halbergman

It’s been a while since I last visited WestRock (NYSE:WRK) back in July. I found the stock to be trading at a good value price at that time, and the stock has fallen in sympathy with the rest of the market since then.

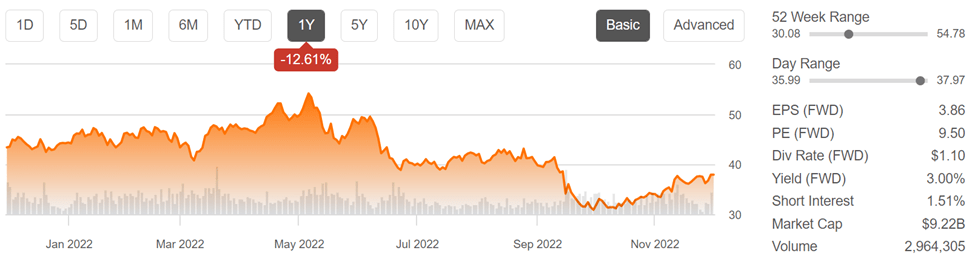

Despite the recent share price recovery, WRK still trades far below its 52-week high of $55, as shown below. In this article, I highlight why WRK is an attractive option for those who seek a meaningful dividend yield combined with potentially strong capital appreciation.

WRK Stock (Seeking Alpha)

Why WRK?

WestRock is a paper and packaging products company that supports clients around the world, with operations North and South America, Europe, Asia, and Australia. The company has a diversified product mix with corrugated packaging accounting for approximately 60% of sales, followed by consumer packaging (15%), and paper and recycling (25%). In total, WRK serves over 25K customers in various end-markets including food and beverage, home improvement, e-commerce, and healthcare.

I view WRK as being an indirect investment in e-commerce growth, as more online shopping will undoubtedly require more sustainable paper and packaging solutions provided by WestRock. This is supported by recent U.S. Census Bureau data, which notes that e-commerce sales accounted for 14.8% of total retail sales during the third quarter of this year. E-commerce is also expected to grow at a strong 15% annual rate between now and 2027.

Meanwhile, WRK appears to be showing all signs of robust participation in this growth, as it generated 6% YoY revenue growth to a record $5.4 billion in its fiscal fourth quarter (ended Sep. 30th). This caps a strong year for WRK, with full year revenue and net income both growing by an impressive 13%, despite broad based economic volatility. This gave the company leeway to raise its fourth quarter dividend by 10% to $0.275, putting it well on track to reclaim its pre-pandemic rate of $0.465. The current dividend is also well covered by a low 21% payout ratio.

Also encouraging, WRK is exhibiting signs of efficient scale through operating leverage, as full year adjusted EBITDA grew at a faster pace than revenue, at 15% growth. WRK is putting its capital to good use, as it repaid $236 million worth of debt during its fiscal fourth quarter, reducing its net debt to EBITDA ratio to 2.05x, sitting well within management’s stated target leverage in the 1.75x to 2.25x range.

Moreover, WRK currently has $3.7 billion of liquidity, comprised of cash on hand and available liquidity on revolving credit facilities, giving int plenty of financial flexibility, as noted by management during the recent conference call:

As we look ahead, we plan to continue to use our strong free cash flow to invest in our business and return capital to our shareholders through our dividend and opportunistic share repurchases. We will also continue to pursue attractive tuck-in acquisitions. While we have seen a slowdown in corrugated demand due to inventory destocking and the slowing economy, our Consumer segment remains robust, demonstrating the value of our diverse portfolio to navigate the current challenges.

Turning to valuation, WRK remains attractive at the current price of $37.92, despite the recent rally in the share price. At this price, it carries a forward PE ratio of just 9.8, sitting well below its normal PE of 13.6 over the past decade. This appears cheap for company which I would expect to achieve long-term annual EPS growth of mid-single digit to low teens range. Analysts have a consensus Buy rating on WRK with an average price target of $42.71, implying a potential one-year 16% total return including dividends.

Investor Takeaway

WRK has shown impressive resilience in the face of a difficult year for many companies, and is well positioned to benefit from ongoing e-commerce growth. The company’s efficient scale operations, strong balance sheet and low dividend payout ratio all make it an attractive option for investors seeking meaningful dividend yield combined with potential capital appreciation.

Be the first to comment