Lemon_tm

The New Year is fast approaching, and you might be looking to make a change – small or large – to your portfolio after a disappointing 2022. If you’re looking for a way to minimize your volatility while keeping pace with the S&P 500’s 10% return, consider the Vanguard Value Index Fund ETF (NYSEARCA:VTV). It’s not an ostentatious investment by any means, but with over $100 billion in assets under management and nearly breaking even for the year, it’s a reputable choice that doesn’t get the spotlight it deserves.

What Is VTV?

VTV is a Vanguard index ETF that tracks the CRSP US Large Cap Value Index. It holds 340 companies, many of which are household names like Berkshire Hathaway (BRK.B), Chevron (CVX), and Pfizer (PFE). VTV’s top 10 holdings account for ~22% of the fund, which isn’t very concentrated.

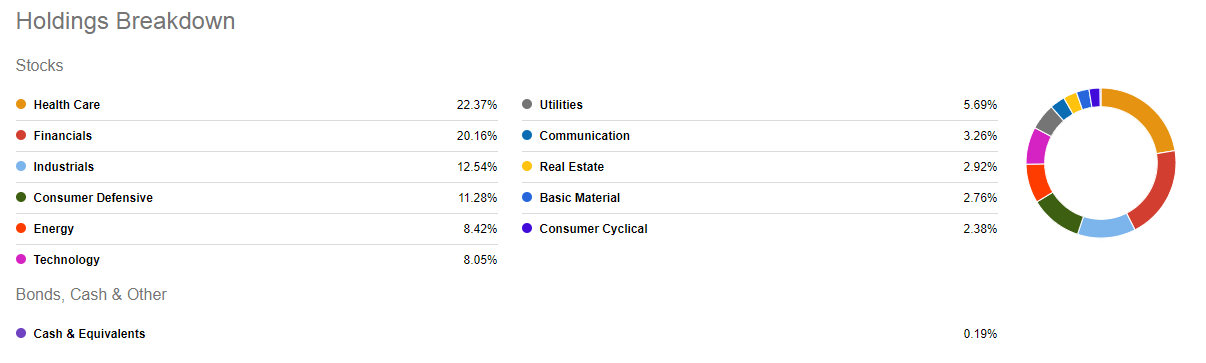

Sector diversification is reasonable, but is dominated by healthcare, financials, and industrials, and consumer defensive stocks.

VTV’s sector diversification is reasonable. (Seeking Alpha)

It stands to reason that VTV can represent the bulk of any portfolio and will probably go up in the long term. After all, it tracks a broadly diversified index and is a part owner of some of the world’s most successful businesses. The real question is: what makes it so special?

Valuations And Risks

We first need to establish that VTV can be expected to outperform the market in the long term. We can do this in many ways, but I prefer a factor analysis.

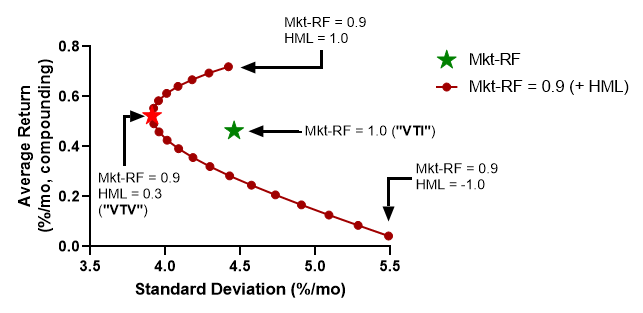

“The market”, which we could invest in with something like the Vanguard Total Stock Market Index Fund ETF (VTI), has a market beta equal to 1 by definition. VTV does not necessarily have the same beta. A Fama-French 5-factor regression on VTV from July 1963 to May 2022 suggests that its exposure to market beta has been ~0.9 and exposure to the HML value factor has been 0.3 (with some negative tilt towards large companies with conservative investment). This is somewhat expected. Large value firms tend to have enough “mass”, for example moats or robust business models, that insulates them from the peregrinations of the market. This means that, on average, we can expect a lower beta.

Using monthly US 5-factor returns from 1963 to 2022 in the Ken French Data Library, we can look for optimal HML loadings given this 0.9 market beta. We see that VTV’s value loading almost exactly matches that of a minimum variance portfolio considering market beta and HML. We also see that simulated VTV generated higher returns than simulated VTI.

Historically, value has provided added value to a market-cap weighted portfolio. (FM Research)

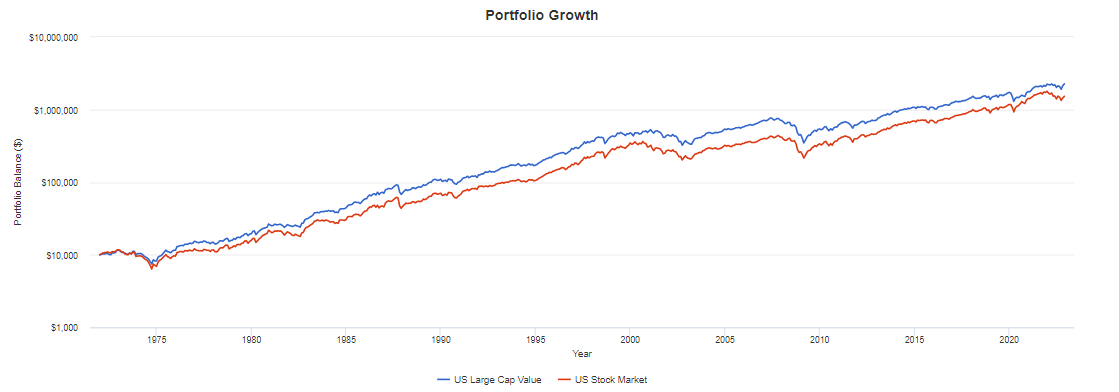

VTV holding the perfect value allocation is interesting, but value outperforming the market is hardly surprising. Value stocks have been clearly ex-ante preferable not only from a returns perspective but also from a risk-adjusted perspective. Indeed, US large cap value stocks have delivered an 11.2% return over the last 50 years with a 15.1% standard deviation. The total US market, on the other hand, fell short with a 10.4% return and 15.8% standard deviation.

Large cap value has outpaced the total US market for 50 years. (Portfolio Visualizer)

A Boglehead might argue that VTV is riskier than holding the market because it contains far fewer securities – 340 large value stocks compared to over 3000 stocks in the US universe. That argument doesn’t appreciate the complexity of portfolio management. You are exposing yourself to different kinds of risks by deviating from the market, but these risks may not matter to you. For example, value stocks suffered greatly during the financial crisis, with a drawdown of 55% compared to the market’s 50%. Large value stocks even took an extra year to recover. Still, if you can tolerate this kind of havoc, then why not deviate from the market? You get a long-term premium for being more risk-tolerant than average.

Why is value a good investment now? We know that both value and momentum exist in capital markets. Value is a long-term strategy, and momentum is a short-term strategy. They are seemingly at odds with each other, but really they just operate on different time scales. The best opportunities will manifest after tremendous periods of underperformance and during their long-awaited upticks.

For this reason, it is inconceivable to me that now is not a good time to buy VTV. Value has “been dead” for nearly a decade now, and if we know anything about markets, we know that they revert to the mean. When will it revert to the mean? Well, that has already been happening. VTV has been beating VTI since March 2020 by over 2% annually.

And because we know momentum exists, we can argue that this macroeconomic performance will persist in the future.

How do we know that this mean reversion isn’t a fluke? There are a number of known macroeconomic conditions where value stocks outperform. As we know, value has been doing well ever since inflation was sky high. William Bernstein suggests that value outperformance is closely related to inflation because growth firms are investing expensive, current dollars to generate future, weak dollars. Large value firms also stand better because they’re big enough to keep operating costs low amid inflation. Interest rates being high is another signal of value outperformance. Growth firms find it more difficult to borrow money.

A darker thesis for value overperformance exists as well. Value firms may be overleveraged due to poor economic conditions. A bet on value is a bet that these struggling firms – not all of them, but many of them – will recover. If that’s not a heroic bet, I don’t know what is.

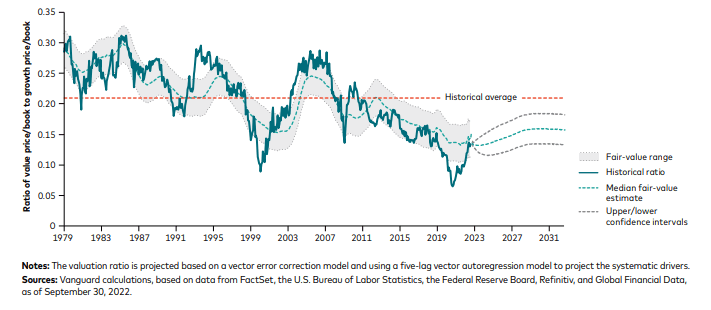

VTV is far from “free money”, however. Opinions conflict. For example, Vanguard itself is more pessimistic than I am. According to their 2023 economic and market outlook whitepaper, US value has only a modest 0.1% expected return edge over broad US equities, but also with deeper tail risk. In other words, value is fairly valued. Still, their odds of value beating the market are over 50% (if only marginally). They even admit that value is cheaper than growth compared to history, and the spread is comparable to those in the tech bubble.

Vanguard argues that value is fairly valued, but still cheap compared to previous decades. (Vanguard)

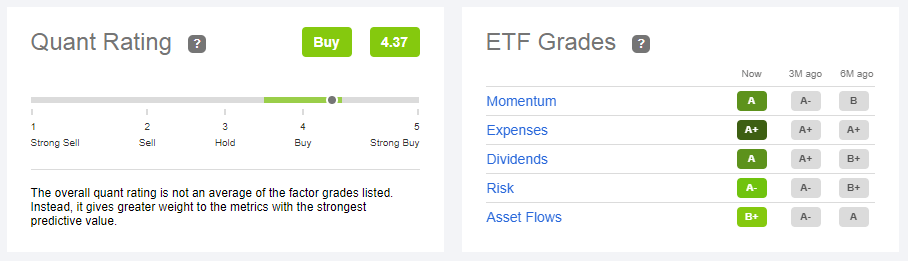

Seeking Alpha’s Quant thinks VTV is low risk (whatever that means), though, giving it a 4.37/5 rating. In addition to agreeing with other metrics, it also points out that the dividend yield is reasonable, at 2.4%.

Quant likes VTV. (Seeking Alpha)

Whether or not VTV’s catalysts are genuine depends on your convictions and how you look at the data, but the data themselves don’t lie – value is at historically cheap levels and is having a great time recently.

How Does VTV Fit In A Portfolio?

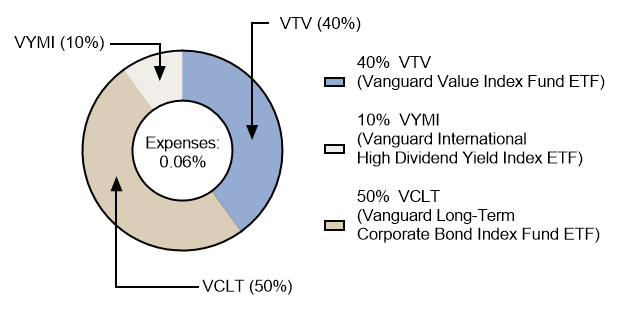

Below is a model portfolio where, in essence, we are selecting stocks with low market correlation and conservative investment. These stocks are all name-brand and large, so they ought to provide some level of comfort in a bear market. That’s VTV, and it’s the core of our model portfolio.

We supplement VTV with high-quality fixed-income instruments. We want to reduce our stock allocation, but we also need safe yield. We can afford to take more risks correlated to the market (i.e. credit risk) because VTV is already low-beta. Therefore, long-term investment-grade corporate bonds are our choice investment. Bonds in VCLT have an average duration of just about 14 years, which is appropriate for a 30-year retirement time horizon.

To maximize our (ex-ante) risk-adjusted return, we use a historical efficient frontier to come up with something around 50% stocks and 50% bonds – the Jack Bogle allocation.

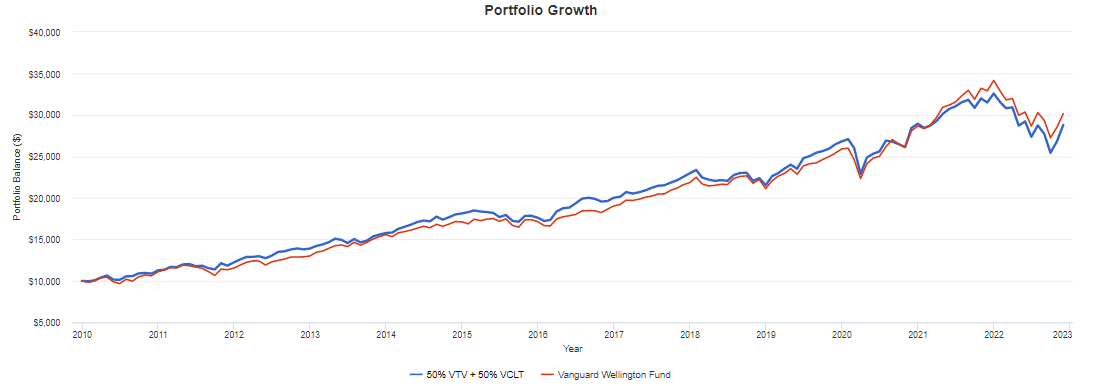

Unsurprisingly (and unintentionally), this allocation tracks Vanguard’s Wellington Fund (VWELX) quite well.

The VTV model portfolio performs similarly to Vanguard’s Wellington fund. (Portfolio Visualizer)

From there, I would add international stocks to taste. Remember, in this portfolio we want to take a little bit of risk with every asset class, but still diversify across many of them. Given this portfolio’s similarity to Wellington fund, we might stick with “no more than 20%” of the stock allocation (though, personally, I’d go 40%). Unfortunately, there are a lack of global ex-US large cap value index ETFs, but the Vanguard International High Dividend Yield Index Fund ETF (VYMI) seems like a sensible (Vanguard-themed) option to boost your dividend yield and stick with the value theme.

VTV model portfolio. (FM Research)

And that’s our build: a value- and credit-oriented take on a traditional three-fund portfolio that resembles Vanguard’s actively-managed Wellington Fund, but with fewer costs.

Conclusion: VTV Will (Probably) Set You Up For A Lifetime

We don’t need to pick a single winning stock if we can pick the winning kind of stock. The past has not been so kind to value, but for now and probably for the future, value is the way to go. Trust the folks at Vanguard. They know what they’re doing. I’m not sure it could be any other way.

Be the first to comment