BrianAJackson/iStock via Getty Images

The S&P MIDCAP 400 ETF Trust (NYSEARCA:MDY) is a widely popular exchange-traded fund (ETF) that seeks to track the performance of the S&P Mid-Cap 400 Index. Mid-capitalization firms usually have a market capitalization in a range of $2 billion to $10 billion. The mid-cap area of the equity market can offer investors a sweet spot of growth opportunity and financial stability. The S&P Midcap 400 ETF Trust provides a cost-efficient method to add exposure to a broad portfolio of mid-cap equities. It is a great option for investors seeking both long-term growth and great diversification.

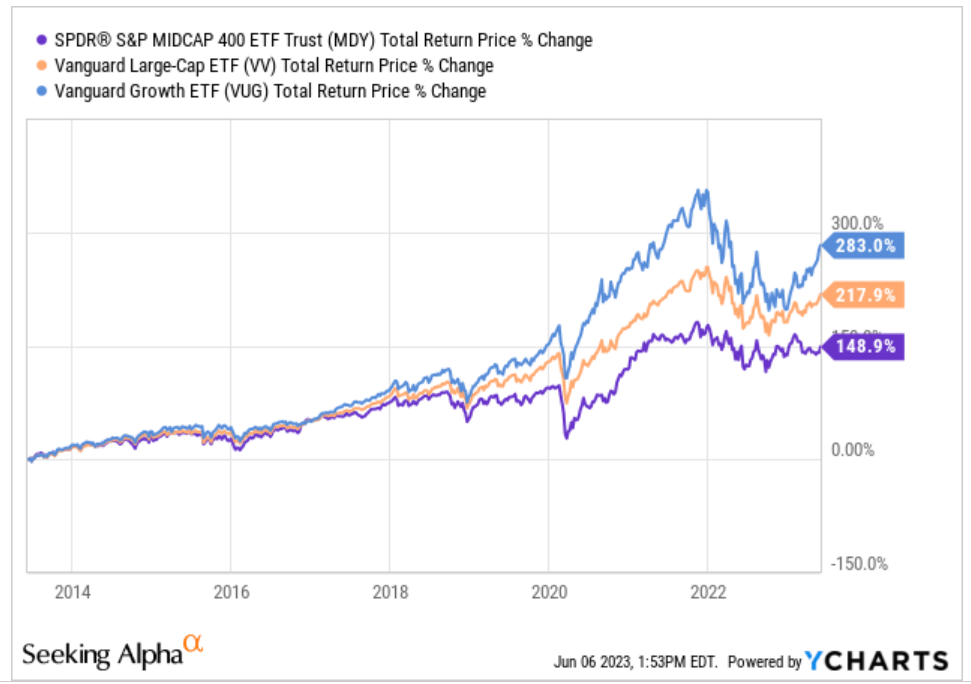

It should be noted that mid-capitalization firms have been trailing large capitalization firms over the past ten years. Large capitalization performance has been especially better in the past couple of bull market stretches. The performance of mega-caps like Microsoft (MSFT), Apple (AAPL), and a few others have been primary drivers of this outperformance in large capitalization equities and that may eventually come to an end.

Historical Comparison Large and Mid Caps (ycharts)

Large Capitalization Outperformance

Large capitalization equities have been outperforming recently. Over the past few years, large capitalization equities have been outperforming their small and mid-capitalization counterparts. This trend can be attributed to several things, including a shift towards growth investments, a favorable economic environment for risk-taking, and a surge in investor confidence in large, well-established firms. Another reason for the outperformance of large-cap equities is the increasing acceptance of index investing, which sometimes favors larger firms with greater market capitalizations, resulting in concentrated large-cap positions in large ETFs. It’s a cycle that results in many investors flocking to large-cap index funds and ETFs, which has helped to drive up the prices of these equities, which in turn draws in more investors. It’s a virtuous cycle during boom times (and can be a vicious cycle in bad times).

In a previous piece, we saw that Apple, Microsoft, and Amazon (AMZN) account for more than 30% of the Vanguard Large Capitalization Growth Fund (VUG). This concentration is an example of how index investing favors greater market capitalizations.

One area where large-cap equities have been particularly popular, and performance has been exceptional, is technology. As the pandemic accelerated the shift towards remote work and e-commerce, larger and more established tech firms have earned larger profits. Firms like Apple, Amazon, and Microsoft have seen their prices surge in recent years, as they continue to dominate their respective markets and money flows into large caps, fueling the overall outperformance of large-cap equities. Investors have poured money into these tech giants and other well-established firms with strong brand recognition and proven track records of success.

Although U.S. large-cap equities are currently stable, there could be other opportunities in the market. If you are seeking areas that provide growth potential and attractive valuations, then U.S. small- and mid-cap equities could be a hidden opportunity worth exploring.

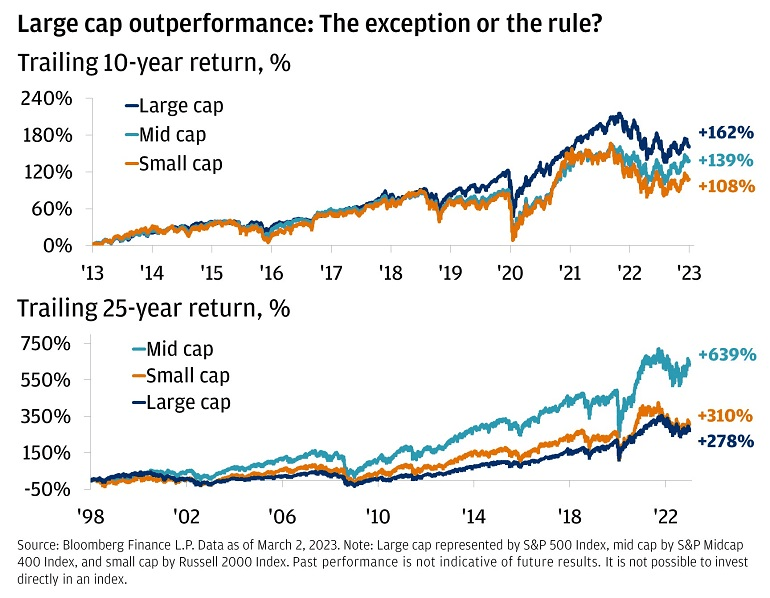

Long-term Comparison Large Mid and Small Caps (JPMorgan)

It may be surprising to know that in the past 25 years, small and mid-cap equities have actually performed better than large-cap firms overall. While many of investors have a tendency to focus on recent results and expect them to continue, it’s important to remember that the past can sometimes be a better indicator of the future. While large-cap firms have boosted overall returns in recent years, it’s important to keep a long-term outlook and consider the benefits of diversifying your portfolio to include smaller and mid-cap firms as well.

Should you sell Large Capitalization Growth equities?

If you are a long-term investor, then it’s not advisable to time the market and try to move from one ETF to the other. One big reason is capital gains tax. If you are buying this in a taxable brokerage account, one of the benefits of buying and holding is reducing your overall tax burden. So, in this case, the recommendation would be to reallocate new capital and dividends to mid-caps like the S&P Midcap 400 ETF Trust.

Which financial gurus favor mid-capitalization equities?

Mid-capitalization equities are preferred by managers such as Bill Nygren, of the Oakmark Fund, and Joel Greenblatt, who runs Gotham Asset Management, and Chris Davis, who manages the Davis Opportunity Fund. Nygren believes that mid-capitalization firms offer a powerful mix of growth potential, stable cash flow, and financial strength. Greenblatt, on the other hand, uses a value investing approach to identify undervalued mid-capitalization equities with high returns on equity and earnings yield (low P/E). Another advocate of mid-cap equities is Chris Davis, who manages the Davis Opportunity Fund and sees these firms as being in a sweet spot between risk and reward.

Bill Nygren, the portfolio manager of the Oakmark Select Fund, likes mid-cap equities because they often offer a bigger chance for growth compared to large-cap equities, but with less volatility than small-cap equities. He believes that mid-cap firms have the promise to become large-cap firms someday, and therefore may offer significant returns for investors who are patient and willing to wait.

Additionally, Nygren believes that mid-cap firms are often under-researched and overlooked by investors. This creates a potential for undervaluing the equity, which can lead to amazing investment prospects. Generally, he sees mid-capitalization equities as a sweet spot for investors who are looking for both growth potential and financial stability.

Joel Greenblatt is another well-known manager who believes that mid-cap equities are an attractive opportunity because they offer the potential for higher returns than large-cap equities without the risk that comes with small-cap equities. Many times, these mid-cap firms are considered to be in a growth phase and have the potential to increase their businesses rapidly, which could lead to significant increases in their price per share.

Chris Davis, a seasoned investor, prefers mid-cap equities for similar reasons. Davis favors these equities because of their high growth potential and ability to offer returns comparable to larger-cap equities. Mid-cap firms have already achieved a level of financial stability but still have room for future expansion, making them the sweet spot for risk-tolerant stockholders. Additionally, mid-cap equities are typically less risky than small-cap equities, which can be subject to wild price swings, making them a safer option for investors seeking to diversify their holdings.

There are others that agree. Mid-capitalization equities offer benefits that large-cap and small-cap can’t match. That’s why you should have a place for them in your portfolio.

Top Ten Holdings

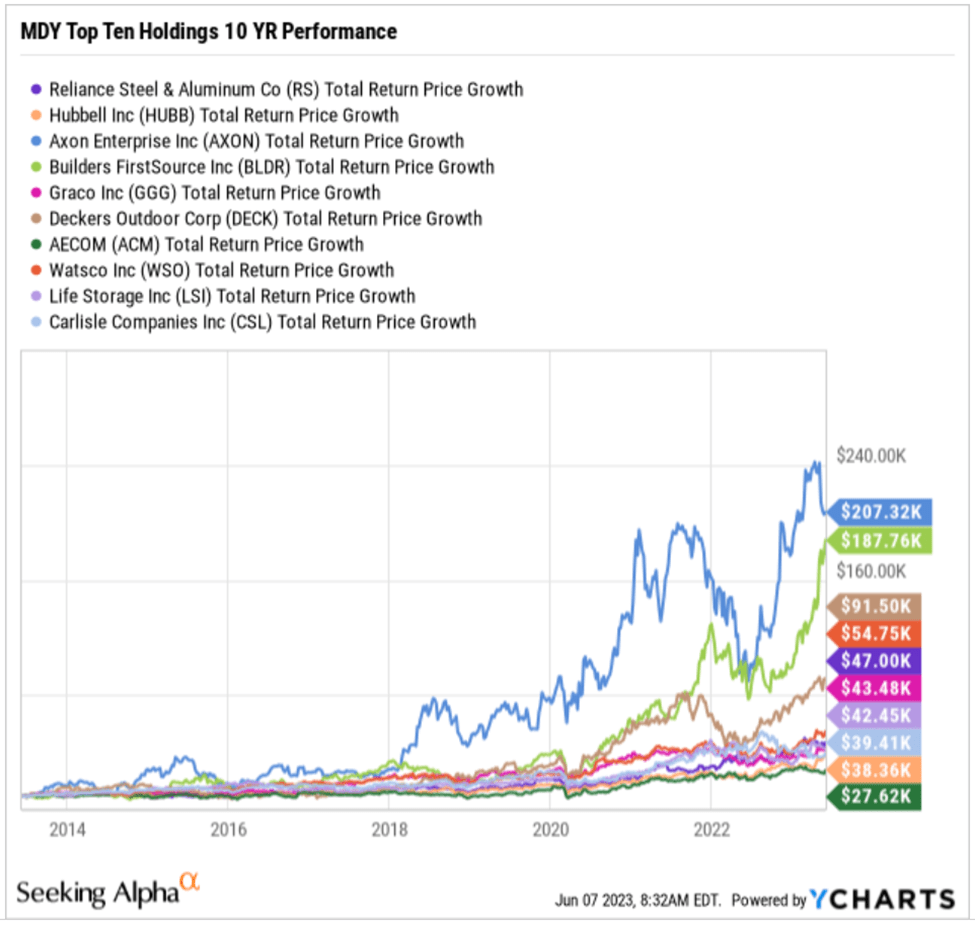

Before looking at the top ten holdings of this ETF, let’s keep in mind that these holdings make up just 6% of the total ETF’s holdings. Because this mid-cap ETF is broadly diversified no single stock will drive it’s performance. Looking at the holdings of the ETF will give the investor a better understanding of what sectors and economic influences will drive performance. These ten stocks have performed very well over the past ten years. Some of them may be excellent investments on their own. The following chart shows how a $10,000 investment might have returned for each of these equities.

MDY Top Ten Holdings 10 YR Performance (ycharts)

Established in 1939, Reliance Steel & Aluminum Co. (RS) is a leader in metals distribution. The company operates over 300 global locations and has a diverse line of metal products. They specialize in processing and stocking stainless steel, carbon steel, alloy steel, aluminum, brass, copper, titanium, and other metal products. This company’s equity has a P/E ratio of about 10 and a dividend yield of 1.63%. This is an attractive valuation.

Hubbell Inc (HUBB) is a global firm with headquarters in Shelton, Connecticut. Founded in 1888, the company manufactures electrical and electronic products for a many sectors, including construction, healthcare, and energy. The company’s products are designed to improve safety, energy efficiency, and productivity and Hubbell Inc has a strong reputation for quality, reliability, and innovation. This company’s equity has a P/E ratio of about 22 and a dividend yield of 1.51%. In many cases, investors might consider that a lofty P/E, but revenue growth has been over 15%.

Axon Enterprise Inc (AXON) is a global leader in law enforcement technology, including products such as body-worn cameras, tasers, and software. The firm is committed to promoting accountability and transparency in law enforcement, and works closely with local governments and agencies to provide training and support. This company’s equity has a P/E ratio of about 62 and no dividend. The lofty valuation comes from an expected growth rate of 26.24% going forward.

Builders FirstSource (BLDR) is a leading supplier of construction materials, providing products to homebuilders and contractors across the United States. Its extensive product offerings include lumber millwork, windows, doors, cabinets, flooring, insulation, roofing, and other building products. This company’s equity has a P/E ratio of about 13 and no dividend. Analysts expect revenue to decline, most likely due to the housing recession, but this is a solid valuation for an established company.

Graco Inc (GGG) is a global leader in providing fluid handling solutions and equipment. Founded in 1926, the company has built a reputation for innovation and reliability. They offer a variety of products for industries such as automotive, construction, and manufacturing. This company’s equity has a P/E ratio of about 26 and a dividend yield of 1.17%. Forward looking revenue growth is only 5.3%. This equity may be a bit overvalued.

Deckers Outdoor Corp (DECK) is an American footwear company founded in 1973. The company has several well-known brands including UGG, HOKA ONE ONE, Teva, and Sanuk. The company is committed to sustainability and has implemented several eco initiatives, such as reducing waste and promoting eco-conscious materials. This company’s equity has a P/E ratio of about 22 and revenue growth estimates of 12% next year. This is a solid growth company.

AECOM (ACM) is an engineering and infrastructure firm that provides professional services to clients across the globe. With over 87,000 employees operating in more than 150 countries, the company is a leader in delivering solutions for important infrastructure projects. The company’s areas of expertise include transportation, water, energy, and environmental engineering. This company’s equity has a P/E ratio of about 22 and a paltry dividend yield of 0.79%. Revenue growth expectations are low at 3.77%, but as a professional services firm, the stock commands a value premium.

Watsco Inc. (WSO) is a leading distributor of HVAC products in the United States. Founded in 1956, the company has grown to include 600 locations throughout North America and they aim to offer unsurpassed service to contractors, promoting energy efficiency and sustainability. This company’s equity has a P/E ratio of about 24 and a dividend yield of 2.84%. Watsco pays out about 64% of earnings as a dividend, but is still expected to grow revenue by 7.25%. This is an intriguing investment for a value investor.

Life Storage Inc (LSI) is a real estate investment trust (aka REIT) specializing in self-storage facilities. The company is headquartered in Williamsville, New York and was founded in 1982. With over 925 properties nationwide, Life Storage offers customers a wide range of self-storage options, including climate-controlled storage units and automobile storage. This dividend yield of 3.79% and double digit growth rate of 14.6% are very interesting and investors should take note.

Carlisle Companies Inc (CSL) is an industrial company that manufactures commercial and industrial products to a variety of customers in multiple markets. The company operates through four business segments: Construction Materials, Interconnect Technologies, Fluid Technologies, and Brake & Friction. This company’s equity has a P/E ratio of about 12 and a dividend yield of 1.32%. With revenue growth expected to be 10.39%, this is a solid value investment.

Dividend Growth and Yield

The S&P Midcap 400 ETF Trust has seen remarkable dividend growth in the past ten years. In 2013, the ETF’s dividend was $2.61, but it has since grown to $6.09 per share. This is a fairly significant rise of 133% in just a decade. The ETF’s dividend yield was 1.34%, most recently, offering investors a decent yield.

Investors who are looking for dividend income growth may find the ETF’s track record of dividend growth appealing. Additionally, the ETF’s exposure to mid-sized firms may offer growth potential as well, for reasons outlined above.

Expenses

The S&P Midcap 400 ETF Trust is noted for having a fairly low expense ratio, which is one of its key advantages. This ETF charges an expense ratio of only 0.23%, which makes it an affordable ETF for most investors. Having a low expense ratio is crucial for long-term wealth accumulation. A higher expense ratio can erode investment returns over time, so reducing expenses is essential to success.

Conclusion

Overall, the S&P Midcap 400 ETF Trust is a solid option for those seeking exposure to mid-cap firms with strong growth potential, financial stability, and a steady stream of income through dividends. Its low expense ratio, diversification, and passive management make it a cost-effective and relatively lower-risk investment. With the current market environment, this may be a more attractive long-term investment than large capitalization equities. So, allocation of new capital to MDY ETF may make sense.

Be the first to comment