, to sum up, the deeper the discount for the fund, the larger emphasis – the more expensive the CEF is, the less weighting it’ll have. They then include an 8% cap for any CEF. As well as a 45% cap on the entire portfolio with fund weights greater than 5%. They also never allow the number of positions to fall below 25.

This all means that there is some fairly strong diversification in these funds in terms of getting different muni CEFs in the index.

The fund is quite small, and it launched in mid-2011. Smaller funds tend to have less daily trading volume. The fund’s expense ratio comes to 1.81%, but only 0.40% of that is from the fund itself. The other 1.41% is the acquired fund fees and expenses.

Performance – Interest Rate Damage

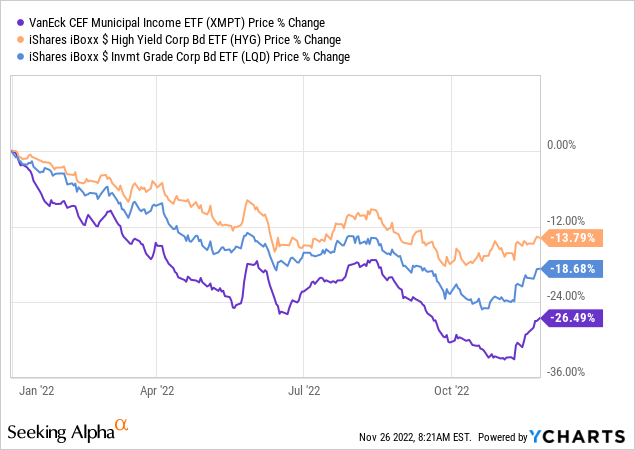

Munis tend to have long maturities, and that translates into high portfolio duration. XMPT’s effective duration is 12.69 years. For every 1% the Fed raises interest rates, XMPT’s portfolio should drop around 12.69%. Now, it’s not exact, but it has dropped further than both classes of corporate bonds.

We highlight below a YTD price performance against the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) and iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD).

Ycharts

We can see that XMPT performed the worst, then LQD underperformed HYG even though XMPT and LQD should both be safer than HYG. It all comes down to the duration of the portfolio being more interest rate sensitive. The effective duration for HYG comes to just 3.96 years, and LQD is at 8.51 years.

We would expect XMPT to underperform both HYG and LQD over the longer term due to what should be a more conservative fund. Except, there are things that make XMPT not as conservative as holding a basket of muni bonds. We see that over the longer term, XMPT has underperformed, as expected. However, it seemed to be in a more volatile manner, also as expected. In the end, it had come in quite close to LQD’s performance at this time.

XMPT invests in closed-end funds, making it unique relative to these other ETFs representing other fixed-income spaces. There are additional considerations when looking at CEFs that ETFs don’t usually have to think about.

For one, XMPT’s underlying holdings are going to be leveraged. Muni CEFs lover leverage in high doses. The primary reason is that they are almost risk-free bonds when backed by state governments. The only thing safer in the securities world would be debt issued by the U.S. Government.

Leverage adds additional risks, such as extra downside during a down year. Which is exactly what we’ve been seeing. Of course, it can also benefit when times are good and interest rates are near zero. As interest rates rise, the underlying leverage costs for CEFs will also rise. That cuts into the income generation of the funds. We’ve already been seeing this play out with several trimming distributions already.

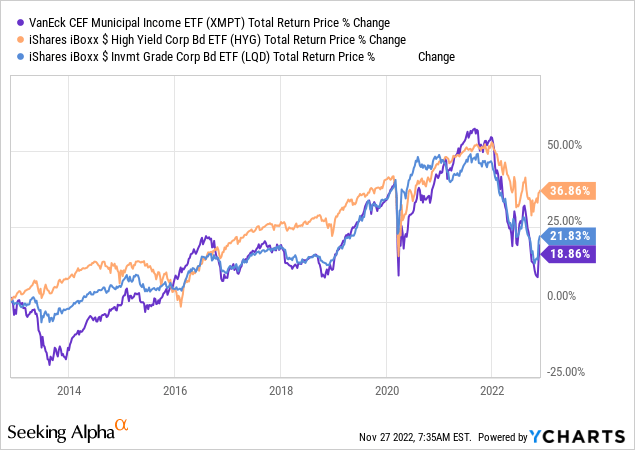

An additional consideration for XMPT for holding muni CEFs is the discount/premium. XMPT, as an ETF, doesn’t have to worry about extended periods of trading at significant discounts and premiums. On the other hand, CEFs can trade at discounts and premiums for a considerable period of time. In 2021, CEFs were at a historically high premium across the board. So unsurprisingly, we see that XMPT was outperforming both high-yield and investment-grade bonds if we look at the longer-term chart performance above.

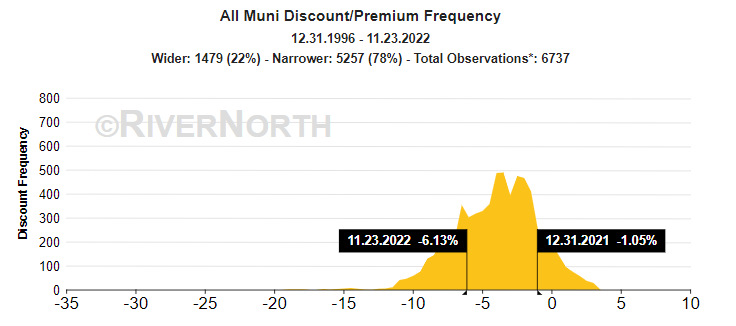

If we look at the current discount/premium of the muni CEF space, the fund’s discounts are now wider than usual on average. Thus, adding to the downside returns that the underlying muni bonds were already feeling. That can be the downside but also where the opportunity lies. This is for the entire muni CEF space more broadly, but we will take a look at some of the discounts/premiums of XMPT’s holdings, more specifically below.

Muni CEF Discount/Premium History (RiverNorth)

Holding CEFs also means a higher expense ratio too. ETFs are required to include the acquired fund fees and expenses and add those to their expense ratio. Thus, why XMPT is going to look like a very expensive ETF. A lot of that is contributed to by leverage costs on the underlying funds.

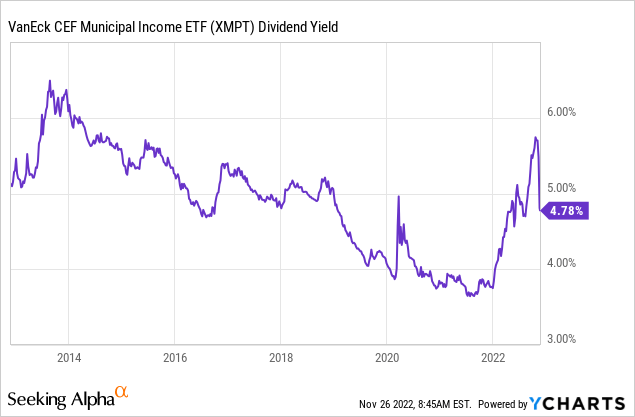

Dividend – Yields Rising

One thing that can be positive about higher interest rates is the lower prices that bump up the yields. Rates have moved lower lately due to what is the expectation for a decrease in the pace of increases. We can already see that the dividend yield for XMPT has dropped considerably but is still quite elevated relative to the last few years.

Ycharts

When interest rates are higher, bonds being issued have to have higher coupons to generate any interest. So new bonds being issued today aren’t going to be susceptible to the big drops that we’ve seen in old bonds. That is unless interest rates rise rapidly higher further yet from here. Then they would be pressured.

For muni bonds, that’s why they are so interest rate sensitive. They are lower yielding because they can be due to being safer. Due to being safer, they can also be issued with long maturities. Meaning that the portfolio turnover would naturally be much slower if they were waiting until maturity. XMPT is passive, but the underlying CEFs are active. So they aren’t necessarily waiting around until maturity to make moves.

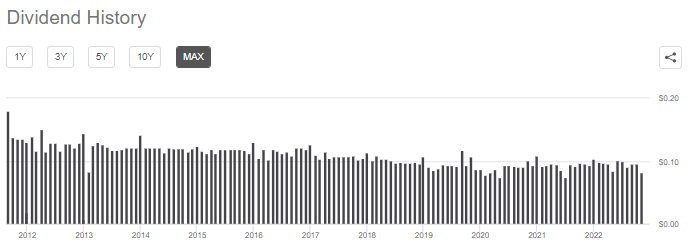

Like most ETFs, XMPT’s dividend is whatever the fund generates from income in the underlying portfolio. That means it changes from month to month and year to year.

XMPT Dividend History (Seeking Alpha)

There have been several muni CEFs that cut their distributions because of the higher interest rates making leverage costs rise. Therefore, it wouldn’t be surprising to see XMPT’s dividend decline for a while going forward.

Another benefit of investing in muni bonds is the tax-free portion of the distribution. For XMPT, the last two years had the majority of it being classified as such. That means depending on one’s tax rate, the tax-equivalent yield would be even higher than the headline yield.

XMPT Dividend Classification (VanEck)

XMPT’s Portfolio

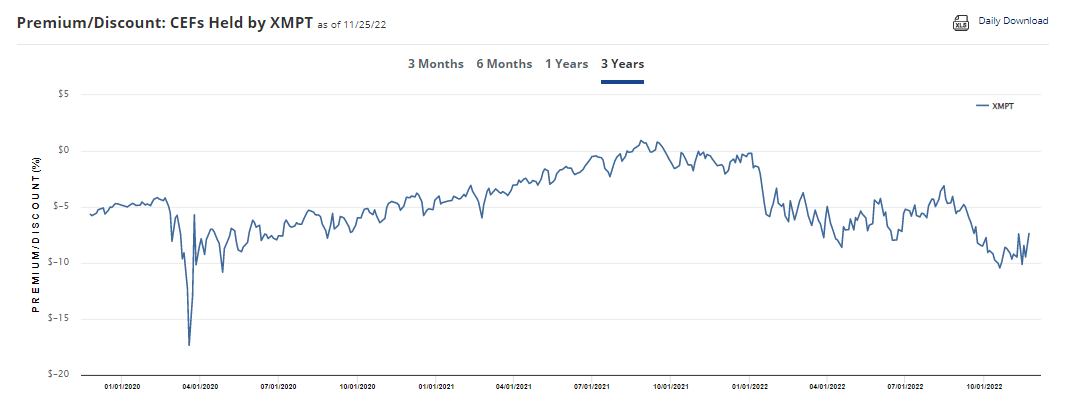

As we saw above, muni CEFs across the board are trading at generally wider discounts. This is consistent with what we see in XMPT as well. Here’s a chart of the discount/premium of the underlying portfolio over the last three years.

XMPT Underlying CEF Discount/Premium History (VanEck)

We can see that briefly through 2021, the funds were trading at parity – even popping into a slight premium for a short period. This widening backout is what is bringing the returns down for XMPT. This would be more so than what the equivalent non-CEF holding muni ETF would be on a YTD basis.

CEFs that hold munis are rather popular; they make up a good portion of total CEF assets if we pool together all the funds.

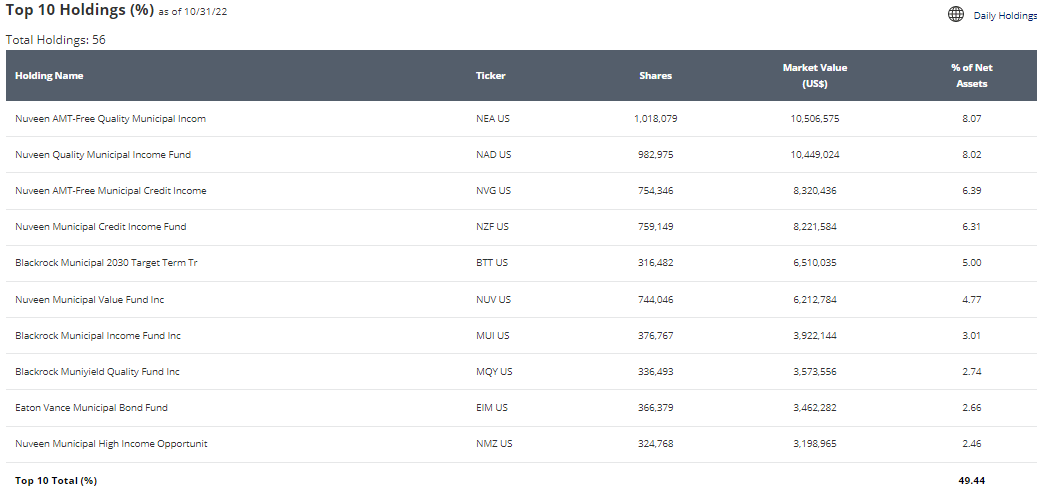

XMPT Top Ten (VanEck)

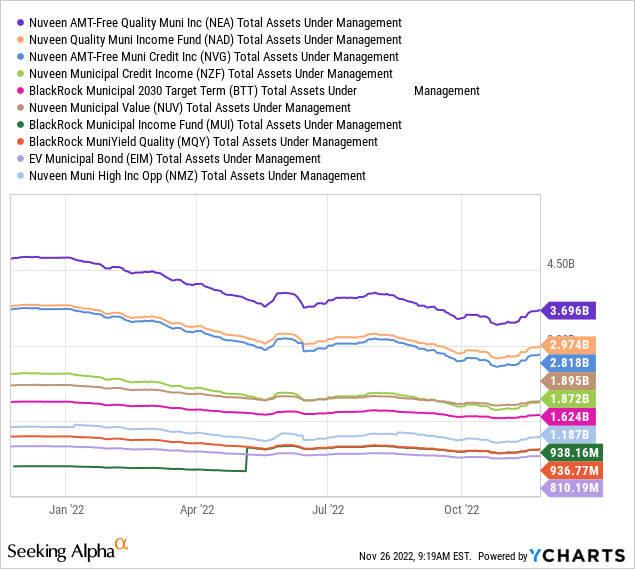

Nuveen ATM-Free Quality Municipal Income Fund (NEA), Nuveen Quality Municipal Income Fund (NAD) and Nuveen AMT-Free Municipal Credit Income Fund (NVG) are some of the largest CEFs available. Even Nuveen Municipal Credit Income Fund (NZF) and Nuveen Municipal Value Fund (NUV) are fairly large.

Ycharts

Keep in mind that above is only showing the net assets of the fund. With leverage, they are considerably larger. NEA has $6.462 billion in total managed assets, and NAD has $5.158 billion – meaning both are carrying over 40% in leverage.

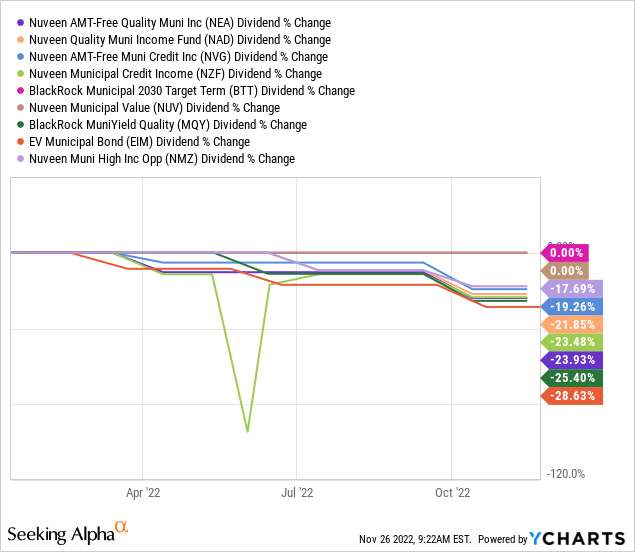

When looking at the distribution changes on a YTD basis, we can see that 8 of the top 10 funds have cut their payouts. Most having cut on more than one occasion. NEA cut from $0.0585 per month to $0.0525 and then now to $0.0445.

Eaton Vance Municipal Bond (EIM) cut from $0.0496 to $0.0454, to $0.0412 and finally now to $0.0354.

Ycharts

I don’t suspect that these will be the last cuts, either. It won’t stabilize until the Fed quits raising interest rates, as the leverage costs on these underlying funds are primarily variable. That’s eating into their income generation. At the same time, the portfolio turnover is slow with long maturities, so they can’t get par back to reinvest in higher-paying yields quickly.

This all should mean that an investor in XMPT should expect a decline in dividends paid every month for the next 3 to 6 months potentially. At the same time, appreciation from the optimism of the expected pause in rates and a decline in discounts from this point could counteract that negative. In the end, it could still result in positive results even with declining distributions if the Fed doesn’t have to get aggressive again.

XMPT only holds around 56 holdings. For a fixed-income fund, that would be rather low. However, their underlying portfolios can mean it holds thousands of different bonds. According to CEFConnect, NEA holds 1278 different bonds. I’m sure there is a significant overlap with the other Nuveen funds. It still means there is considerable diversification across issuers here.

Conclusion

XMPT is a rather interesting ETF that invests in municipal closed-end funds. As an ETF, it is passively managed based on a reconstitute semi-annually and quarterly rebalancing. However, the underlying holdings are actively managed funds. They are making changes much more frequently. The underlying CEFs can also trade at large discounts, presenting a fairly strong opportunity as they are trading at wider than usual discounts.

However, the funds are also leveraged. That can make them more volatile and risky overall. The higher leverage costs are now leading to distributions being trimmed across the board. That leads to a lower trending dividend for XMPT. Despite that, if the Fed pauses in the next few months, the positive could outweigh the negative. That’s primarily what makes muni bonds relatively attractive at this time.

Be the first to comment